The impasse persists, and real-world physical shortages are now only weeks away.

Prior to the ceasefire beginning early April, the US/Israeli offensive killed thousands across Iran.

Israel has also killed thousands more across Lebanon, which (ostensibly) it invaded by way of pursuing the Hezbollah militia (backed by Iran).

To date, the ceasefire has just about held (though Israel continues to bomb and occupy with a stated aim of ensuring their borders remain protected in the face of existential threat).

Early May also brought sporadic attacks on shipping and on Gulf states in response to Trump’s “Project Freedom” with a stated aim of reopening the Strait – then Trump pulled the plan after only a day or so.

This week has seen drone attacks on Saudi Arabia and the UAE allegedly coming out of Iraq (where militia aligned with Iran are known to operate).

Then, Jordan reported shooting down a drone this morning.

Back in February, Trump and Netanyahu stated their war aims as curbing Iran’s support for regional militias, dismantling its nuclear programme, destroying its missile capabilities, and ultimately making it easier for Iranians to topple the regime from within.

Fast forward 82 days later, Iran retains its stockpile of (very nearly) weapons-grade enriched uranium, as well as its ability to threaten neighbours with missiles, drones, and proxy militias.

The regime, having brutally suppressed a mass uprising at the start of the year, has faced zero sign of any organised opposition from a terrified population since the US/Israeli offensive began.

So, mission accomplished? Not even close.

If anything, those original stated aims are barely mentioned these days – instead, it’s all about the Strait of Hormuz and Iran’s strangle-hold on the global economy.

It’s become clear in the last few days that Iran is enforcing a multi-tiered system for clearing vessels through the Strait of Hormuz.

The US has (rather unhelpfully) warned against complying with Iran’s controls – nonetheless, some shippers and governments are taking the risk.

Iran continues to threaten war ‘beyond the region’ if the US attacks again as Trump continues to threaten (amid his announcements that the war is due to end).

Surprisingly, the US Senate yesterday has successfully advanced anti-Iran war measures in an unexpected blow to Trump’s otherwise total control over his adversaries.

Senator Bill Cassidy, who lost his primary this weekend to one of Trump’s preferred Republican candidates, became the latest GOP (“Grand Ol’ Party”) defector and joined Democrats in taking advantage of Republican absences to advance a war powers resolution.

This week has seen significant volatility as traders/market participants are jumping in and out of trades on a daily basis – bizarrely, today is a marginally softer price day, despite the bullish rally to close yesterday’s session.

Most likely, yesterday’s increases were attributed to the onset of Norway’s pipeline maintenance season with capacity reductions to increase as the week progresses (the Troll field is scheduled to shut from today) – but thankfully the Asgard unscheduled outage looks set to end tomorrow.

Notably, despite Xi having hosted Trump’s visit to China last week with both sides lauding a “new bilateral relationship”, today it was Putin’s turn to visit his “dear friend” – however, rumours abound that Putin was unsuccessful in securing further advancement of his “Power of Siberia 2” pipeline that would bestow much needed additional revenues for Russia.

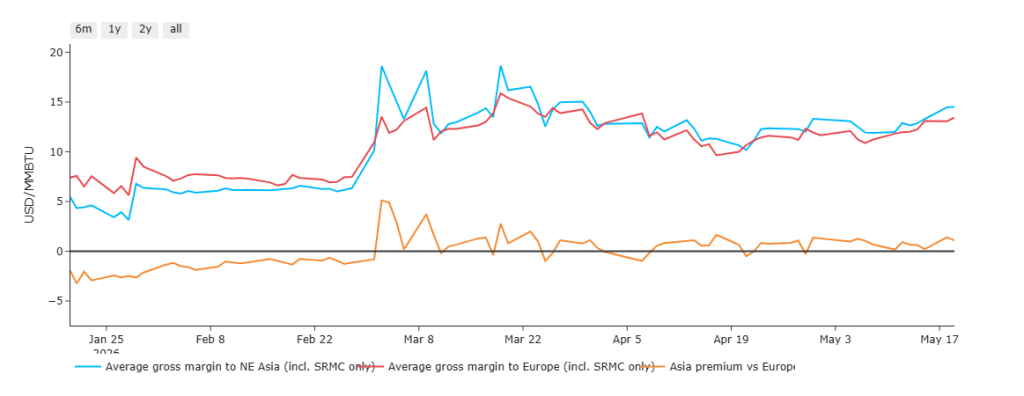

It’s also worth noting that (as per the chart below) following the onset of the Iran conflict, US-originated LNG vessels started making more money by heading to Asia than they did to Europe – so, it would be fair to conclude Xi is content to import from both the US and Russia whilst being seen to be the stabalising player across geopolitics these days.

At the time of writing, European/UK gas prices have softened versus this morning’s open.

Europe is forecast to enjoy significantly warmer temperatures over the coming days, with demand easing as a result.

Trump has unashamedly stated this morning again that the “war will end very soon” – we’ve lost count how many times he’s made these claims over the last 11 weeks or so.

Nonetheless, somebody must be listening, as front-month prices have dropped off 4p/therm versus yesterday’s close.

In conclusion then, the European gas balance is becoming a serious cause for concern.

Historically weak stock levels amid increased competition with Asia to attract LNG cargoes from the US (as illustrated below) cannot be ignored.

Ongoing Russian attacks on key gas facilities across Ukraine, further which complicates the filling of Ukrainian’s massive gas storage facilities, and will soon force Ukraine to rely more heavily on imports (inevitably from Europe) over Winter-26.

As such, despite today’s fall in prices, FLEX clients with open volumes for Jun-26 and beyond are being encouraged to consider mitigating exposure so as to avoid a worsening supply outlook over the coming days/weeks/months.

Across the UK, energy buyers have adopted a wait-and-see approach since the unexpected conflict disrupted what was to be a summer of soft prices and plentiful supply.

Unfortunately, time is running out for the Strait to re-open – and buyers should be aware that the upside risk is now greater than the downside potential (conditions that would ordinarily mean hedging is the safest approach, as opposed to leaing volumes to float).

Monthly Day-Ahead Averages for the month have crept up to 117p/therm (or 4 p/kwh exc. non-gas).

ELECTRICITY & CARBON

Whilst UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb, nonetheless, bulls are taking bites out of Winter-26 value.

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 62%, thermal at 8% (gas and coal) and low carbon at 17% (nuclear and imports).

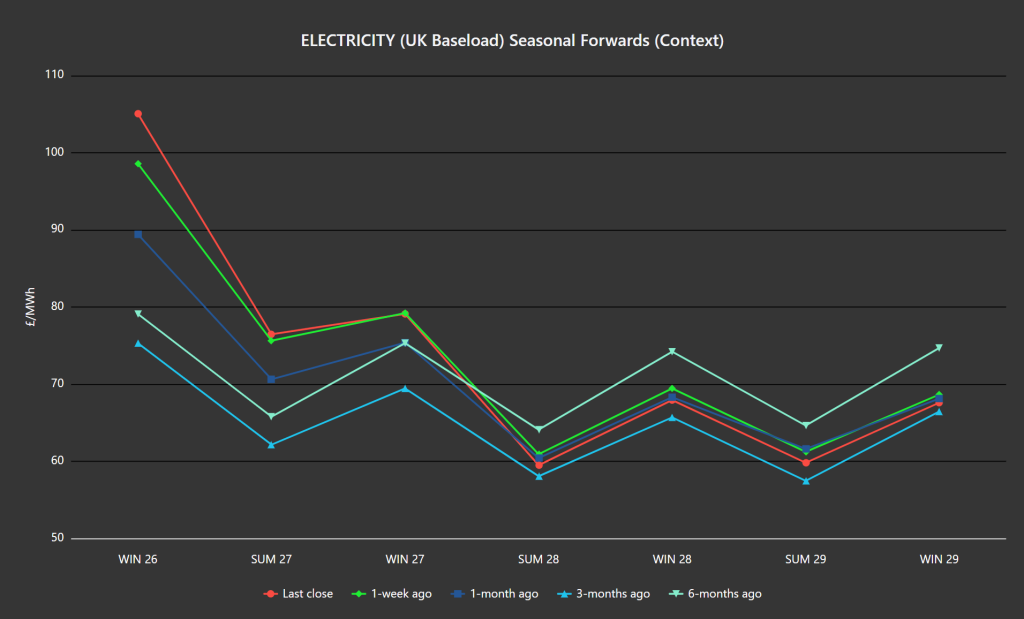

The chart below details Seasonal Forwards versus 1-week/1-month/3-months/6-months ago.

As you can see, the risk-premia is built into the front 3-Seasons – beyond which, prices are lower now than they were 1-week/1-month/6-months ago (but still higher than 3-months ago).

So it’s fair to say buyers are still able to access comparatively solid value beginning Summer-28.

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets.

However, correlation shifted to equities throughout March (which continue to enjoy a strong, tech-led upwards momentum).

At the time of writing, UKA mid-price Dec ’26 delivery is at £50.67/tn (and the spot is at mid-49s).

Monthly Day-Ahead Averages for UK electricity for May so far are holding steady at £101/mwh (or 10.1 p/kwh exc. non-energy).