The headlines are dominated by the Allies’ srikes against the Houthi rebels in Yemen – as well as the subsequent condemnation by Russia, China and Turkey.

Insecurity for LNG vessels navigating in and around the Suez Canal continues to provide support to near-term delivery prices.

On the supply side, Norway have had a minor outage at Aasta Hansteen – though the loss of 8 mcm should only last for a day or so.

At the time of writing, prices are marginally up versus this morning’s open – this despite a slightly long system (supply outstripping demand).

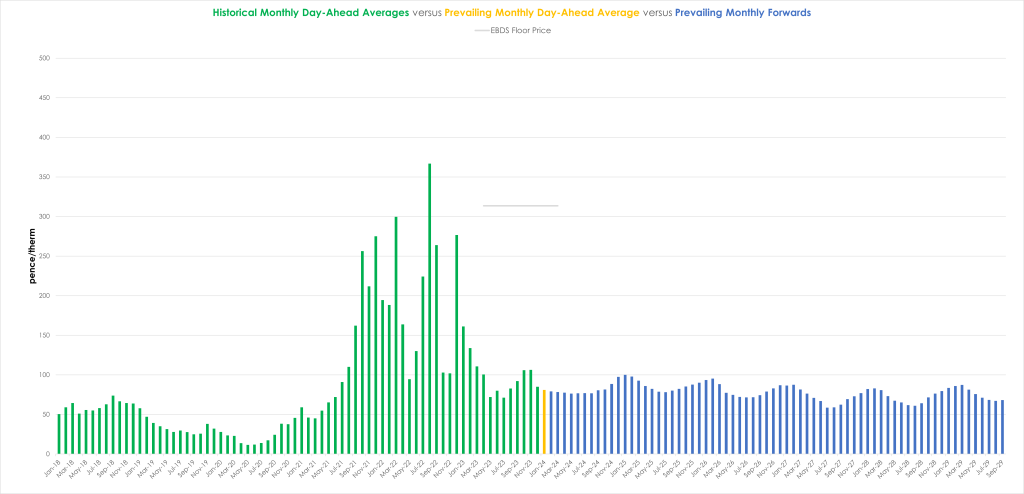

Looking at the bigger picture, monthly Forwards all the way down the curve are now at or below the psychological level of 100p/therm.

Monthly Day-Ahead averages are on target this month to achieve 81p/therm (or 2.76p/kwh).

ELECTRICITY & CARBON ALLOWANCES

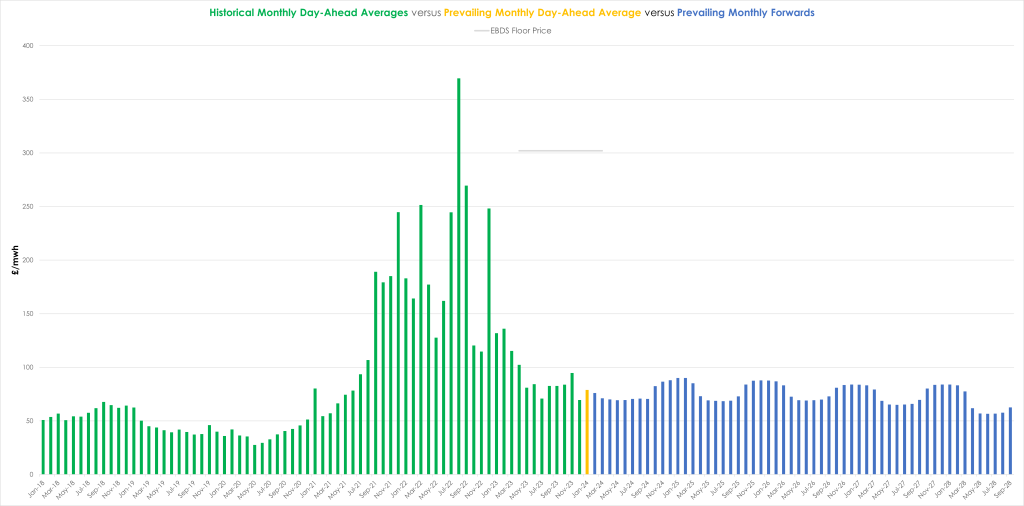

Looking at the bigger picture, monthly Forwards all the way down the curve are now at or below the psychological level of £100/mwh.

Looking to the continent for direction, European short-term delivery prices faded further yesterday against a backdrop of unseasonably benign fundamentals and sliding carbon and gas prices.

Expect more of the same next week, with improving wind outputs and higher French nuclear availability by mid-week.

Once again, market participants were quick to react to a marginally milder revision of weather forecasts for the back end of Jan ’24.

Though a slightly colder correction overnight supported prices at this morning’s open for near-term delivery.

Any meaningful upside potential remains limited by sustained high gas, nuclear and hydro stocks and availability.

Notwithstanding coal prices experiencing a more substantial decline than gas prices yesterday, carbon prices still continued their downward trend.

The market sentiment remains bearish off the back of an anticipated increase in supply of credits, as well as expectations of lower emissions this coming year compared to 2023 (due to demand destruction).

The resumption of auctions scheduled for next week is further depressing the market, as supply is abundant, and demand is on the slide.

Back in the UK, our generation mix is bullish (though you wouldn’t know it from price action) – 60% gas-for-power burn; 15% renewables; 11% low carbon (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £79/mwh (or 7.9 p/kwh).