On the FLEX side of things, we’ve waited longer this month (than previous months) to close out near-term delivery for clients amid an improving outlook (ongoing negotitions between the US and Iran/a reluctant concession on the part of Israel to curb hostilities/an increasing number of ships successfully transiting the Strait of Hormuz).

We’re told that Oman and Iran agreed yesterday to press on with discussions about the future administration of navigation in the Strait of Hormuz – though, for his part, US Secretary of State, Marco Rubio, said that Iran would not be able to charge tolls in the key waterway as part of any final agreement, reiterating that such an arrangement would violate international law.

Oil prices are down 39% versus April highs off the back of signs that more oil tankers stranded in the Gulf are scheduled to move out of the Strait of Hormuz over the coming days/weeks – while the number of idle LNG vessels in the Persian Gulf has risen in anticipation of safe transit (at last!)

Ship-tracking data (Source:Vortexa and Kpler) shows that seven ballast QatarEnergy-controlled tankers moved west into the Gulf to reload between 11th to 22nd June – the first such journeys since 28th February.

Data also shows other empty LNG tankers are on their way to Qatar – QatarEnergy, which runs the world’s largest LNG facility in Ras Laffan, is now gearing up for a full return to normal operations “as soon as conditions in the Strait stabilize,” with production from unaffected sections of the plant expected to recover to typical levels within only a few weeks.

And so, prices across the board today look soft and liquid for the first time in many weeks (spreads between bids/offers are tight, trade volumes are constant).

On the supply side, European storage numbers are low, but not too far out of touch– fullness is now at 47% versus the 5-year average of 57%.

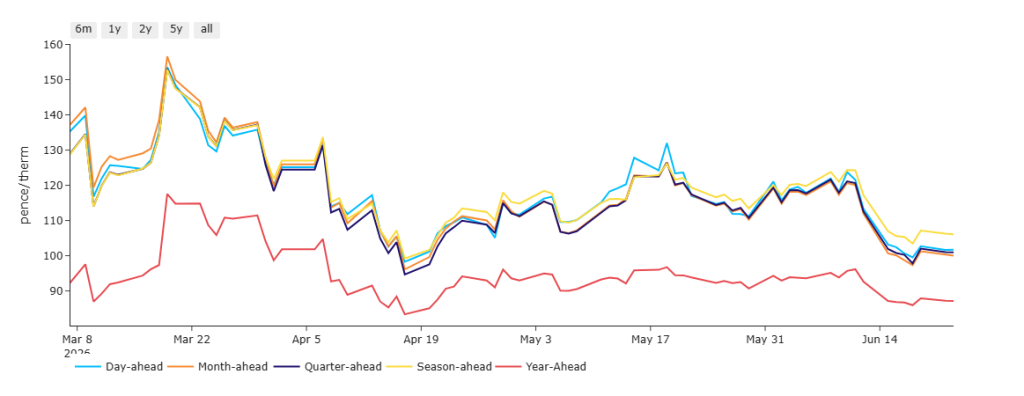

Monthly Day-Ahead Averages for June so far have fallen to 114 p/therm (or 3.9 p/kwh exc. non-gas).

As per the chart below, Day-Ahead prices are now comfortably below Season-Ahead prices (reflecting a meaningful reduction in short-term risk).

PLEASE NOTE, for any FLEX clients with open volumes for July, we’ll be in touch over the coming days with hedging rationale.

ELECTRICITY & CARBON

UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb – primarily due to summery conditions, solid renewables outputs (meaning lower gas-for-power generation).

Though today’s UK electricity generation mix is fairly neutral in nature – specifically, renewables are contributing 40%, thermal at 33% (gas and coal) and low carbon at 17% (nuclear and imports).

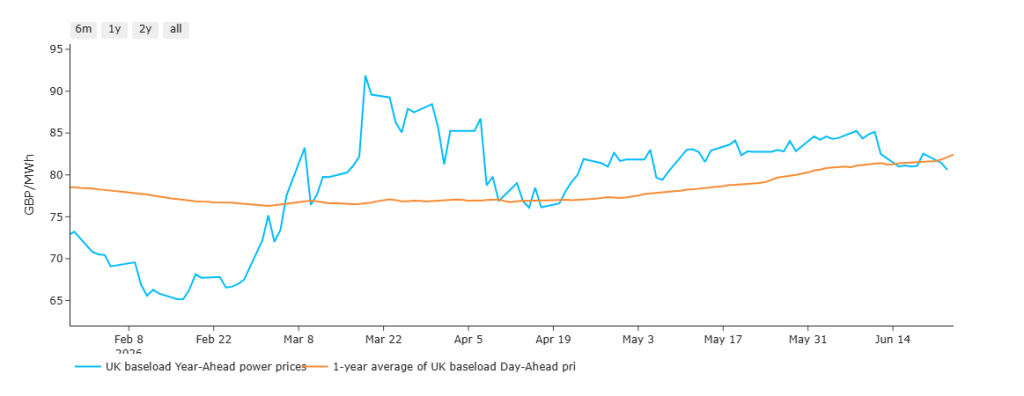

The chart below details UK electricity Year-Ahead prices versus the 1-Year Average of Day-Ahead prices since late-Feb.

By way of explanation, when the blue line is above the orange line, mid-term delivery prices are at a premium to an average of the last 12 months.

As you can see, prior to the onset of the US/Israeli offensive, prices were enjoying a soft-landing heading into Summer-26 – thereafter, Year-Ahead has remained consistently at a premium despite the otherwise ‘summery’ conditions.

However, in light of the improved outlook for the Gulf crisis, the blue line is back below the orange line and holding its ground (reflecting a significant shift in sentiment).

On the Carbon side of things, mid-price Dec-26 UKA delivery is at £56.35/tn (and the spot is at early 55s) mirroring softer gas prices.

PLEASE NOTE, for any FLEX clients with open volumes for July, we’ll be in touch over the coming days with hedging rationale.

UK electriity Monthly Day-Ahead Averages for June so far are holding steady at £92/mwh (or 9.2 p/kwh exc. non-energy).