Near-term delivery prices fell below 100p/therm yesterday lunchtime amid headlines that an MoU (Memorandum of Understanding) to end the war was close to being agreed between the US and Iran.

However, shortly thereafter, it came to light that Iran had launched a website confirming the establishment of the “Persian Gulf Strait Authority” designed to collect tolls from ships transiting the notorious waterway!

Not surprisingly, panic ensued, and prices rose hastily to reflect reinstated risk-premia.

As of today, Iran is reviewing the US-driven memo/proposal, which omits hitherto key US demands relating to the ending of Iran’s nuclear programme and the fate of stockpiles of enriched uranium – and so represents a reluctant climb-down on Trump’s part.

Were it to come to pass, the proposed framework would unfold in three stages – 1)formally ending the war 2)resolving the crisis in the Strait of Hormuz then 3) launching a 30-day window for negotiations on a broader agreement.

All variables considered, I don’t think it’s unbalanced to suggest that whilst Trump is “optimistic” (casting around desperately for an off-ramp), Tehran is “skeptical” (not casting around desperately for an off-ramp).

Whilst it’s true to say that the US has benefitted from the crisis to date (as a net exporter of fossil fuels not dependent on the Strait for either import or export), it’s also true that, politically, Trump is running out of road.

He told reporters at the White House yesterday, “they want to make a deal… it’s very possible…it’ll be over quickly.”

Meanwhile, Israel renewed its attacks on Beirut for the first time since the ceasefire there was agreed last month – this despite a halt to Israeli strikes being a key Iranian demand should Trump wish to reach agrement with Tehran.

And so, not surprisingly to the rest of the world, an Iranian lawmaker (Ebrahim Rezaei) has described the MoU as “more of an American wish list than a reality.”

In addition, Mohammad Baqer Qalibaf (Iran’s Parliament Speaker) has mocked reports that suggested an agreement was close, by writing on social media that “Operation Trust Me Bro failed” and portraying the talks as no more than US spin after its failure to reopen the waterway (with Trump’s one-day old “Operation Freedom” put on the backburner very quickly).

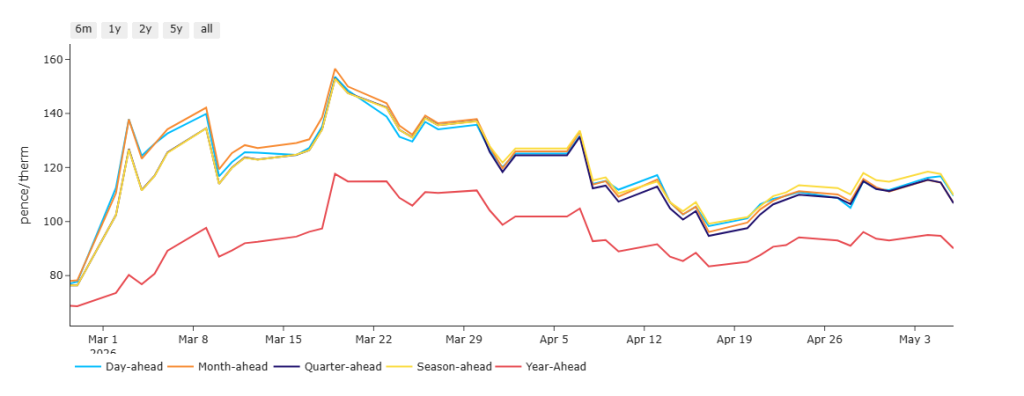

All noise aside, near-term delivery prices (Day-Ahead/Month-Ahead/Quarter -Ahead/Season-Ahead) are more than 25% lower than they were back on 19th March at the height of the crisis – please see chart below.

Fundamentally speaking, European storage fullness is at 34% versus the 5-year average of 45% – so not too far off the pace, and no need for panic stations (yet).

On the trading side, the immediate challenge facing some FLEX clients is June delivery – traders will be looking to buy dips as the month progresses.

Monthly Day-Ahead Averages for the month so far are drifting marginally lower at 112p/therm (or 3.82 p/kwh exc. non-gas).

ELECTRICITY & CARBON

Thankfully, UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb.

Suffice as to say, given summer conditions (improved renewables/lower gas for power burn), UK electricity prices remain (in the main) below the psychological level of £100/mwh.

Today’s UK electricity generation mix is neutral in nature (neither a bullish, not bearish driver) – specifically, renewables are contributing 35%, thermal at 32% (gas and coal) and low carbon at 20% (nuclear and imports).

On the trading side, the immediate challenge facing some FLEX clients’ is June delivery – traders will be looking to buy dips as the month progresses.

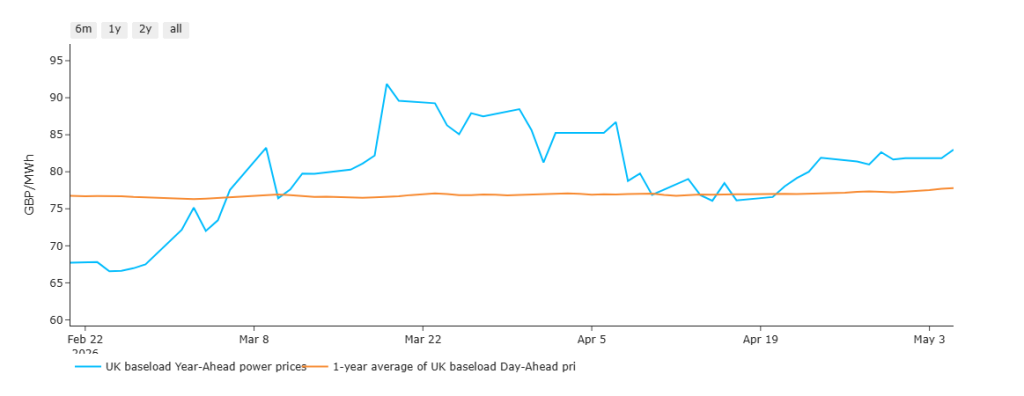

The chart below details UK electricity Year-Ahead prices versus the 1-Year Average of Day-Ahead prices since the US/Israeli offensive began back on 28th Feb.

By way of explantion, when the blue line is above the orange line, mid-term delivery prices are at a premium to an average of the last 12 months.

As you can see, prior to the onset of the US/Israeli offensive, prices were enjoying a soft-landing heading into Summer-26 – thereafter, Year-Ahead has remained consistently at a premium despite the otherwise ‘summery’ conditions.

Whilst the blue line remains above the orange line, it’s fair to conclude that prices are not as good as they should be (were it not for bullish geopolitical drivers).

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets.

However, correlation has now seemingly shifted to equities, which continue to enjoy a strong, tech-led rally.

At the time of writing, UKA mid-price Dec ’26 delivery is at £48.53/tn (and the spot is at mid-47s).

Monthly Day-Ahead Averages for May so far are at £105/mwh (or 10.5 p/kwh exc. non-energy) – so little changed since the start of the month.