It’s widely known that the acronym TACO has been attributed to Trump since he began his second term back in Jan-25 – Trump Always Chickens Out.

To be fair to Trump, this acronym in not entirely accurate – though of course he is inclined to pivot/change his approach from time to time.

As of this week, there’s a new acronym doing the rounds across trading floors around the globe – NACHO (Not A Chance Hormuz Opens).

As of yesterday afternoon, the US Administration has been forced to come clean – they’re floundering.

Prices began to look increasingly supported yesterday after Trump rejected an Iranian proposal to reopen the Strait of Hormuz subject to the US ending the blockade/siege.

Trump is now pushing for other countries (the hitherto allies that he’s been berating this last few weeks) to form an international coalition to restore “freedom of navigation” across the Strait of Hormuz.

This morning, oil prices have surged past £125/barrel amid confirmations that Trump will receive a briefing today on plans for a series of fresh military strikes on Iran (by way of cajoling the regime to play ball).

And so it’s as you were – diplomacy has failed, and a re-escalation of hostilities looks imminent (that will no doubt induce retaliatory strikes on the part of Iran on their close neighbours’ key energy infrastructure).

Fundamentally speaking, European storage fullness is at 32% versus the 5-year average of 43% – so not too far off the pace, and no need for panic stations just yet.

On the trading side, FLEX clients are all but closed-out for May in the hopes that, come June, the Strait will re-open and essential LNG transit will have been restored.

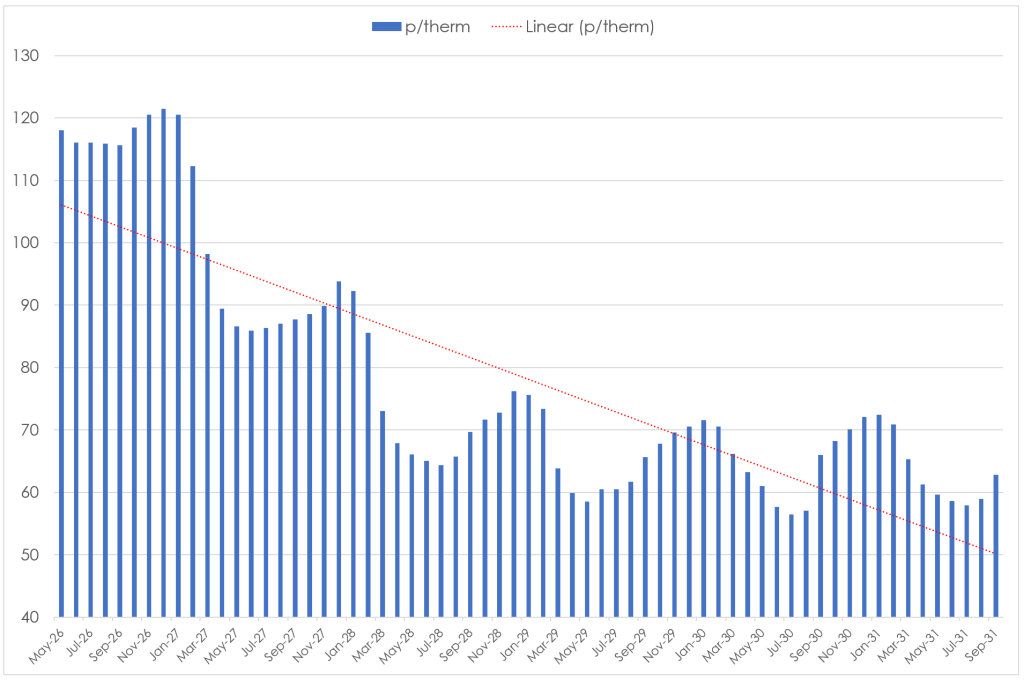

Monthly Day-Ahead Averages for the month remain are holding steady at 113 p/therm (or 3.9 p/kwh exc. non-gas).

ELECTRICITY & CARBON

By way of a concerted effort to mitigate the impact of surging fuel and fertilizer prices caused by the US/Israeli offensive, the EU chose to adopt a new policy this week (METSAF).

The scheme (Middle East Crisis Temporary State Aid Framework) will allow EU member states to support those sectors most heavily affected – primarily agriculture, fisheries, non-aviation transport (road, rail, inland waterways), and energy-intensive industries.

The subsidies will be made available until the end of ’26 – energy-intensive industries can be compensated by up to 70% for additional fuel and fertilizer costs.

In addition, a simplified option will be made available for smaller beneficiaries to receive up to €50,000 without providing detailed, individual consumption data (which will no doubt will vulnerable to fraudulent applications, as was the case with rescue packages offered during the ’22 crisis).

Thankfully, UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb.

Suffice as to say, given summer conditions (improved renewables/lower gas for power burn), UK electricity prices remain comfortably below the psychological level of £100/mwh.

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 66%, thermal at 3% (gas and coal) and low carbon at 22% (nuclear and imports).

On the trading side, FLEX clients are all but closed-out for May in the hopes that, come June, the Strait will re-open and essential LNG transit will have been restored.

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets – so when gas prices fell, UKAs rose (and vice versa).

However, correlation has now seemingly shifted to equities, which continue to enjoy a strong, tech-led rally.

At the time of writing, UKA mid-price Dec ’26 delivery is at £49.50/tn (and the spot is at mid-48s).

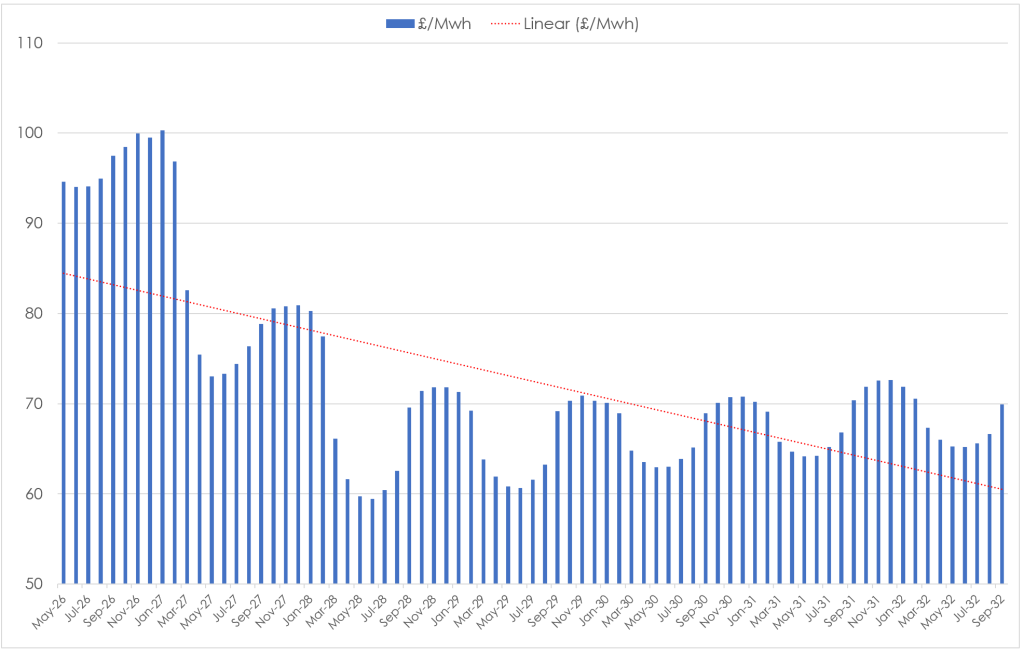

Monthly Day-Ahead Averages for UK electricity for the month have dropped to £86/mwh (or 8.6 p/kwh exc. non-energy) off the back of high renewables outputs.