As has become standard over the last couple of months, the weekend brought with it more market-moving geopolitical bullish momentum.

Traders began yet another week playing catch-up, with prices across the wider energy complex ‘gapping-up’ at market open.

This type of price action occurs when futures open higher than the previous session’s closing price, despite markets being closed over the weekend.

At market open, pre-placed buy orders overwhelmed sell orders, forcing the opening price to jump and leave a gap reflecting heightened volatility.

It’s worth pointing out that if you were you an individual with insider knowledge, and you wanted to ensure the success of a buy trade in the global energy markets come Monday morning, the best way to achieve this outcome would be to engage in warfare across the Middle East over the weekend (and/or ensure the closure of Strait of Hormuz)!

Gas has tracked oil higher today off the back of tit-for-tat airstrikes across the Gulf – not surprisingly, traffic through the Strait has once more ground to a halt.

As is often the case during periods of geopolitical disquiet, market participants become gloomy and more obsessively focussed on bullish fundamentals (at the expense of an otherwise balanced fundamental outlook).

And so, right now, fundamentals are adding additional support – European storage is at 52% versus the 5-year average of 64%; the continued summer-winter price inversion is not helping with storage injections (summer delivery prices are higher than winter forwards).

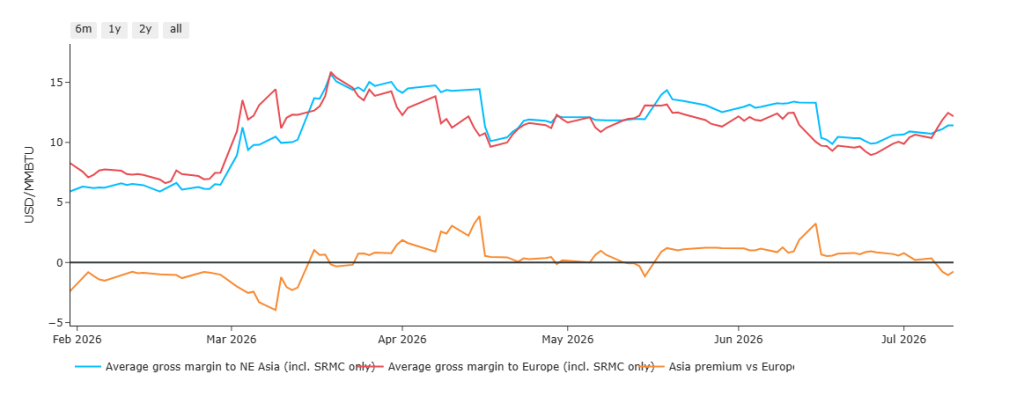

As further evidence of Europe’s increasingly desperate plight, the chart below shows how European’s prices have needed to rise again so as to lure US LNG cargoes away from Asia.

Notably, figures now confirm that Europe remained the primary destination for Russia’s Yamal LNG exports during the first half of 2026, this despite the EU announcing its intention (many times) over the last 12 months to wean itself off of Russian exports.

EU member states are estimated to have spent almost €6bn on Yamal cargoes – with France, Belgium and Spain receiving the lion’s share.

Of course, whilst the sustained flow of Russian LNG is helping to ensure European supply security, Ukraine is keen to point out that the EU is de facto supporting Putin’s war effort.

In other news, Norwegian exports are down today due to process issues at the Asgard field – whilst Norwegian exports had recovered following recent scheduled summer maintenance, we’re reminded just how sensitive prices can be to unscheduled outages during the scheduled maintenance season.

On the FLEX side of things, for clients with remaining near-term open volumes, we’ll look to advise on potential intraday dips and hedging opportunities over the coming days (though we don’t expect many, if any).

Monthly Day-Ahead Averages for July so far have jumped to 112 p/therm (or 3.8 p/kwh exc. non-gas).

ELECTRICITY & CARBON

UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb – primarily due to summery conditions, solid renewables outputs (meaning lower gas-for-power generation).

However, given the weekend’s renewed hostilities, near-term UK electricity prices have crept up above the psychological level of £100/mwh amid fears that replenishing storage in time for the onset of winter becomes trickier the longer the Strait remains closed for business.

This despite today’s UK electricity generation mix being very bearish in nature – specifically, renewables are contributing 62%, thermal at 4% (gas and coal) and low carbon at 18% (nuclear and imports).

So, under normal summery conditions, today would be seeing very low prices – unfortunately, the primary key price driver since 28th Feb is linked to the vagaries of US foreign policy.

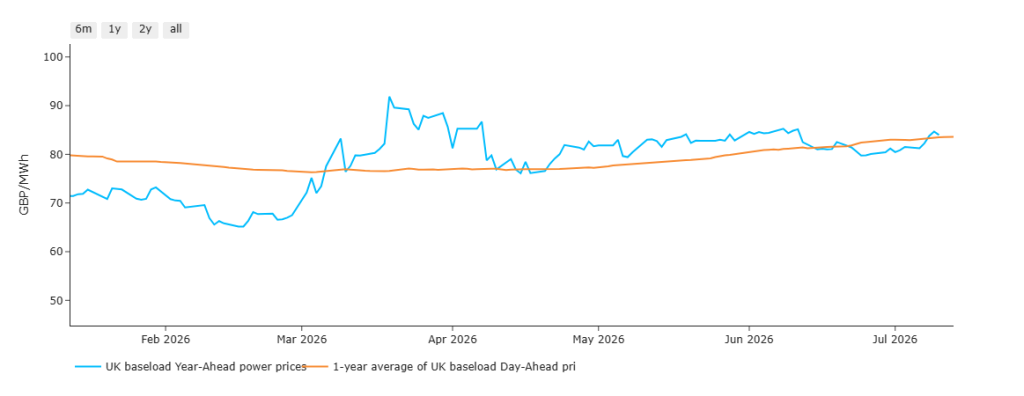

The chart below details UK electricity Year-Ahead prices versus the 1-Year Average of Day-Ahead prices since late-Feb.

By way of explanation, when the blue line is above the orange line, mid-term delivery prices are at a premium to an average of the last 12 months.

As you can see, prior to the onset of the US/Israeli offensive, prices were enjoying a soft-landing heading into Summer-26 – thereafter, Year-Ahead has remained consistently at a premium despite the otherwise ‘summery’ conditions.

Despite last week seeing an improved outlook for the Gulf crisis, and several days of the blue line being back below the orange line (reflecting a significant shift in sentiment), I’m afraid that ,as of this morning, near-term delivery is back above averages and so solid comparative value is once again off the table.

On the Carbon side of things, mid-price Dec-26 UKA delivery remains directionless at £56.65/tn (and the spot is at early 55s) – reflecting an underlying sentiment that industrial demand destruction is inevitable (should the Gulf crisis persist into the winter months).

On the FLEX side of things, for clients with remaining near-term open volumes, we’ll look to advise on potential intraday dips and hedging opportunities over the coming days (though we don’t expect many, if any).

UK electricity Monthly Day-Ahead Averages for July so far are holding steady at £92/mwh (or 9.2 p/kwh exc. non-energy) – so the monthly Day-Ahead average for July so far remains below near-term monthly Forwards (for August and September).