The arrival of this year’s Siberian Express weather system across the US last weekend spiked heating demand and temporarily disrupted gas production triggering bullish fervour and taking the market higher.

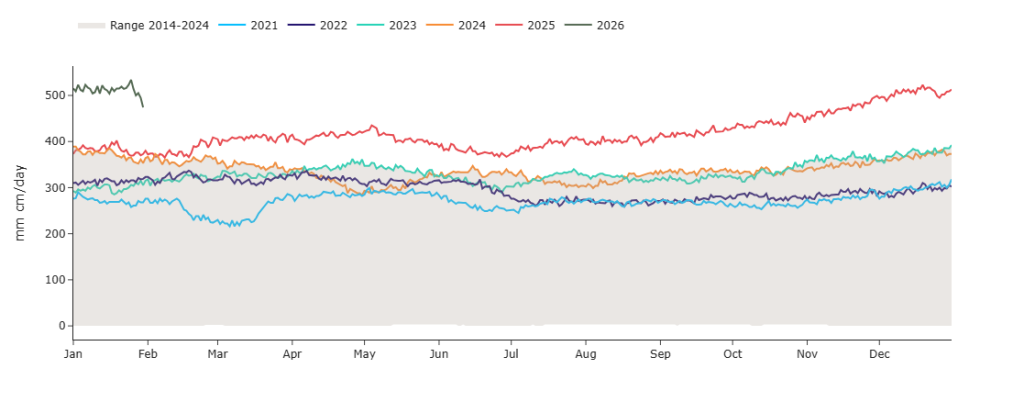

As this began, US LNG exports to Europe dropped off a cliff due to the heightened domestic requirement (please see chart of US LNG exports below, 2014 to date).

A drop in US exports gave further support to European/UK markets (as prices needed to rise to attract what little LNG was left on the seas).

US exports are now recovering somewhat, and remain well above historical levels, so this blip is only temporary (so not really affecting longer-term delivery prices down the curve).

However, near-term delivery European/UK contracts remain elevated – posting their largest percentage monthly gain in more than two years off the back of wintry conditions and ever-dwindling European stocks (now at 43% versus the 5-year average of 68%).

In other price supportive supply news, Norwegian pipeline flows remain below their 10-day moving average primarily due to scheduled maintenance at key processing facilities like Nyhamna.

Tensions between the US and Iran continue to simmer, lending support to oil markets (rising oil prices invariably push natural gas prices higher due to increased demand for gas as a substitute fuel for heavy industry).

On the weather side, it seems increasingly likely that mid-Feb will bring below seasonal norm temperatures across Europe/the UK – but it’s just normal wintry cold spells, nothing out of the ordinary.

For now, temperatures for the UK (and swathes of mainland Europe) remain comfortably above seasonal norms (mitigating the bull rally we’ve seen this week).

On the strategy side, FLEX clients are still taking small positions further down the curve where prices look positively summery compared to prevailing Day-Ahead/Month-Ahead which are currently well-above 100p/therm.

Monthly Day-Ahead averages for the month are up to 89p/therm (or 3p/kwh) reflecting multiple daily closes above 100p/therm over the last fortnight.

ELECTRICITY & CARBON

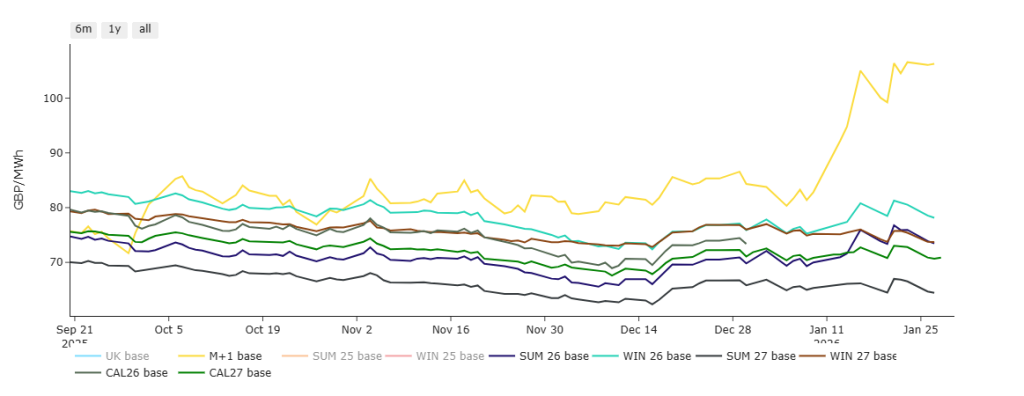

Following months of benign winter conditions, Month-Ahead prices began to pull away from Seasonal Forward prices back in mid-Jan, and are now approx. 30% higher than prices further down the curve (please see chart below).

On the Carbon side of things, UKAs are increasingly on a leash following EUAs’ every whim following recent pronouncements by the EU that talks to merge UKAs and EUAs are going well.

Nonetheless, this week has seen another softening of EUA/UKA prices most likely off the back of investment funds taking profits and piling their specualtive interest into gold and silver.

Once metals become overbought, it’s a safe bet that investment funds will return to Carbon anew.

Compliance buyers (whose activity in the market is eclipsed by the investment funds) can only ride the waves and are being advised to set downside targets then buy on the dips as and when investment funds take profits – so timing is everything.

Please note, UKA spot prices on the secondary market remain at an approximate £2/tn discount to Dec-26 delivery.

Today’s UK electricity generation mix is bearish in nature off the back of windy conditions – specifically, renewables are contributing 50%, thermal at 19% (gas and coal) and low carbon at 19% (nuclear and imports).

Monthly Day-Ahead averages for the month so far remain wintry at £97/mwh (or 9.7p/kwh exc. non-energy).