All eyes are the Trump/Xi summit in China this week.

Hopes persist that China will, in some way, help the US to bring the impasse with Iran to an end.

Despite the ongoing closure of the Strait of Hormuz, natural gas is still way cheaper versus the 2022 Russia crisis.

This is primarily due to a significantly reduced EU reliance on Gulf exports, as well as Asia’s willingness to pivot to renewables & coal in the face of shortages.

But as spring temperatures make way for deeper summer conditions, demand across Asia for HVAC will likely increase, and panic stations could set in.

Benchmark Brent Crude is at $109 – so around 10% down versus this week’s highs.

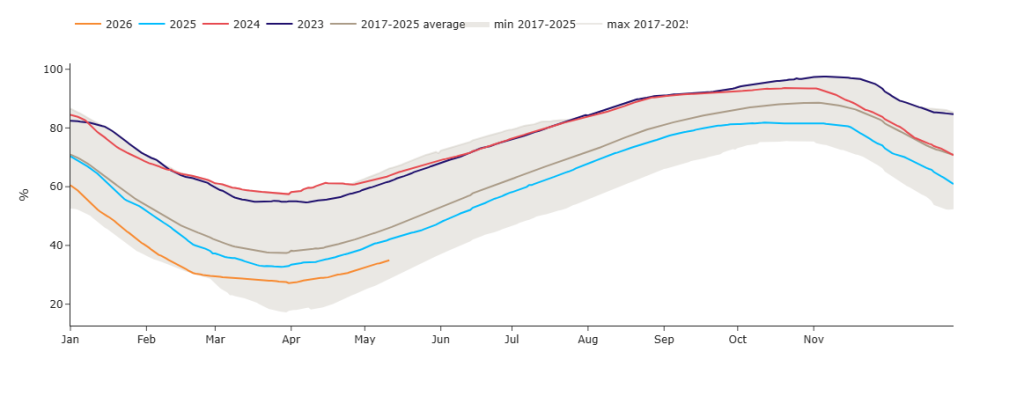

European storage is at 36% versus the 5-year average of 44% – so inventories are rising slowly but surely, amid thankfully low demand and solid renewables outputs (please see Europe Gas Stock Fullness Rates below).

On the trading side, the immediate challenge facing some FLEX clients is June delivery – traders will be looking to buy dips as the month progresses (please watch this space).

Monthly Day-Ahead Averages for the month so far are holding steady at 112p/therm (or 3.82 p/kwh exc. non-gas).

ELECTRICITY & CARBON

UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb.

Suffice as to say, given summer conditions (improved renewables/lower gas for power burn), UK electricity prices remain below the psychological level of £100/mwh (in the main).

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 51%, thermal at 13% (gas and coal) and low carbon at 21% (nuclear and imports).

On the trading side, the immediate challenge facing some FLEX clients is June delivery – traders will be looking to buy dips as the month progresses (please watch this space).

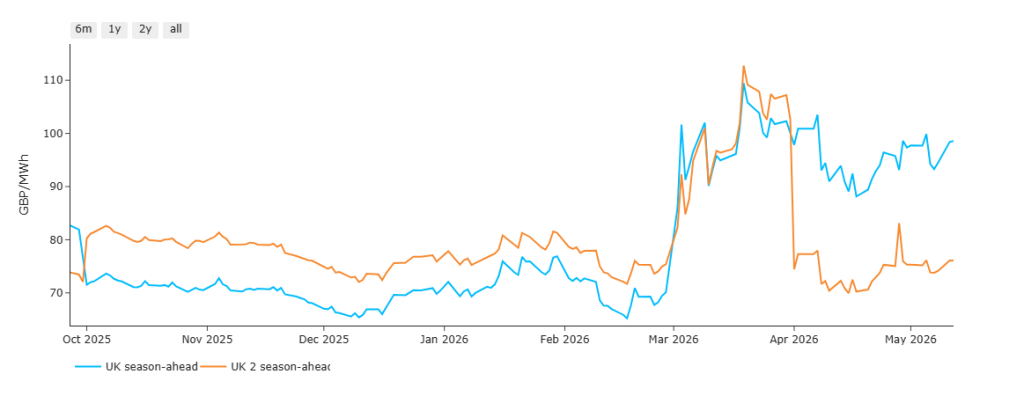

The chart below details UK electricity Season-Ahead prices (blue line) versus 2-Seasons-Ahead prices (orange line).

By way of explanation, at the outset of any respective summer (beginning 1st April) or winter (beginning 1st October), one would expect for the lines to re-cross to reflect higher priced winters than summers (as is the traditional shape).

Notably (and anomalously), on 28th Feb when the US/Israeli offensive began, the two lines diverged and spiked northwards – reflecting short-term panic that closure of the Strait of Hormuz would mean high prices indefinitely.

Thereafter, beginning 1st April, normal price-action resumed and, as you’d expect during the summer months, the orange line is back comfortably below the blue line – reflecting an underlying belief amongst market participants that prevailing geopolitical impacts will not affect Summer-27 (but Winter-26 is looking shaky).

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets.

However, correlation has now seemingly shifted to equities, which continue to enjoy a strong, tech-led rally.

At the time of writing, UKA mid-price Dec ’26 delivery is at £51.59/tn (and the spot is at early-50s).

Monthly Day-Ahead Averages for UK electricity for May so far are holding steady at £102/mwh (or 10.2 p/kwh exc. non-energy).