Yesterday, Trump used his Truth Social platform to air his feelings toward Iran’s response to his most recent peace proposal, “I don’t like it. TOTALLY UNACCEPTABLE.”

Last week, on Thursday, it looked as though investment funds were selling their long positions in TTF (European gas benchmark) amid rumours that a peace deal was all but done.

By way of further evidence, the CAL-27 TTF benchmark fell back below its 20-day moving average – unfortunately, prices have this morning climbed back above that same 20-day moving average – reflecting a renewed interest on the part of speculators in a bullish resurgence.

And so, it’s as you were – yet again.

If Trump is privately worried about his plummeting approval ratings in the US, and with the standing of the US on the global geopolitical stage, he isn’t showing it.

Week-after-week, month-after-month, he seems content to bumble along, acting with surprise when Iran once again rejects his re-phrased maximalist demands.

No doubt this week, he’ll reiterate both to Congress, and to the world’s press, that Iran is finished, and that the war has ended – but still the Strait of Hormuz will remain closed to oil/LNG transit.

Brent Crude is back up to $107/barrel.

European storage fullness is at 35% versus the 5-year average of 47% – so a little more adrift than it’s been since the heating season came to an end last month.

In short, time is running out for Europe/the UK – we need the Strait to open so that plentiful global supply can lessen the pressure on our efforts to replenish storage over the coming months.

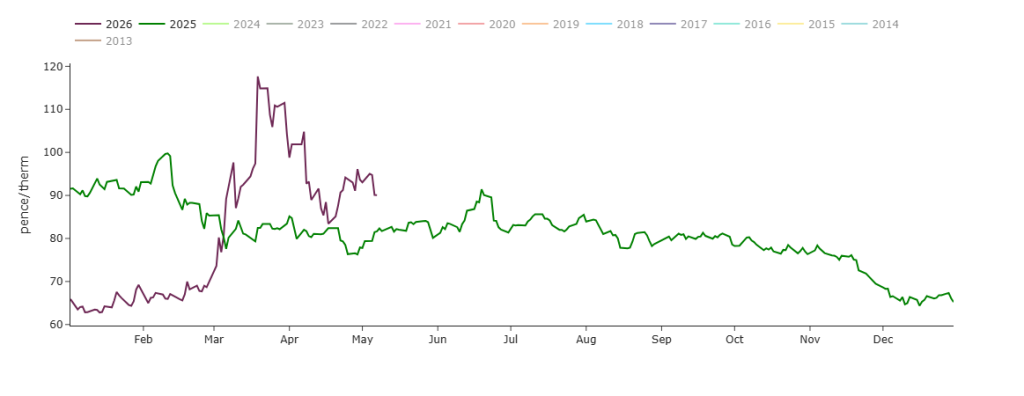

The chart below details the daily evolution of Year-Ahead UK gas prices for 2025, and 2026 so far.

As you can see, prices trailed-off nicely in the last quarter of 2025 amid talk of an LNG glut come Summer-26.

The year started low, well below 2025 Year-Ahead numbers for the same period, until late Feb when the US/Israeli offensive began.

Thereafter, Year-Ahead prices remain above 2025 for the same period – a reflection that prices remain elevated, and that value (consistent with fundamentals) has yet to return.

Encouragingly, Norwegian gas flows to the UK/Europe remain above the 5‑day moving average, despite Norway’s Hammerfest LNG facility going offline on Friday due to process issues (the outage is expected to last until 13th May).

Bizarrely, the first Qatari LNG vessel has successfully passed through the Strait of Hormuz and is enroute to offload in Pakistan – though this can only be viewed as a cynical gesture on the part of the regime, highlighting their power to sanction transit at will.

On the trading side, the immediate challenge facing some FLEX clients is June delivery – traders will be looking to buy dips as the month progresses (please watch this space).

Monthly Day-Ahead Averages for the month so far are holding steady at 112p/therm (or 3.82 p/kwh exc. non-gas).

ELECTRICITY & CARBON

Thankfully, UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb.

Suffice as to say, given summer conditions (improved renewables/lower gas for power burn), UK electricity prices remain below the psychological level of £100/mwh.

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 47%, thermal at 16% (gas and coal) and low carbon at 18% (nuclear and imports).

On the trading side, the immediate challenge facing some FLEX clients is June delivery – traders will be looking to buy dips as the month progresses (please watch this space).

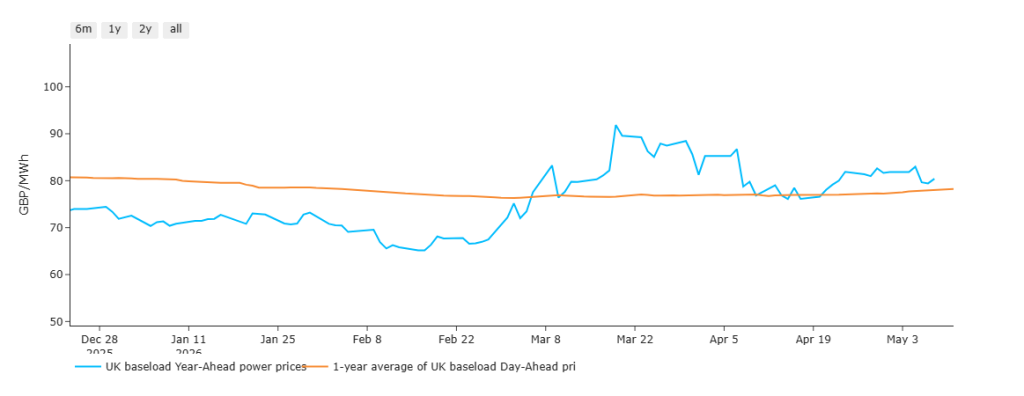

The chart below details UK electricity Year-Ahead prices versus the 1-Year Average of Day-Ahead prices since the US/Israeli offensive began back on 28th Feb.

By way of explantion, when the blue line is above the orange line, mid-term delivery prices are at a premium to an average of the last 12 months.

As you can see, prior to the onset of the US/Israeli offensive, prices were enjoying a soft-landing heading into Summer-26 – thereafter, Year-Ahead has remained consistently at a premium despite the otherwise ‘summery’ conditions.

Whilst the blue line remains above the orange line, it’s fair to conclude that prices are not as good as they should be (were it not for bullish geopolitical drivers).

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets.

However, correlation has now seemingly shifted to equities, which continue to enjoy a strong, tech-led rally.

Notably, a high‑level roundtable discussion will take place in Brussels tomorrow, bringing together key EUETS industry sectors and selected stakeholders to inform the upcoming reforms – investment funds/speculators will extend their long positions if the reforms mean scarcer allowances.

At the time of writing, UKA mid-price Dec ’26 delivery is at £52.74/tn (and the spot is at mid-51s).

Monthly Day-Ahead Averages for May so far are lower on the week at £102/mwh (or 10.2 p/kwh exc. non-energy).