Analysts/traders are quiet today, but seemingly optimistic – with prices having fallen gradually since this morning’s opening bell.

Yesterday’s confirmations that Israel was preparing to enter into direct talks with Lebanon were enough to encourage bullish speculators to close out long positions – as such, prices have lost value all the way down the curve.

And yet, news still pervades the airwaves that Israel continues to drop bombs on Lebanon – despite confirmed reports that hundreds of civilians (including 120 children) across Beirut have been killed this week.

Against this backdrop, JD Vance is heading to Islamabad, talking up the prospects of “positive talks”.

And so, prices are falling in anticipation that Israel will stop, and the Strait of Hormuz will re-open.

Unfortunately, such an outcome is far from certain amid worries that the Trump Administration is struggling to put the genie back in the bottle.

FLEX clients are heavily hedged the front month (May-26), so as not to be caught out in the event the Islamabad talks go sour (and Trump resumes his “mad-man” approach).

When all is said and done, so long as the Strait of Hormuz re-opens (without tolls), markets will drop fast and steep.

But this will only happen if Israel can be reined in by the Trump Administration.

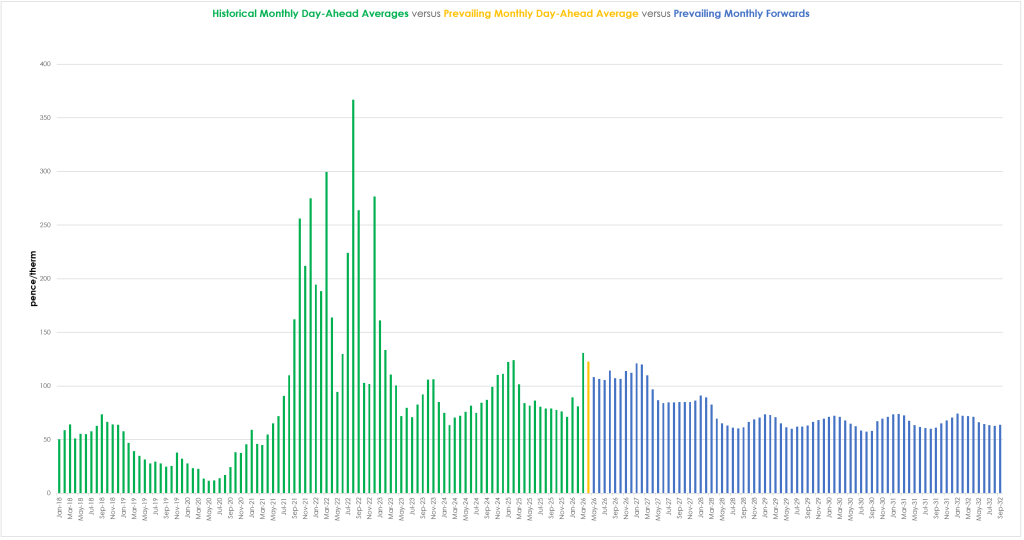

The context chart below shows Historical Monthly Day-Ahead Averages (green columns), prevailing Monthly Day-Ahead Average (single orange column), and prevailing Monthly Forward prices.

Monthly Day-Ahead Averages for the month so far are holding steady at 123p/therm (or 4.2p/kwh exc. non-gas).

ELECTRICITY & CARBON

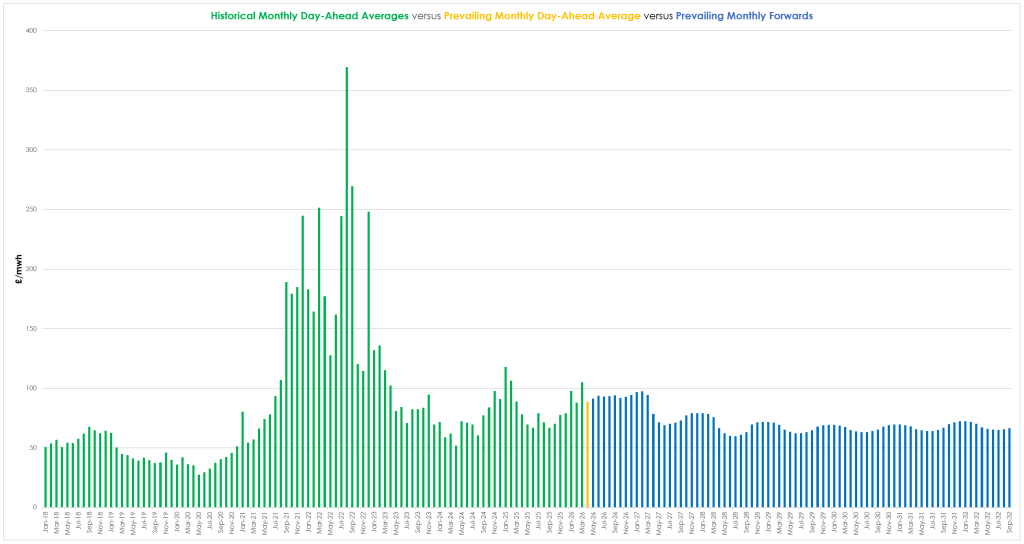

The context chart below shows Historical Monthly Day-Ahead Averages (green columns), prevailing Monthly Day-Ahead Average (single orange column), and prevailing Monthly Forward prices.

UK electricity prices remain at a significant discount versus gas prices (given summer conditions/improved renewables outputs/falling gas-for-power burn).

FLEX clients are heavily hedged the front month (May-26), so as not to be caught out in the event the Islamabad talks go sour (and Trump resumes his “mad-man” approach).

On the Carbon side of things, Dec-26 UKA delivery remains uncoupled from gas volatility with prices touching levels that are 31% below those printed in mid-Jan amid fears that Trump’s war on Iran is slowing global economies (and, in so doing, Industrial outputs).

At the time of writing, UKA mid-price Dec ’26 delivery is at £43.37/tn (and the spot is at early-42s).

Since the US/Israeli offensive began, gas price falls are met with rising UKAs (and vice versa) – so UKAs have been on the up today.

Monthly Day-Ahead Averages for UK electricity for the month so far remain at £89/mwh (or 8.9p/kwh exc. non-energy).