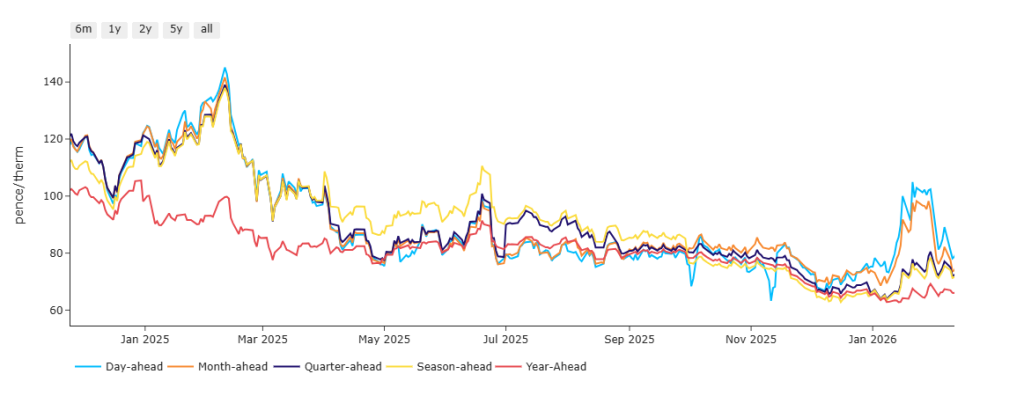

Near-term delivery remains toward the bottom of a 12-month range (please see chart below).

In fact, European/UK prices are on-target for their steepest weekly fall since Jun-25 thanks to solid supply offsetting wintry conditions.

This week has seen bullish days, then bearish corrections, and now sideways price action – reflecting the balancing effect of neutral underlying fundamentals.

Bears will have been pleased to hear this week that Norway looks set to un-mothball several North Sea fields so as to increase production beginning 2028 (they were closed down in 1998 due to pressure depletion across the chalk reservoirs).

Bulls are keen to reiterate that European storage fullness is now looking very depleted – 35% versus the 5-year average of 61%.

Refilling will not begin until Apr-26, so it looks likely we’ll end Winter-25 at levels potentially below the 7-year range (near 20%) – thereafter, those market particpants with a vested interest in seeing prices rise will no doubt spread fear that Summer-26 will need to see higher prices so as to ensure we can refill in time for Winter-26! And so it goes on…

The truth will be somewhere in the middle – yes, summer refilling will require very solid supply dynamics, but we have those – and given Trump’s latest gambit at reversing emissions restrictions, it would seem very unlikely that the US is going to curtail its LNG exports to European shores any time soon.

On the strategy side, FLEX clients are still taking small positions further down the curve where there’s great value to be picked up.

Monthly Day-Ahead averages for the month have fallen slightly to 86p/therm (or 2.9p/kwh).

ELECTRICITY & CARBON

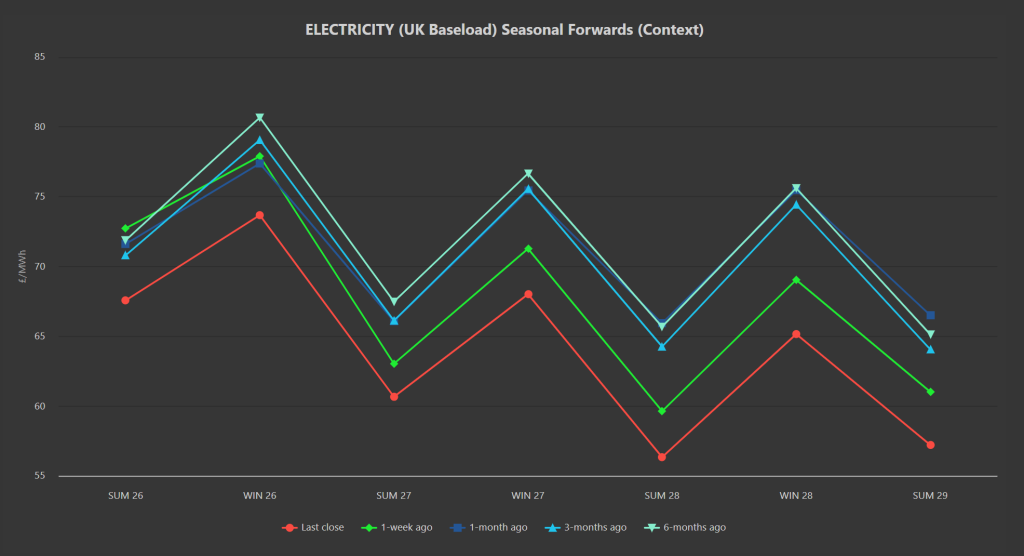

Seasonal Forwards all the way down the curve are lower on the week/month/3-months/6-months (see chart below).

On the Carbon side of things, both EUAs and UKAs have been in free fall amid revelations that make Starmer’s premiership look increasingly shaky.

Front December delivery over the last 12-months has seen a march northwards beginning Jan-25 when Starmer first announced his plans to re-link EUETS and UKETS.

Since his potentially imminent demise has come to the fore in the last week or so, UKAs have become disproportionately bearish with re-linkage looking less likely.

At the time of writing, Dec-26 UKA delivery has fallen to £45.42/tn (down 40% in a just a fortnight!)

Compliance buyers can only look on and scratch their heads as to how they can budget accurately for a tax which rises and falls with such erratic volatility.

Today’s UK electricity generation mix is bullish in nature – specifically, renewables are contributing 29%, thermal at 46% (gas and coal) and low carbon at 16% (nuclear and imports).

Monthly Day-Ahead averages for the month so far remain wintry at £95/mwh (or 9.5p/kwh exc. non-energy).