Not surprisingly, given the backdrop of Israel’s continued bombardment of Lebanon, this weekend’s talks in Islamabad between the US and Iran failed to achieved a diplomatic outcome.

And so, the Strait of Hormuz remains shut, and LNG cargoes to Asia remain stuck outside the waterway.

Trump’s latest gambit is to establish a blockade of the Strait (notwithstanding the fact that an Iranian blockade is already in place).

As has become the norm, analysts are second-guessing Trump’s intentions – which, of course, assumes Trump knows what he intends.

We suspect he wants to encourage the Iranians to attack his blockade, giving the US just cause to retaliate, and in so doing, re-escalate the conflict.

So, only one thing is sure at this stage, nothing will be getting through the Strait of Hormuz over the coming days.

As you’d expect, prices across the board have risen (though only marginally) at this morning’s open.

Brent crude futures are back up above $100, having gapped-up at this morning’s open (the chart below shows clearly how out of hours events are becoming the norm in oil markets under Trump’s watch – having gapped-down significantly on Tuesday night of last week, only then to gap-up over the weekend).

The rule of thumb in markets is that gaps are ALWAYS filled – so expect the market to retrace at some point so as to fill the gap left by the last 7 days’ price action.

In short, Trump is playing fast and loose with the markets, and his approach to the conflict oscillates from one compulsion to the next – as such, there’s not a trader out there who knows where this is going.

Trump is not following a long-established wartime and/or diplomatic playbook – instead, he’s making it up on the fly.

The only potential upside to the US Navy occupying the Strait of Hormuz by this afternoon is if they successfully clear the Oman side of the waterway of mines laid by Iran, then assume control of the Iranian coastline making it impossible for Iran to exert control over vessel transit.

However, this will no doubt involve a ground offensive, and the inevitable deaths of untold numbers of US personnel – can Trump’s already spiralling domestic approval numbers take it (amid rising gasoline prices, and interest rates)?

Trump’s self-declared friend, Viktor Orbán, has lost power in Hungary – giving way to Péter Magyar in a landslide two-thirds majority victory.

Theoretically, this should make it easier for Ukraine to access European financial support, and for Europe to grant policy without Hungary continually vetoing motions (invariably in support of Russia).

Viktor Orbán has been a totemic figure of the the nationalist right for the last 16 years – he came to power when more recent right wing nationalists were nowhere to be seen (Trump was a real estate developer, Giorgia Meloni an obscure junior minister, Marine Le Pen and Nigel Farage just fringe wannabes).

Only last week, JD Vance was sent by Trump to voice the US’ very public support of Orbán and his regime – so, one suspects Trump (and Putin) will be applying pressure to Péter Magyar’s new government at every opportunity over the coming months.

Hungary’s new government will have to unpick 16 years of endemic state corruption, and an undeniable reliance on Russia for energy security – roughly 75% of Hungary’s natural gas, up to 80% of its oil, and all of its nuclear fuel comes from Russia.

In other news (indirectly related to the closure of the Strait of Hormuz), Israel’s courts have agreed (again) to cancel the latest set of hearings that had been scheduled for Benjamin Netanyahu’s testimony in his corruption trial.

Hearings in Netanyahu’s trial (along with many other criminal proceedings), were suspended at the war’s outset due to the courts being placed on “an emergency footing”.

Monthly Day-Ahead Averages for the month so far are holding steady at 121p/therm (or 4.1p/kwh exc. non-gas).

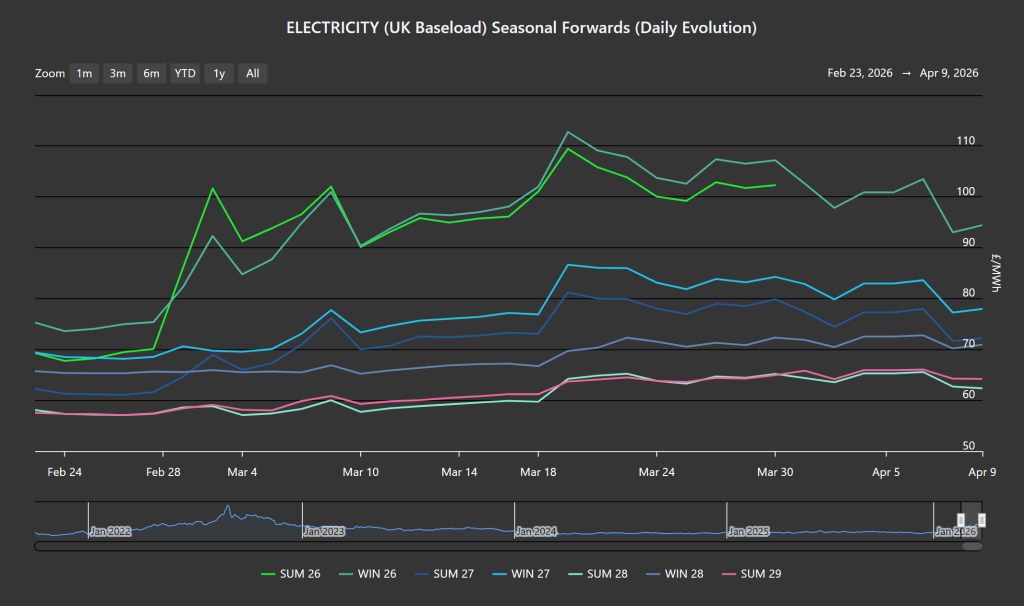

ELECTRICITY & CARBON

The Evolution chart below shows how Seasonal Forwards have behaved since the US/Israeli offensive began on 28th Feb ’26.

Thankfully, UK electricity prices remain at a significant discount versus gas prices (given summer conditions/improved renewables outputs/falling gas-for-power burn).

On the Carbon side of things, Dec-26 UKA delivery remains uncoupled from gas volatility with prices touching levels that are 31% below those printed in mid-Jan amid fears that Trump’s war on Iran is slowing global economies (and, in so doing, Industrial outputs).

At the time of writing, UKA mid-price Dec ’26 delivery is at £43.32/tn (and the spot is at mid-42s).

Since the US/Israeli offensive began, gas price falls are met with rising UKAs (and vice versa).

Monthly Day-Ahead Averages for UK electricity for the month have risen over the weekend to £94/mwh (or 9.4p/kwh exc. non-energy).