Prices across the board remain elevated, amid fears that Trump’s war on Iran has the potential to influence outcomes beyond the Gulf (Ukraine/Taiwan/Lebanon/Syria).

Certainly, protracted supply shortages will hamper Europe’s ability to successfully replenish storage ahead of Winter-26 (with Asia being forced to compete with Europe for US LNG exports).

Fears are mounting that the US may escalate the conflict by putting boots on the ground (with thousands of Marines looking increasingly likely to lay siege to Kharg Island in the coming days).

For buyers, whilst adopting a wait-and-see approach has worked well up to now (with prices closing on Friday down on the week), consensus is building that front-end delivery poses increasingly high risk.

As of today, none of our FLEX clients are entirely exposed to Day-Ahead heading into Summer-26 (despite how well Day-Ahead has performed over the last couple of summers).

Looking at the bigger picture, Iran’s retaliatory strikes on key Gulf infrastructure have exascerbated what was already a disastrous closure of the Strait of Hormuz – most notably, damage to Qatar’s giant Ras Laffan complex, with repairs forecast to take as long as 5-years (which we doubt).

This latest supply crisis underscores Europe’s inherent energy security weaknesses, with electricity generation, heating, and industrial outputs still heavily reliant on the stability of increasingly unstable parts of the world.

Today, prices have been steady (and even a little bit bearish over the last hour or so) as markets take a breather (and funds no doubt take profits).

Yemeni Houthis launched their first attacks on Israel over the weekend.

Rumours abound that the Houthis in support of Iran may opt to close the Bab al-Mandab strait at the southern end of the Red Sea (between Yemen and the Horn of Africa).

Coupled with the Strait of Hormuz, this would mean two of the world’s main strategic waterways for trade and energy supplies would be closed for business.

Australian LNG is still contending with disruption caused by last week’s Tropical Cyclone Narelle.

Oil prices are not reacting well to Trump’s increasingly cursory stalling tactics, with intraday Brent having reached $116 this morning.

On a more positive note, the rate of price increases across European gas markets have slowed as comfortable domestic fundamentals (higher wind generation in particular) are giving rise to some welcome downward pressure.

With only 2 days left before the onset of Summer-26, buyers have opted in the main to scale-in hedges of the front-month (Apr ’26) – thereafter, hedging subsequent months or Balance of Quarter remains a viable option, allowing buyers a little more time to see how things develop over the coming days/weeks.

If the Strait of Hormuz re-opens off the back of successful diplomacy, near-term delivery prices will inevitably fall sharply – though, increasingly, hopes of a timely end to this conflict are slipping away…

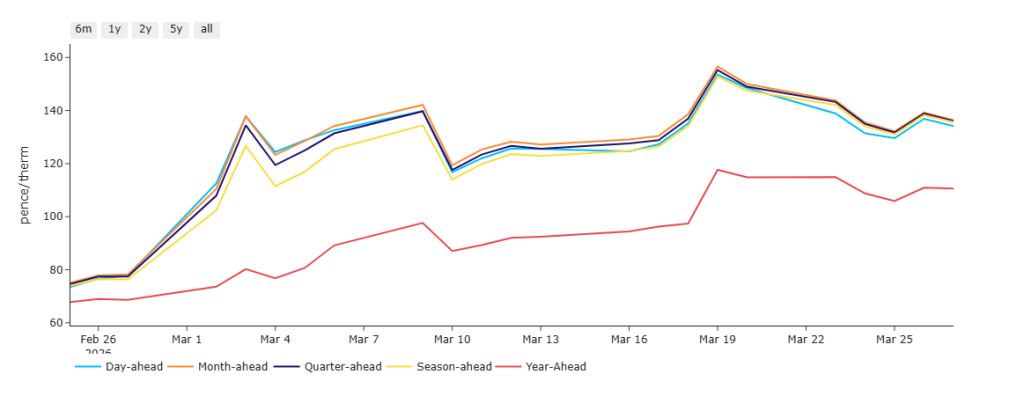

The chart below shows how the Prompt (near-term delivery) market has behaved since the offensive began – notably, Day-Ahead remains comfortably below Month/Quarter/Season-Ahead, with Year-Ahead remaining comparatively soft (reflecting an underlying belief that the lion’s share of risk is mid-term loaded).

Monthly Day-Ahead averages for the month remain high but stable – currently at 130p/therm (or 4.45p/kwh).

ELECTRICITY & CARBON

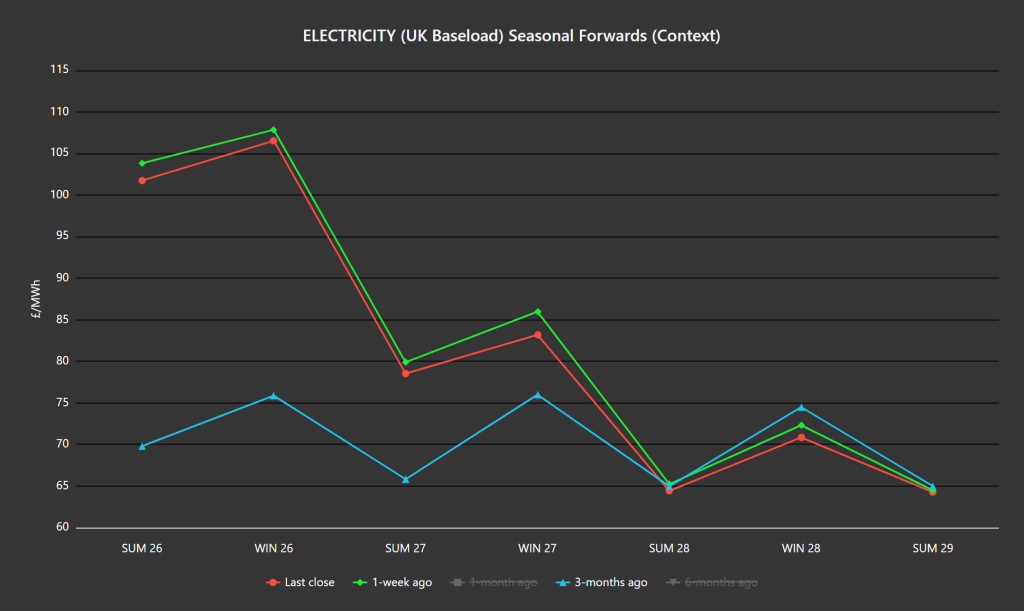

Friday’s Seasonal Forward close was down on the week but at a yawning premium to 3-months ago (please see chart below).

On the Carbon side of things, Dec-26 UKA delivery remains uncoupled from gas volatility with prices touching levels that are 35% below those printed in mid-Jan amid fears that Trump’s war on Iran is slowing global economies (and, in so doing, Industrial outputs).

At the time of writing, UKA mid-price Dec ’26 delivery is at £38.45/tn (and the spot is at early-37s).

Over the last couple of weeks, when gas falls, UKAs firm up – and vice versa.

Monthly Day-Ahead averages for UK electricity for the month so far fell slightly to end last week – currently at £105/mwh (or 10.5 p/kwh).