Following a quiet week, prices are sharply up this morning following Israel’s attack on Iran (only hours after U.S. and Israeli officials had warned one was imminent).

From a gas POV, market participants are most concerned about LNG shipments through the Strait of Hormuz – though right now, LNG is traversing the waterway as normal.

Though it’s likely we’ll start seeing delays if the skirmish escalates – and no doubt, prices will rise to reflect supply tightness.

20% of world LNG supply transits the Strait of Hormuz (mainly from Qatar and the UAE).

Norwegian flows are still patchy off the back of maintenance, and storage injections are slowing.

So, this latest geopolitical impact is likely to tip the balance in favour of the bulls over the coming days – a blow to summer buyers.

Notably, Winter-25 gas has spiked 7p/therm versus yesterday’s closing (currently sitting at 101.5p/therm).

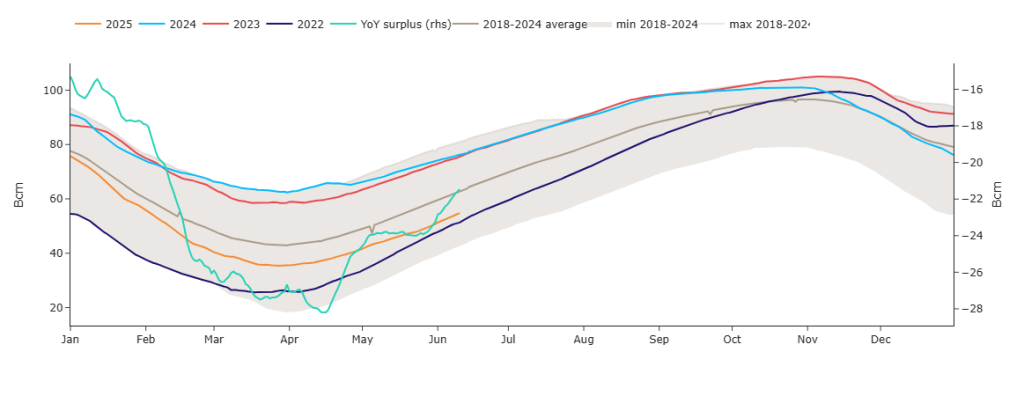

European storage fullness sits at 52% versus the 5-year average of 65% – so we’ve lost a little injection ground this week (please see chart below).

On the trading side, clients running flexible capability would be wise to sit on the sidelines as the Israel-Iran flare-up unwinds.

This month’s UK gas Day-Ahead averages are at 84p/therm (or approx. 2.9p/kwh excluding non-gas) – though this number will likely creep up over the coming days subject to Iran’s retaliation.

ELECTRICITY & CARBON

Not surprisingly, near-term electricity prices have mirrored the gas spike.

Notably, Winter-25 has jumped from yesterday’s closing price at £88/mwh (or 8.8p/kwh) to £92/mwh (or 9.2p/kwh) at the time of writing.

On the Carbon side of things, UKAs have resumed their upwards drift toward EUA parity (off the back of solid bullish volume) – currently sitting at £55.30, retesting resistance at £55.40 (please see chart below).

Today’s UK electricity generation mix is bearish in nature reflecting benign weather conditions – specifically, renewables are contributing 44%, thermal at 17% (gas and coal) and low carbon at 21% (nuclear and imports).

So far this month, electricity Day-Ahead averages remain low and reflect summer-demand – currently at £64/mwh (or approx. 6.4p/kwh excluding non-energy).

On the trading side, clients running flexible capability would be wise to sit on the sidelines as the Israel-Iran flare-up unwinds.