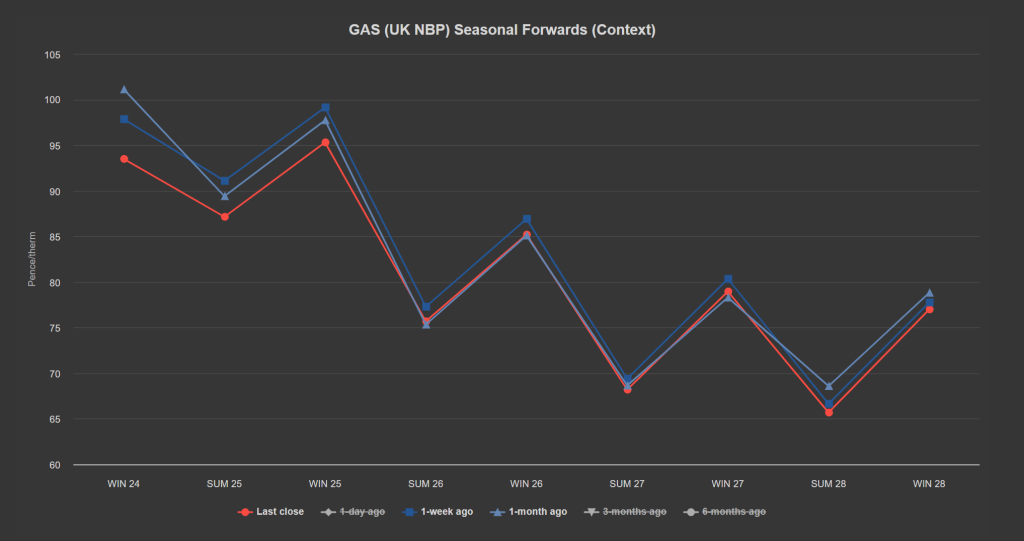

Prices are ending the week down on both the week and the month – see chart.

Though, yesterday, prices tracked European benchmarks and printed a marginal increase to halt a 4-day bearish run.

Bullish support is centred around fears of LNG supply tightness, with Freeport LNG terminal still not operational following a hurricane induced outage.

At the time of writing, both near- and far-term prices are trading sideways with a marginal bearish bias.

The UK system opened long this morning (supply outstripping demand forecast).

Fundamentals remain unchanged, meaning a combination of storage injections and strong exports to the continent look set to continue to sustain a comfortable market balance.

Wind outputs are forecast to drop off this weekend (increasing the need for gas-for-power burn) which is limiting any further meaningful downside price action in the short term.

All in all, solid injections and high European storage (80% versus the 5-year average of 67%) coupled with steady Norwegian flows continues to apply bearish pressure to a market exhibiting mild summery symptoms.

With demand low, and supply comfortable, replenishing gas stocks is not posing any problems.

On the hedging side, we’re now on the other side of Summer-24 – with 103 days having elapsed, and 81 remaining.

Clients with open volumes for Winter-24 are increasingly scaling-in so as to avoid any loss of prevailing value.

Prices are increasingly soft and threatening to roll-over, with temperatures expected to be back above seasonal norms come 16th July (amid improving wind outputs as the month progresses).

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24) – though LNG delivery remains tight against a backdrop of sustained high temperatures across Asia (and the associated cooling demand).

Monthly Day-Ahead averages so far this month are on target to achieve 76p/therm (or circa. 2.55p/kwh excluding non-gas).

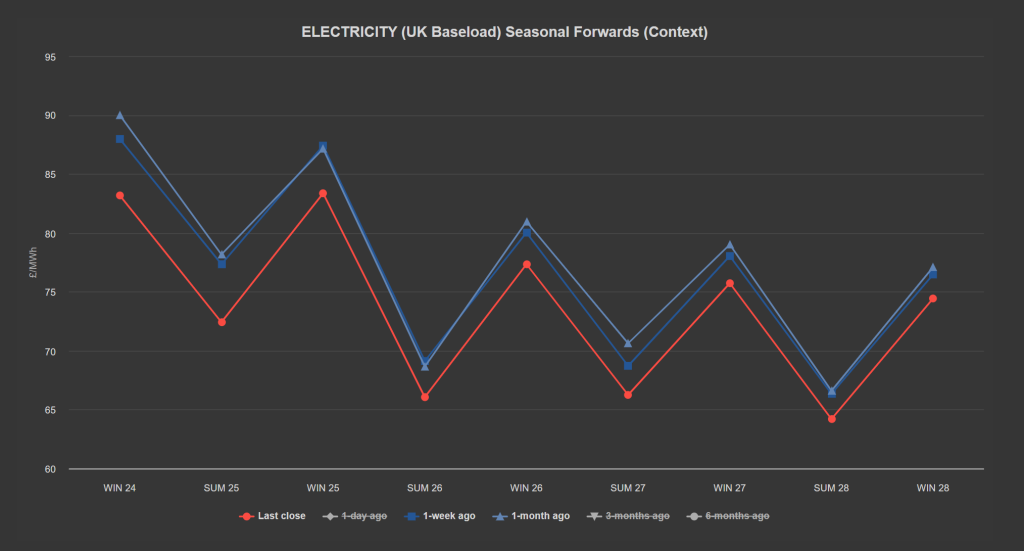

ELECTRICITY & CARBON

Looking to the continent, near-term delivery prices are circa. 10% lower on the day.

Things look warm come the weekend across Western Europe – wind will be patchy and driven by frontal weather conditions.

On the Carbon side, markets remain in a bear trend (tracking gas) – though summer remains unsupportive for emissions prices.

Back in the UK, UKAs (UK Carbon Allowances) followed our prediction that prices were due to fall (as indicated by RSI divergence) – now trading at circa. £41/tonne.

Prices are now in a confirmed ascending trend channel testing the lower extremity – with £40/tn as a strong area of support to the downside – so a retest of this level is likely if EUAs can maintain bearish momentum.

Our electricity generation mix is bearish in nature today with renewables contributing 36%, thermal at 22% (gas and coal) and low carbon at 29% (nuclear and imports).

Monthly Day-Ahead averages so far this month are looking summer-esque, and are on target to achieve £62/mwh (or circa. 6.2p/kwh excluding non-energy).