Prices have taken a breather this morning, drifting marginally lower following two consecutive days of gains.

Market participants are weighing up supply risks (the closure of the Strait of Hormuz) and the seeming renewed efforts by the U.S. to convice the markets that everything is under control.

Whilst Europe’s flows have actually held actually held up well this month so far (supported by solid Norwegian pipeline delivery), the undeniable challenges of refilling storage over the coming summer months loom large.

With the Strait of Hormuz closed, Asian buyers will be increasingly active across global LNG markets bidding high for cargoes – this of course will mean European/UK prices will have to stay high so we can continue to attract vessels to our shores.

In his latest flip-flop, Trump has abandoned efforts to recruit international partners to join the US in their war on Iran, and criticised allies who have publicly rejected his calls for support – though we hear this morning that the UAE may be preparing to help the US clear the Strait of Hormuz (though how this will be done has yet to be confirmed).

Meanwhile, the US/Israel coalition have continued to drop bombs on Iran and Lebanon, with Israel successfully targeting Iran’s security chief, Ali Larijani – Iran have now confirmed he’s dead.

We also hear this morning that Iran’s Intelligence Minister was killed overnight.

Worryingly for oil traders, Trump has warned that the US may expand attacks to include Kharg Island (Iran’s main export terminal).

As a net exporter of oil/gas, the US is demonstrating/exploiting their resource supremacy over Europe/Asia (as net importers of oil/gas) – ultimately, the US doesn’t need the Strait of Hormuz to be re-opened…

Operations were suspended at the Shah natural gas field in the United Arab Emirates after a drone strike triggered a fire on Monday, with officials now assessing the extent of the damage.

Amongst analysts, consensus of where this is headed is hard to find, but notably, HSBC Holdings Plc has lifted its European gas price outlook for the year, warning that prices could remain elevated for longer, reflecting deepening supply risks and the prolonged disruption in the region – though, this is just a big fund hedging its bets.

Domestically, surging oil prices are beginning to feed through into U.S. gasoline costs, adding further political and economic pressure – though Trump has yet to show any signs of capitulating.

Yesterday, a top counterterrorism official has resigned urging Trump to “reverse course” – so, cracks are beginning to show from within Trump’s Administration.

Fundamentally speaking, weather forecasts remain confident of a ramp up in temperatures for the working week.

Temperatures could climb as high as 4˚C above average on Wednesday for the UK.

On the strategy side, FLEX clients are being encouraged to build modest positions further down the curve beginning Summer-28 (where pre-Iran war prices persist, reflecting an underlying sentiment that this conflict is not expected to be long-term).

Where near-term delivery is concerned, FLEX clients with open volumes (who prior to 28th Feb were looking forward soft, summery Day-Ahead numbers), are weighing up budget certainty at high prices versus waiting to see how the coming week plays out.

Were the war to end abruptly, whilst it would take a few weeks for the Gulf to recover from infrastructure damange, it’s still expected that front-end delivery prices would drop like a stone.

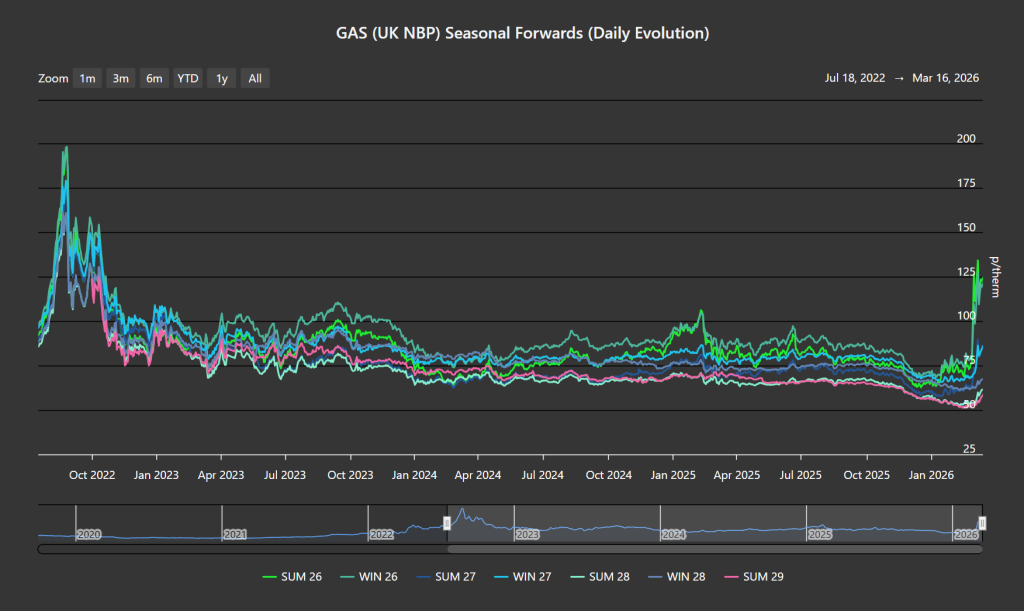

The chart below shows how acute the spike has been in near-term Seasonal Forwards (Summer-26/Winter-26) since Trump (without having consulted with Congress) launched his ill-defined attack – increasingly, rumours abound in Washington that Trump was misled by Israeli lobbyists.

Monthly Day-Ahead averages for the month remain high – currently at 125p/therm (or 4.2p/kwh).

ELECTRICITY & CARBON

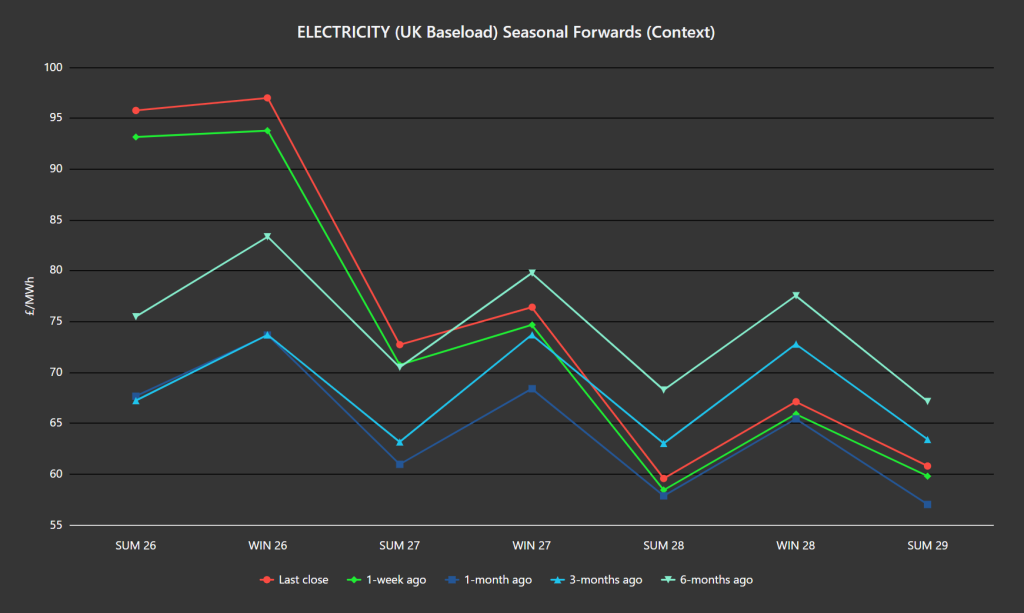

As per the Seasonal Forward Context chart below (showing how prices are changing over time), electricity Forwards continue to mirror gas movements (high near-term, relatively unchanged long-term).

Conversely, on the Carbon side of things, Dec-26 UKA delivery remains uncoupled from gas volatility with prices touching levels that are 45% below those printed in mid-Jan amid fears that Trump’s war on Iran is slowing global economies (and, in so doing, Industrial outputs).

At the time of writing, UKA mid-price Dec ’26 delivery is at £37.16/tn (and the spot is at mid-35s).

Today’s UK electricity generation mix is neutral in nature – specifically, renewables are contributing 38%, thermal at 20% (gas and coal) and low carbon at 25% (nuclear and imports).

On the strategy side of things, electricity FLEX clients are being encouraged to build modest positions further down the curve where steady prices persist (given that far term delivery prices are as much as 37% below those of near-term delivery).

Where near-term delivery is concerned, FLEX clients with open volumes are weighing up budget certainty at high prices versus waiting to see how the coming week plays out.

Monthly Day-Ahead averages for the month so far are mirroring near-term gas prices – currently at £113/mwh (or 11.3 p/kwh).