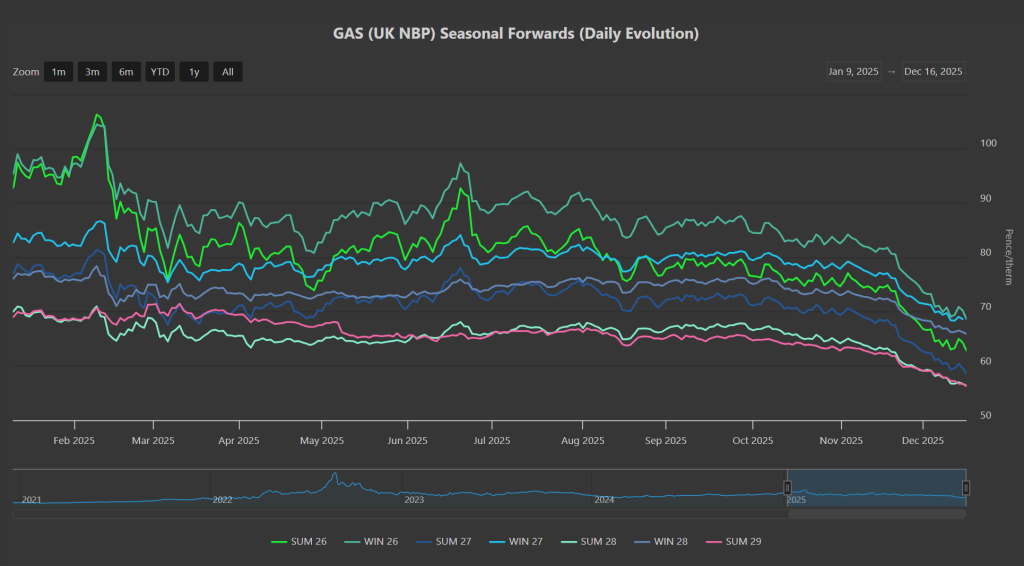

Whilst Seasonal Forwards are pretty flat on the week, it’s worth noting the front 3-Seasons (Summer-26/Winter-26/Summer-27) have fallen approximately 40% versus last winter’s highs, and approximately 19% since the onset of Winter-25 (beginning 1st Oct ’25) – please see ‘Daily Evolution’ chart below.

These unseasonal falls in price reflect above average temperatures, solid wind outputs (limiting gas-for-power burn and storage withdrawals), very steady supply from both LNG and Norwegian pipeline, optimism surrounding Ukraine/Russia peace talks, rumours of a glut of LNG supply come ’27, and healthy European storage fullness (now at 69% versus the 5-year average of 74%).

On the weather side, warmer temperatures are forecast for the coming days coupled with high winds – amid soft demand, such conditions will inevitably put pressure on prices in the lead up to Christmas.

Though it’s worth noting that the front month is struggling to break below a strong price support level at 70p/therm – so the bears will have to go-some to get prices lower, and keep them lower.

President Zelensky has been quoted as saying he has “a framework of the security guarantees he needs” to end the war – as such, bearish traders have everything crossed that Russian gas flows could return to the global supply system next year.

However, territorial concession remains a significant sticking point, and it’s unclear how this hurdle might be overcome…

Monthly Day-Ahead averages for December are holding steady at 70p/therm (or 2.4p/kwh exc. non-gas).

ELECTRICITY & CARBON

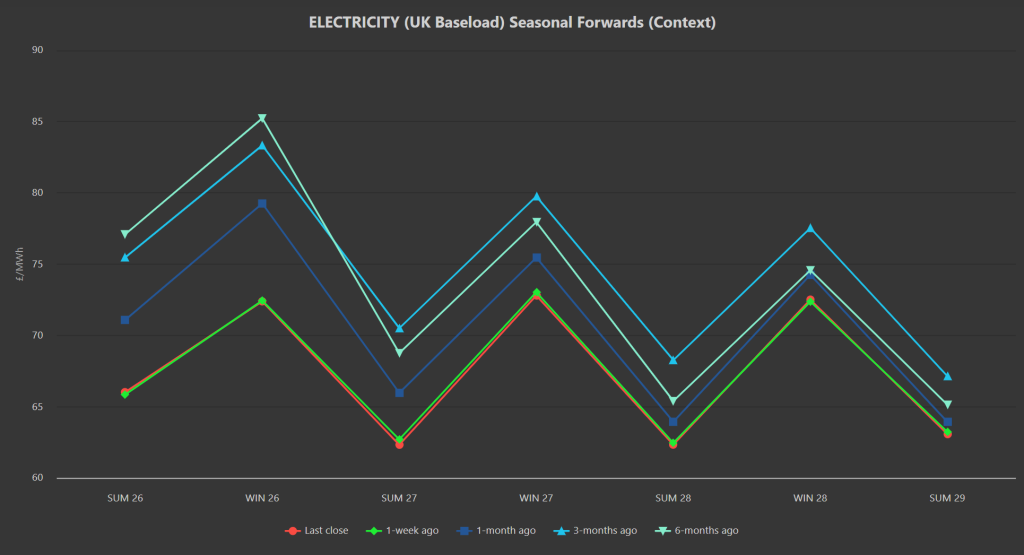

Notably, Seasonal delivery prices all the way down the curve are flat on the week, but down versus 1-month/3-months/6-months ago (please see ‘Context’ chart below).

On the Carbon side of things, UKAs went as low as £55.10 last week on the mid-price – their lowest level since late-Oct ’25 – however, this week marked the end of the Dec-25 dlivery product and so traders managed to keep prices high until expiry on 15th.

Thereafter, markets have “gapped-up” to reflect the Dec-26 delivery product – though spot prices are about £2/tn lower at around £58/tn.

Nonetheless, rumours abound amongst Carbon traders that the EUA/UKA linkage talks are not going as well as hoped (a bearish driver for UKAs) – let’s see what next year brings once holiday illiquidity has abated.

Today’s UK electricity generation mix is slightly bearish in nature – specifically, renewables are contributing 45%, thermal at 30% (gas and coal) and low carbon at 15% (nuclear and imports).

Monthly Day-Ahead averages for December so far are holding steady at £73/mwh (or 7.3p/kwh exc. non-energy).