Low temperatures and patchy wind outputs have inevitably meant high gas-for-power generation this week.

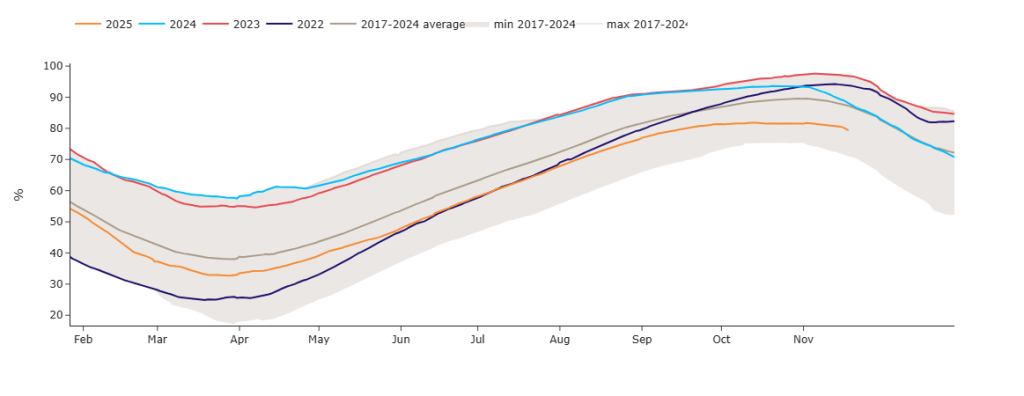

As such, European storage is threatening to “roll over” into wintry net withdrawal – please see chart below.

For the time being, inventories remain steady at 80% versus the 7-year average of 87%.

This morning prompt gas prices opened lower off the back of forecasts predicting temperatures back up above seasonal norms by the end of the month.

The UK gas system is “long” at the time of writing (supply outstripping demand forecast).

Down the curve into ’26/’27/’28, gas prices are marginally softer amid news of a potential “peace deal” between Ukraine and Russia.

Of course, a lasting peace across Eastern Europe would very likely lead to improved gas supplies due to sanctions against Russia being lifted (both pipeline and LNG).

Market bulls are already staring down the barrel amid the prospect of an LNG glut come ’27 onwards.

If Russian gas were thrown into the mix, commodity prices would very likely return to pre-pandemic levels.

Monthly Day-Ahead averages for November so far are at 76p/therm (or 2.6p/kwh exc. non-gas).

The cosmos in my garden looks to be on its last legs (indicating the heating season can’t be far off)!

ELECTRICITY & CARBON

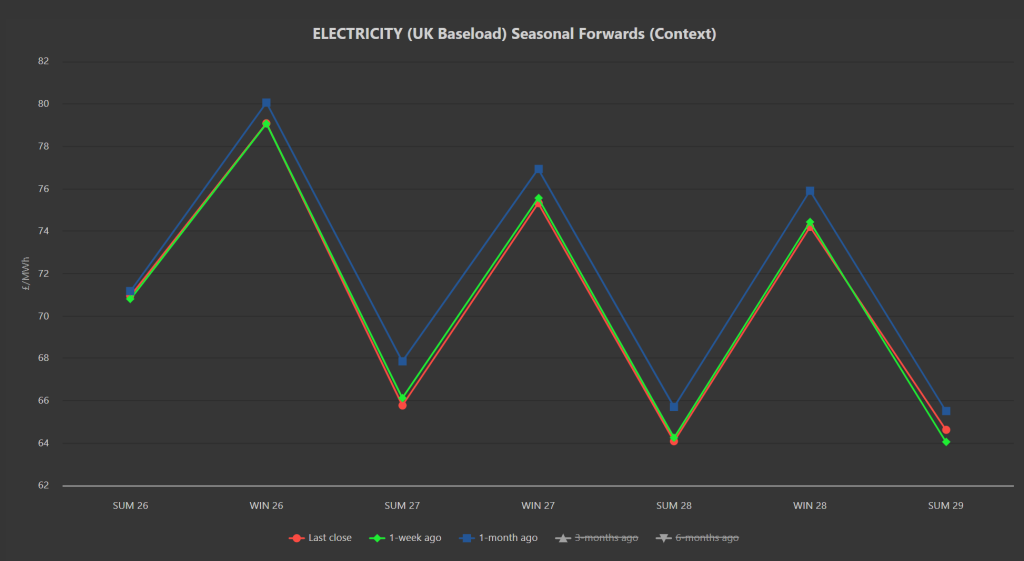

Electricity Seasonal Forwards remain down on the week, and the month (please see chart below).

On the Carbon side of things, UKAs continue to trade below the increasingly important resistance level of £58.50/tn, but have failed to fall back (yet) to the increasingly important support level of £55.50/tn.

Instead, traders are carving out consolidation patterns between these two levels pending bullish/bearish stimulus.

Today’s UK electricity generation mix is bullish in nature given patchy wind outputs – specifically, renewables are contributing 26%, thermal at 45% (gas and coal) and low carbon at 14% (nuclear and imports).

Monthly Day-Ahead averages for November so far are at £76/mwh (or 7.6p/kwh exc. non-energy).