As has become standard process, the US made its moves at the weekend whilst markets were closed.

Whilst soundbites coming out of the White House indicated we were “hours away” from a resolution, the US then launched “defensive” strikes on missile plaements across southern Iran.

The latest from Marco Rubio (US Secretary of State) is that finalising a deal could “take a few days”.

Interestingly, a more defined narrative is permeating the airwaves that it was in fact Israel that convinced the US as to the merits of starting the war – this amid Israeli right-wing ministers continuing to press Netanyahu to resume Beirut strikes to counter Hezbollah drone attacks.

Which begs the question, is the tail wagging the dog after all?

Certainly, any lasting accord that will mean the re-opening of the Strait will require that Israel steps off its permanent war-footing.

But can Netanyahu survive politically if Israel is forced to lay down its arms?

So, whilst volatility remains elevated, actual trading liquidity is slowly but surely on the up.

Without question, if the Strait re-opens, prices will drop to pre-war levels very quickly as replenishing storage should be fairly straightforward if supply routes can function unrestricted – European storge fullness is now at 38% versus the 5-year average of 48%, so totally salvageable if we can get the Strait opened in the coming couple of weeks.

On the weather side of things, Europe’s first major heatwave of the season is expected to last all week, with temperatures significantly above seasonal norms (including the UK) 🙂

This should release a little pressure from our system, with strong solar and supressed gas-for-power generation, offsetting the ongoing geopolitical uncertainties.

On the FLEX side, most clients are now heavily hedged for Jun-26 delivery so as to mitigate against the Trump Administration’s unpredictability.

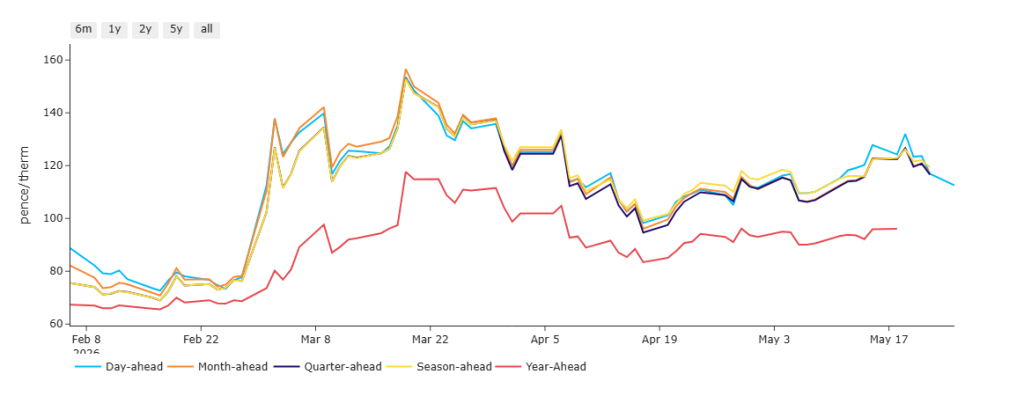

Monthly Day-Ahead Averages for the month are holding steady at 117p/therm (or 4 p/kwh exc. non-gas).

The ‘Prompt’ chart below shows the daily evolution of Day-Ahead/Month-Ahead/Quarter-Ahead/Season-Ahead/Year-Ahead.

As you can see, prices have failed to retest the highs of 19th Mar-26, and are reacting encouragingly to the latest rumours of a deal that will mean the re-opening of the Strait.

We have all our fingers crossed for buyers, as the return of steady supply through the Strait will see a resumption of soft pricing all the way down the curve.

ELECTRICITY & CARBON

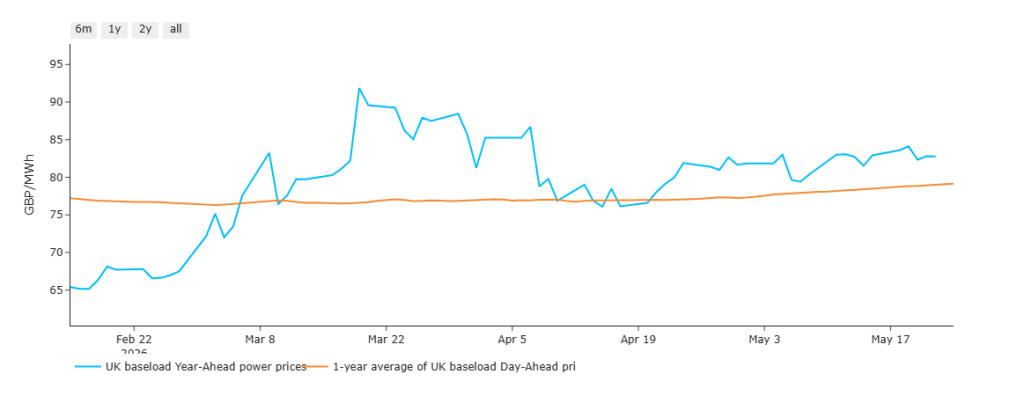

Whilst UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb, nonetheless, the last week has seen front end prices back above the psychological leel of £100/mwh.

Today’s UK electricity generation mix is neutral in nature, neither bullish nor bearish – specifically, renewables are contributing 33%, thermal at 26% (gas and coal) and low carbon at 23% (nuclear and imports).

The chart below details UK electricity Year-Ahead prices versus the 1-Year Average of Day-Ahead prices since the US/Israeli offensive began back on 28th Feb.

By way of explanation, when the blue line is above the orange line, mid-term delivery prices are at a premium to an average of the last 12 months.

We’ll be watching this dataset very closely in the event a deal is reached, as one would expect for the blue line to plunge beneth the orange line in short order thereafter – watch this space.

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets.

However, correlation shifted to equities throughout March (which continue to enjoy a strong, tech-led upwards momentum).

At the time of writing, UKA mid-price Dec ’26 delivery has sky-rocketed to £56.02/tn (and the spot is at mid-55s) – we believe this is a reaction to some very heavy institutional investing of EUAs on Friday.

We think the move strange amid high temperatures and suppressed thermal generation – and so we’d expect the move to be short-lived.

Monthly Day-Ahead Averages for UK electricity for May so far are holding steady at £101/mwh (or 10.1 p/kwh exc. non-energy).