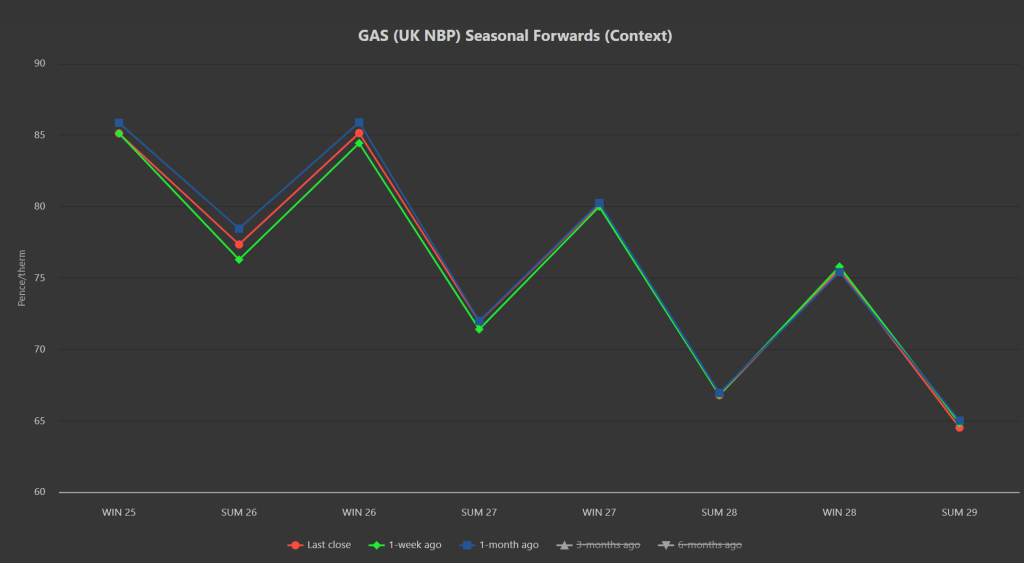

The chart below details Seasonal Forward prices at last close; one week ago; one month ago.

As you can see, values are barely altered – reflecting very low volatility this last few weeks for Forward periods of delivery.

Given mild temperatures, the heating season still looks a little way off – ordinarily 1st Nov marks the period when we expect storage injections to end (and withdrawals to begin in earnest).

As such, prices have resumed rangebound action with Month-Ahead prices having only bracketed in a 12% range since 1st Sep.

Steady supply continues to mitigate the hazards of impending cold weather – fortunately, Europe remains a popular destination for LNG (given greater profitability for cargoes headed to Europe over Asia).

In other news, Egypt looks likely to defer some LNG deliveries from Q4 2025 into next year – with talk of a glut of LNG come ’27, is this a sign of things to come (i.e., supply outstripping demand)?

Monthly Day-Ahead averages for October so far are at 78p/therm (or 2.66p/kwh exc. non-gas).

In short, whilst Winter-25 has officially begun, we’re yet to feel the effects of increased demand/increased withdrawals/worries over supply tightness.

And so, whilst momentum remains neutral to bearish, traders are all too aware of the fragility of the European gas balance.

ELECTRICITY & CARBON

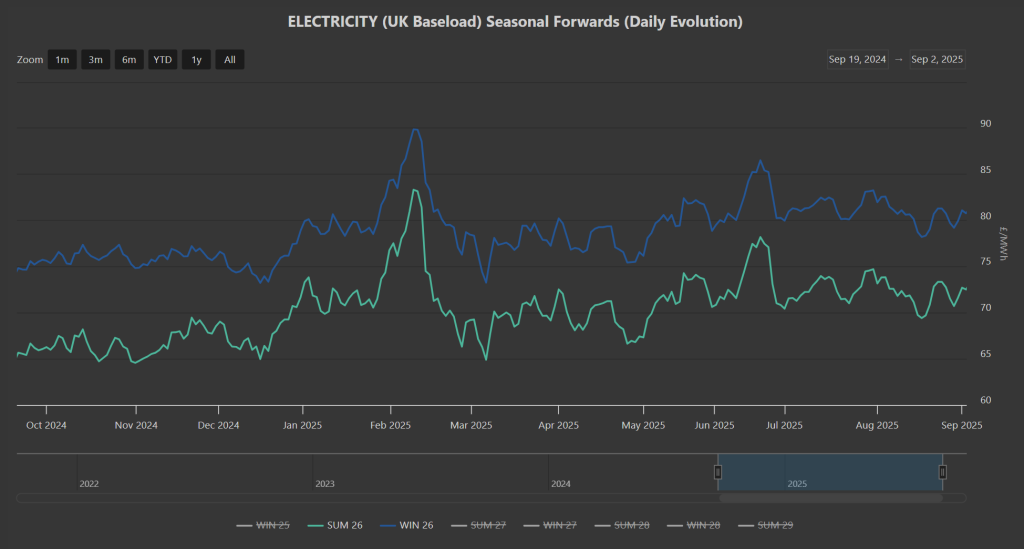

The chart below details Summer-26/Winter-26 delivery prices dating back to the onset of last winter.

If recent history is anything to go by then, we should expect prices for the front 2-Seasons to increase over the coming months, peak in Feb ’26, then drop off as temperatures rise into Mar ’26.

Certainly, I think it’s fair to say that current prices do not feel inflated – and so a drop-off over the winter months would seem very unlikely.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are holding steady in the mid-50s (currently at £55/tn).

Today’s UK electricity generation mix is bullish in nature – specifically, renewables are contributing 28%, thermal at 42% (gas and coal) and low carbon at 19% (nuclear and imports).

Monthly Day-Ahead averages for October so far are at £66/mwh (or 6.6p/kwh exc. non-energy).