You’d be forgiven for thinking that prices would be back up this morning following the re-closure of the Strait of Hormuz over the weekend – but, noise aside, prices are holding onto last week’s slide.

By way of a quick recap – toward the end of last week, prices dropped in response to the Israel-Lebanon ceasefire announcement.

Then on Friday, the Strait of Hormuz was re-opened for the remaining period of the US-Iran ceasefire – at which point prices fell further toward the end of Friday’s session.

Then over the weekend, it turned out that the US weren’t prepared to end their blockade, and so Iran announced the re-closure of the Strait of Hormuz and started bombing Indian LNG vessels as they attempted to cross the waterway.

After which, all the other LNG vessels, which had just begun their transit of the increasingly unpredicatble shipping route, hastily u-turned their vessels and returned to square one – which is where we are this morning.

And yet, prices are lower now than they were before Iran re-opened the Strait on Friday – but why?

Well, it’s likely market participants have been waiting to hear this morning if Iran intends to show-up for the latest round of Islamabad talks.

Unfortunately, it’s now been confirmed that Iran has no plans to send negotiators to Islamabad – and so, we expect for prices to drift northwards over this afternoon’s session, with only 48-hours remaining of the US-Iran ceasefire.

Not surprisingly, Trump has resorted to venting his frustrations on Truth Social stating (sic): “Iran decided to fire bullets yesterday in the Strait of Hormuz — A Total Violation of our Ceasefire Agreement! Many of them were aimed at a French Ship, and a Freighter from the United Kingdom. That wasn’t nice, was it? My Representatives are going to Islamabad, Pakistan — They will be there tomorrow evening, for Negotiations. Iran recently announced that they were closing the Strait, which is strange, because our BLOCKADE has already closed it. They’re helping us without knowing, and they are the ones that lose with the closed passage, $500 Million Dollars a day! The United States loses nothing. In fact, many Ships are headed, right now, to the U.S., Texas, Louisiana, and Alaska, to load up, compliments of the IRGC, always wanting to be “the tough guy!” We’re offering a very fair and reasonable DEAL, and I hope they take it because, if they don’t, the United States is going to knock out every single Power Plant, and every single Bridge, in Iran. NO MORE MR. NICE GUY! They’ll come down fast, they’ll come down easy and, if they don’t take the DEAL, it will be my Honor to do what has to be done, which should have been done to Iran, by other Presidents, for the last 47 years. IT’S TIME FOR THE IRAN KILLING MACHINE TO END! President DONALD J. TRUMP”

Fundamentally speaking, European gas fullness levels crossed above the 30% mark over the weekend – though Norwegian gas production is expected to decline this week due to scheduled summer maintenance.

In other news, the European Commission is expected to unveil emergency measures related to the energy crisis on Wednesday – details are patchy at this time, though it’s expected the scheme will encourage remote home working whilst offering transport subsidies.

On the trading side, FLEX clients are all but closed-out for May in the hopes that, come June, the Strait will be re-open and essential LNG transit will have been restored – thereafter, low summer Day-Ahead prices will resume.

For now, however, the jury is out pending what happens when the US-Iran ceasefire comes to an end on Wednesday.

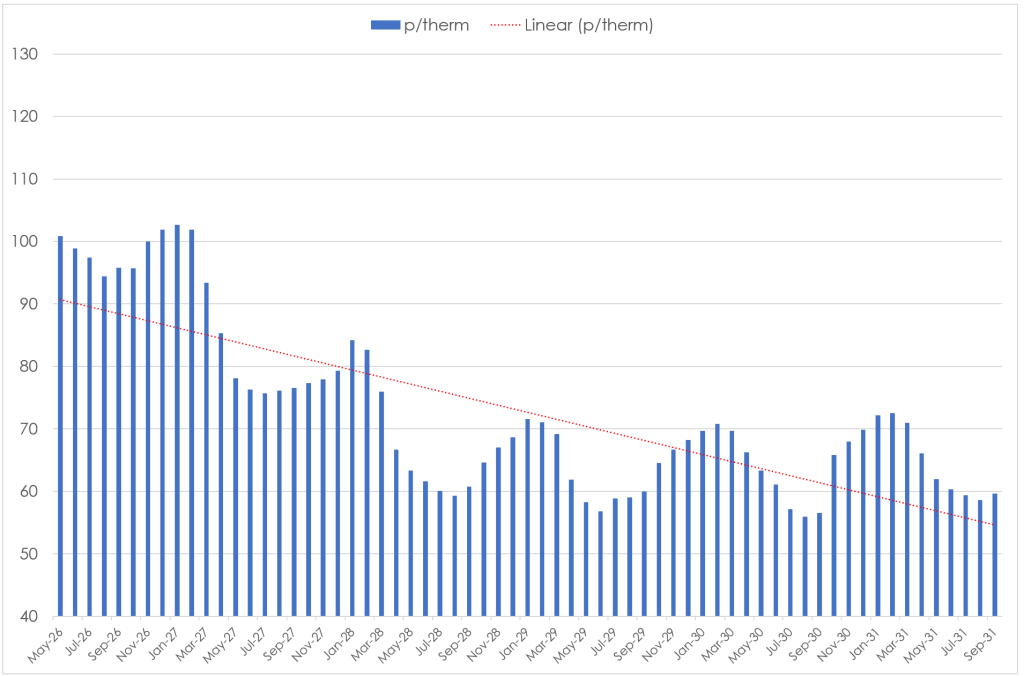

The chart below shows Friday’s closing Monthly Forward prices – notably, the Balance of Summer ’26 and Winter ’26 are doing their best to break below 100p/therm.

Monthly Day-Ahead Averages for the month so far continue to slide week-on-week – now at 114 p/therm (or 3.9 p/kwh exc. non-gas).

ELECTRICITY & CARBON

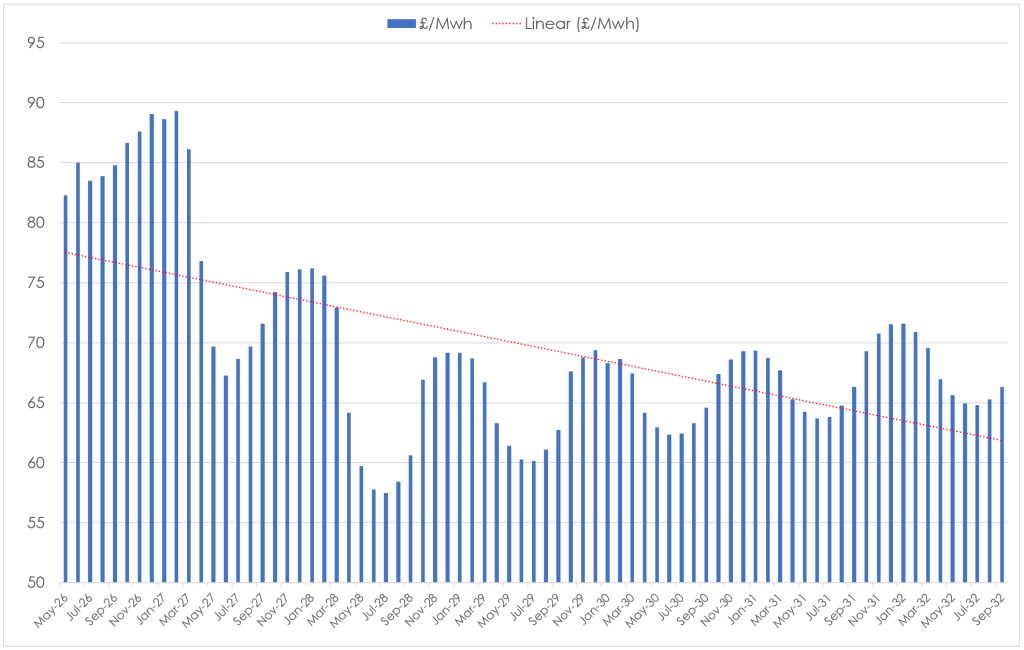

The chart below shows Friday’s closing Monthly Forward prices – notably, the Balance of Summer ’26 and Winter ’26 all closed back below £90/mwh.

Clearly, markets remain backwardated (future delivery prices discounted versus near-term delivery prices) – reflecting an underlying sentiment amongst market participants that conditions are expected to improve further down the ‘curve’.

On the Carbon side of things, Dec-26 UKA delivery remains inversely correlated to gas markets – when gas prices fall, UKAs rise (and vice versa).

At the time of writing, UKA mid-price Dec ’26 delivery is at £50.86/tn (and the spot is at mid-49s).

Monthly Day-Ahead Averages for UK electricity for the month have fallen again to £89/mwh (or 8.9 p/kwh exc. non-energy).