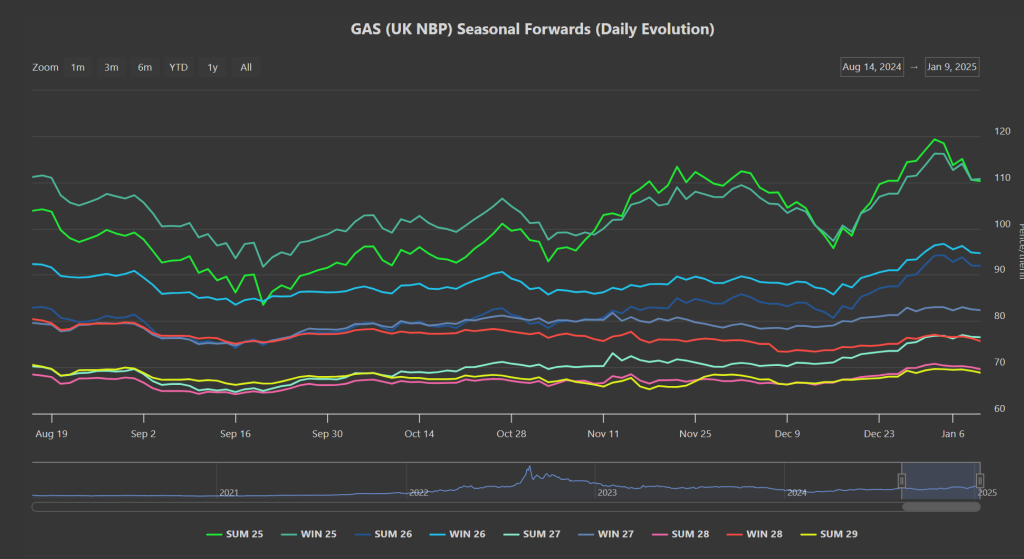

The Summer-25 risk premium over Winter-25 has corrected itself again – reflecting more optimism that replenishing storage over the summer months shouldn’t be as difficult as the doomsayers (bullish traders) would have us believe – please see chart below showing Summer-25 delivery prices now at a discount versus Winter-25.

The week has finished on an encouragingly bearish note off the back of comfortable supply and temperatures in the UK forecast to be back above seasonal norms by 14th Jan.

Norwegian flows are in good shape (though Hammerfest and Kollsnes have some capacity offline due to end tomorrow) – whilst LNG send out has risen this week to meet increased heating demand caused by the cold spell.

Increased storage withdrawals have also been required (given that wind outputs are on the floor) with European inventories at 68% versus the 5-year average of 76% (though fullness levels are bang in the middle of the 8-year range).

Despite sub-zero weather warnings across Europe today, prices down the curve have fallen given forecasts of temperatures rising again next week.

LNG demand across Asia remains depressed, so cargoes are following the money to Europe – keeping downward pressure on European/UK prices.

Notably, Russian LNG exports into the rest of Europe were up in 2024 versus 2023 – so the loss of the Ukraine/russian transit deal has evidently (to some extent) been mitigated.

Day-Ahead is more expensive than Month/Quarter-Ahead at the moment, reflecting a belief that prices are set to fall over the coming weeks/months.

Monthly Day-Ahead averages for this month so far remain inflated but are falling – 120.065p/therm (or approx. 4.097p/kwh excluding non-gas).

ELECTRICITY & CARBON

Not surprisingly, electricity down the curve is mirroring falling gas prices.

Though inflated front-end delivery prices still reflect wintry conditions coupled with poor wind ouputs.

On the Carbon markets, UKAs are again at a significant discount versus EUAs – reflecting less scarcity of credits (with free allowances not scheduled to fall in the UK until 2027).

However, the bearish rally beginning 6th Jan has been halted by compliance buyers picking up heavy volumes at good prices, with a symmetrical triangle pattern forming – reflecting sideways sentiment.

Though momentum indicators started this morning’s session looking bullish, and sure enough the triangle has broken to the upside with a technical target of £35.90/tn on the mid-price looking likely – please see chart below.

Today’s UK’s electricity generation mix is bullish (and price supportive) in nature with renewables contributing 16%, thermal at 52% (gas and coal) and low carbon at 19% (nuclear and imports)

Monthly Day-Ahead averages for this month so far reflect poor renewables outputs, £114.099/mwh (or 11.41p/kwh excluding non-energy).