Once again, the pendulum looks set to swing in favour of the bulls.

Underlying sentiment amongst market participants as the week progresses is increasingly despondent/frustrated/resigned.

When Iran relented last Friday and agreed to re-open the Strait (pending the outcome of further peace negotiations), the US opted instead to keep the blockade.

Thereafter, the Iranian regime reasserted their grip on the waterway, and the US has further bolstered its blockade with almost daily arrivals of additional warships.

Right now, there are 21 US warships in the Gulf, with another 7 on the way – 12 warships are being used to blockade the Strait.

The US has seized Iranian ships, and Iran is attacking ships linked to US/Israel.

What’s increasingly evident is that Trump is in no rush to re-open the Strait.

As a net-exporter of oil and LNG, the US is relatively insulated (other than higher gasoline prices).

If anything, the US stands to profit financially from the Strait’s ongoing closure (with the cost of LNG likely to rise, the longer the Strait is closed).

Meanwhile, Asian and European economies will suffer and weaken – the Strait ordinarily handles roughly 20% of global daily oil distribution, 20% of global LNG transit (primarily from Qatar), refined oil products, petrochemicals (like methanol, naphtha, and ethylene for plastics), around a half of global sulfur (used in agriculture and mining), about a third of global fertilizer distribution (including urea, potash, and ammonia).

For Gulf states, the Strait is used to import food, medicines, and essential industrial components.

Of course, Trump’s Administration has made no secret of their protectionist agenda since he returned to office in Jan ’25.

From Jan to Apr ’25, the overall average effective US tariff rate rose from 2.5% to around 27%—the highest level in over a century.

Trump’s aim with tariffs was to ultimately boost the US economy whilst weakening the economies of perceived adversaries (China/Europe/Venezuela/Canada).

Lest we forget, China’s economy was already battling slower growth, falling industrial outputs, a real estate collapse, and rising unemployment when Trump’s tariffs began.

Whilst the US/Israel offensive has only been running for just under two months, pressure is nonetheless being felt on factory orders, costs, and jobs across Asia – primarily across China.

It’s true that over the last few years, China has built up significant oil reserves, and undoubtedly leads the world in renewables capabilities/outputs.

But Trump’s closure of the Strait of Hormuz is adding to the woes of China’s sluggish economy – with export costs rising day-on-day.

The slowly dawning fear then amongst traders, is that Trump’s closure of the Strait of Hormuz might be the end-game in itself.

For now, there’s no sign that the Strait will re-open anytime soon – the Pentagon has stated this morning that clearing the waterway of Iranian mines could take six months.

If its Trump’s intention that the waterway be closed indefinitely so as to serve his political objectives, who is going to stand in his way (considering that 28 US warships will be protecting the blockade)?

Not surprisingly, off the back of today’s despondency/frustration/resignation, prices all the way down the curve are up by approximately 5%.

On the trading side, FLEX clients are all but closed-out for May in the hopes that, come June, the Strait will re-open and essential LNG transit will have been restored.

For now, however, it’s increasingly difficult to see just how/when the impasse can be overcome.

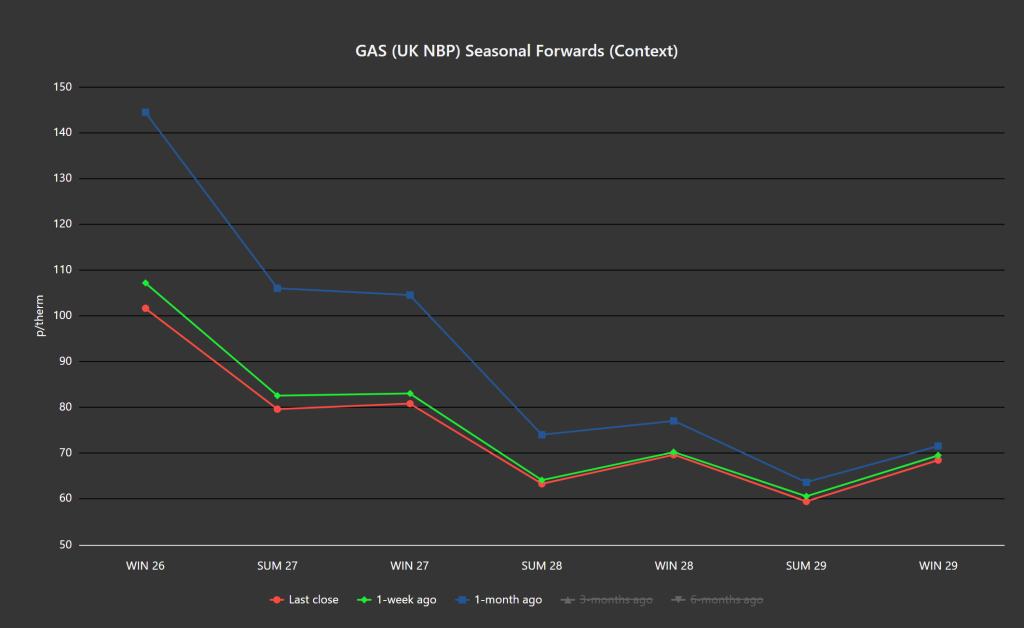

Monthly Day-Ahead Averages for the month remain at 113 p/therm (or 3.9 p/kwh exc. non-gas).

ELECTRICITY & CARBON

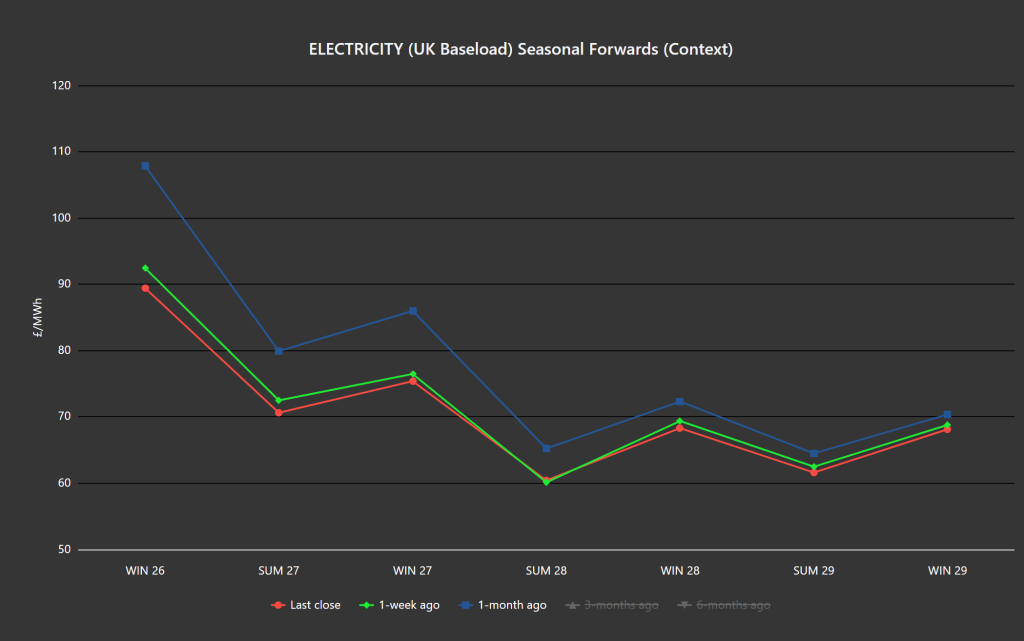

UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb.

Suffice as to say, given summer conditions (improved renewables/lower gas for power burn), UK electricity prices remain comfortably below the psychological level of £100/mwh.

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 52%, thermal at 5% (gas and coal) and low carbon at 28% (nuclear and imports).

On the trading side, FLEX clients are all but closed-out for May in the hopes that, come June, the Strait will re-open and essential LNG transit will have been restored.

For now, however, it’s increasingly difficult to see just how/when the impasse can be overcome.

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets – so when gas prices fell, UKAs rose (and vice versa).

However, given this week’s volatility in UKAs, having fallen £3/tn on Tuesday, we increasingly see a correlation with equities/stock-indices.

At the time of writing, UKA mid-price Dec ’26 delivery is at £48.53/tn (and the spot is at mid-47s).

Monthly Day-Ahead Averages for UK electricity for the month remain at £88/mwh (or 8.8 p/kwh exc. non-energy).