The UK/Europe’s LNG imports remain on an upward trajectory (see chart below) with higher prices attracting LNG cargoes, coupled with Asia opting increasingly for alternate/less costly fuels (coal/oil).

China in its capacity as the largest global LNG importer has not only reduced its LNG buying, but has in fact opted to resell back to market at a profit given price increases (and lowering demand).

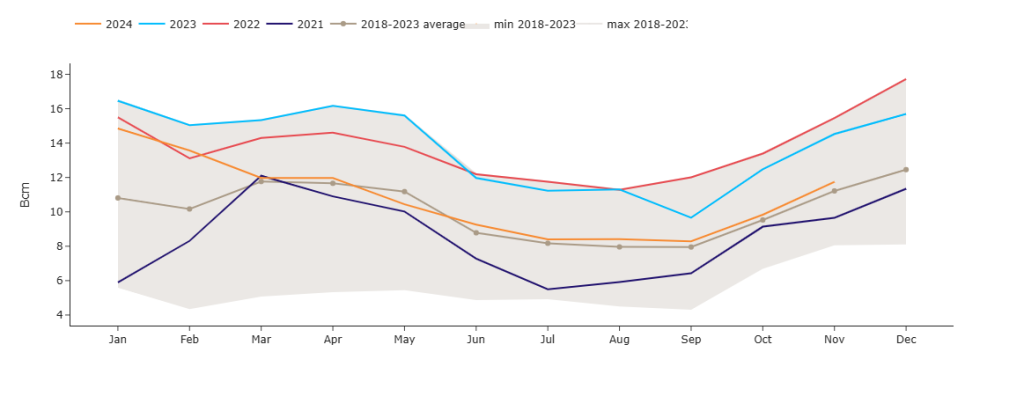

Statistically-speaking, Chinese LNG imports are now more than 10% below the 4-year average – an indication that China is NOT prepared to compete for LNG at any price.

UK gas prices (NBP) are down on the week and at parity with one month ago despite our being at the height of the Winter-24 season.

Current unplanned outages in Norway are expected to end at the beginning of next week, lending additional supply availablity.

Encouragingly (and as predicted last week), Summer-25 risk premium versus Winter-25 has diminished with both seasons offered now at near-parity – reflecting a calmer, more postive attitude towards replenishing gas storage during Summer-25 in time for Nov-25 (when withdrawals ordinarily begin in earnest).

Markets have opened soft this morning against a backdrop of increasingly benign weather forecasts – though these have been flip-flopping from day-to-day.

Geopolitically, the Middle East is grabbing fewer headlines despite Syria’s power vacuum likely to result in a more widespread conflict/land-grab on the part of Israel with the US hinting at abandoning support for the Syrian Kurds once Trump assumes control in Jan-25.

On the bullish side, rumours abound of discussions on potential US and Israeli strikes on Iranian nuclear facilities which may inject some volatility over the coming days.

European gas storage is at 80% versus the 5-year average of 84% – with withdrawals happening at a faster pace than last year.

The Ukraine/Russia transit deal is only a couple of weeks away from ending, yet seemingly negotiations have stopped – so this uncertainty remains a price supportive driver.

So far this month, Monthly Day-Ahead averages are falling and on target to achieve 113.905p/therm (or approx. 3.887p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, markets dropped off nicely yesterday.

On the Carbon markets (EUAs/UKAs) – the DEC ’24 EUA (with trading ending 16th Dec-24 for Christmas) fell by 3.69%, closing at €66.10/tn.

UKAs (UK Allowances) are are at £34.16/tn on the mid this morning, and very much back on the slide on low volumes (see chart below) – having broken below the lows of 7th Oct-24, with a retest of the all-time lows of £31.30/tn printed on 29th Jan-24 now in the offing.

The week of poor renewables output across the UK/Europe looks set to improve with both wind and average temperatures expected to pick up this weekend.

The UK’s electricity generation mix is bullish in nature today with renewables contributing 8%, thermal at 64% (gas and coal) and low carbon at 16% (nuclear and imports).

Monthly Day-Ahead averages for the month so far have risen given a couple of heavy days and are on target to achieve £112.889/mwh (or 11.29p/kwh excluding non-energy).