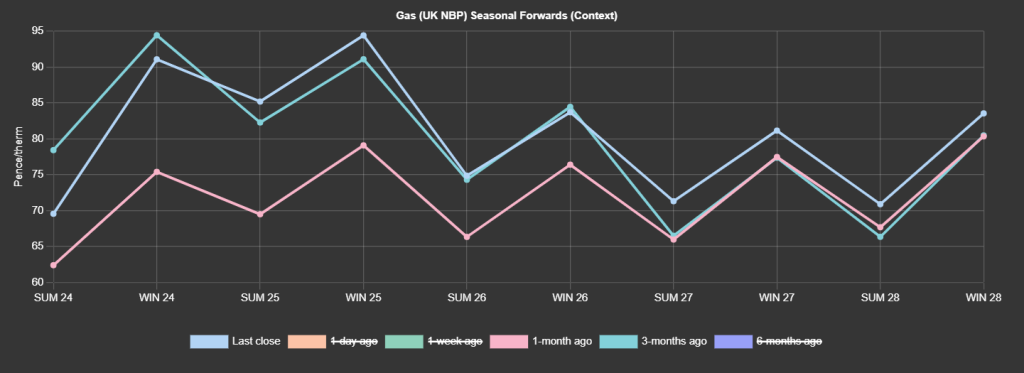

Geopolitical fears resurfaced yesterday – whilst the front end of the Seasonal Forward curve remains below prices printed 3-months ago, the mid-term prices have drifted above (see chart).

Out of the blue, UK gas prices reacted to multiple supply risks.

Freeport LNG terminal (Train 3) went offline and gave rise to panic over the possibility of lower LNG flows to Europe in the coming weeks.

In addition, reports emerged from Ukraine of damage inflicted on gas storage sites and power stations by Russian forces.

Ukraine’s state run Naftogaz has confirmed that Russian strikes attacked two underground gas storage facilities overnight; the company added that the storage facilities continued to operate.

The Russian attacks also hit power facilities (as a reminder, on 24 March, a Russian attack had already hit the ground infrastructure of one the Ukrainian gas storage facilities, resulting in damaged technological equipment without affecting the supply of gas as there were no critical consequences).

Market participants cite fears that the multiplication of these attacks could end up impacting Russian flows that are still delivered to EU countries via Ukrainian transit routes (around 1.15 bcm/month).

These most recent attacks highlight the fallibility of using Ukrainian gas storage for extra reserves and how sensitive prices are to fears of supply disruption – notwithstanding Europe’s historically high gas reserves.

Prices have risen again this morning with news of lower feedgas (dry natural gas that is used as raw material for LNG)being delivered into Freeport which has done nothing to alleviate market jitters of potentially lower LNG volumes.

For near-term delivery, the ongoing warm temperatures and strong wind generation have kept a lid on bullish momentum.

Day-Ahead and weekend delivery contracts remain soft off the back of a bearish setup of strong renewables forecasted to suppress demand.

This week’s events aside, consensus remains that we’ll see improved value for Winter-24 delivery as the summer progresses (assuming geopolitical impacts don’t get worse).

Monthly Day-Ahead averages are on target this month to achieve 65p/therm (or 2.25p/kwh).

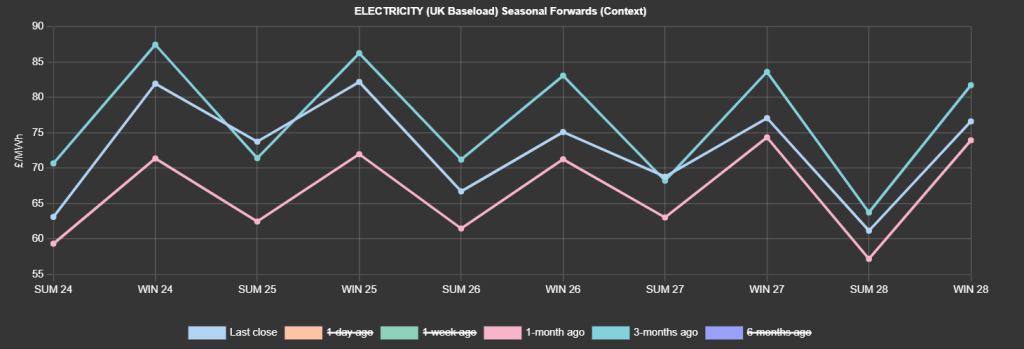

ELECTRICITY & CARBON

Looking to the continent for further reaction, near-term delivery prices continued to be pressured yesterday by very mild temperatures (ranging 3-6°C above seasonal norms) and strong renewable production.

Of course the market was supported in the morning by soaring gas prices following the Russian attack on Ukrainian underground gas storage and the European Parliament decision to temporarily halt Russian gas imports.

Following a brief respite midday, the upward trajectory of gas prices triggered a short squeeze in the carbon markets, leading to another wave of bullish activity across the energy complex.

Very strong gains were posted along the curve, and the energy markets have continued their their upwards trend this morning.

Dec-24 contracts for UKAs are circa. £37/tn.

Our electricity generation mix is very bearish in nature today with renewables contributing 63%, thermal at 3% (gas and coal) and low carbon at 21% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £48/mwh (or 4.8p/kwh).