Whilst European/UK gas prices have surged since 28th Feb (taking electricity with them), actual open interest in gas futures has fallen to a half-year low – reflecting just how many participants are watching from the sidelines (given that Trump is in a rush, and not prone to sustaining commitment to any one course of action for a protracted period of time).

Israel’s Netanyahu has also been outlining the nature of Israel’s successes in the war to date, which many are taking as a pre-cursor to potentially winding things up.

India’s Ministry of External Affairs is already talking directly with Iran with a view to agreeing safe transit for vessels through the Strait of Hormuz – so, it’s fair to argue, that the wheels of diplomacy may have already started turning.

For the time being, approximately 20 LNG tankers are languishing in the Persian Gulf – in his first major public announcement, the new Iranian Supreme Leader has vowed to keep the Strait closed for business (with a view to heaping domestic pressure on Trump with US ‘gas’ (petrol) prices continuing to rise).

For their part, the US conceded yesterday that the US Navy couldn’t realistically escort ships through the Strait for now, but it was “quite likely” that it will happen by the end of the month – for many traders, the end of the month is just too far away…

In a further bid to stabilize markets (and by way of a firm slap in the face of the EU), the US has issued a 30-day license for countries to buy Russian oil/petroleum products stranded at sea!

The market’s reaction to this measure suggests that participants see this as a very short-term solution, and more political than designed to alleviate supply shortages.

Notably, Gazprom said yesterday that two its compressor stations were again attacked by Ukraine, but that all attacks had been repelled – it would seem risk abounds in all directions, and so markets remain high for now (but less volatile than a week ago).

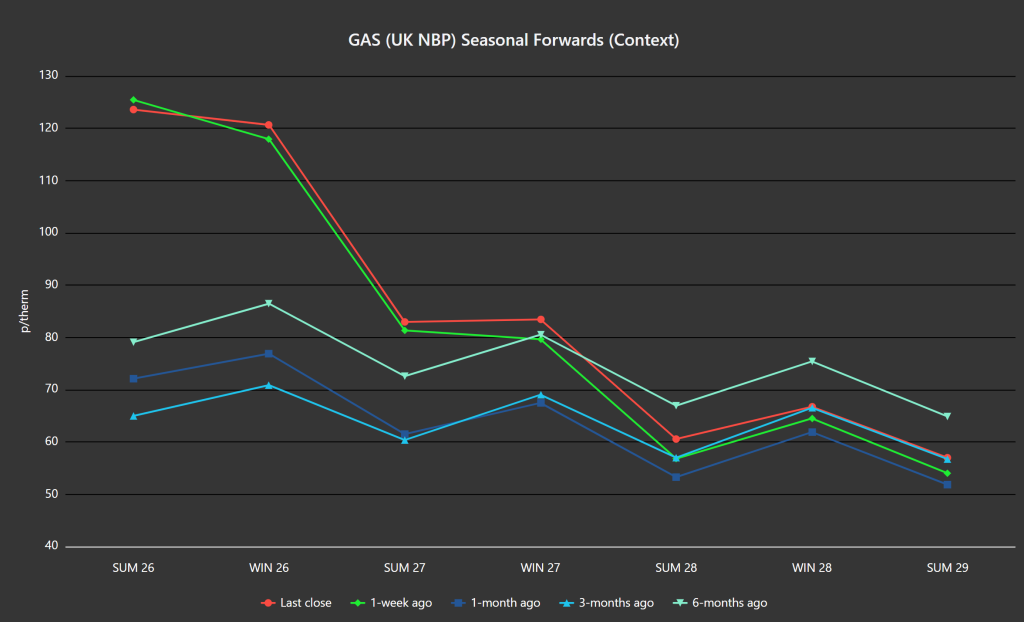

Seasonal Forwards remain steeply backwardated with some great offers remaining further down the curve.

As such, on the strategy side, FLEX clients are being encouraged to build modest positions further down the curve beginning Summer-28 (where pre-Iran war prices persist, reflecting an underlying sentiment that this conflict will be short-lived).

Monthly Day-Ahead averages for the month remain high – currently at 123p/therm (or 4.2p/kwh).

ELECTRICITY & CARBON

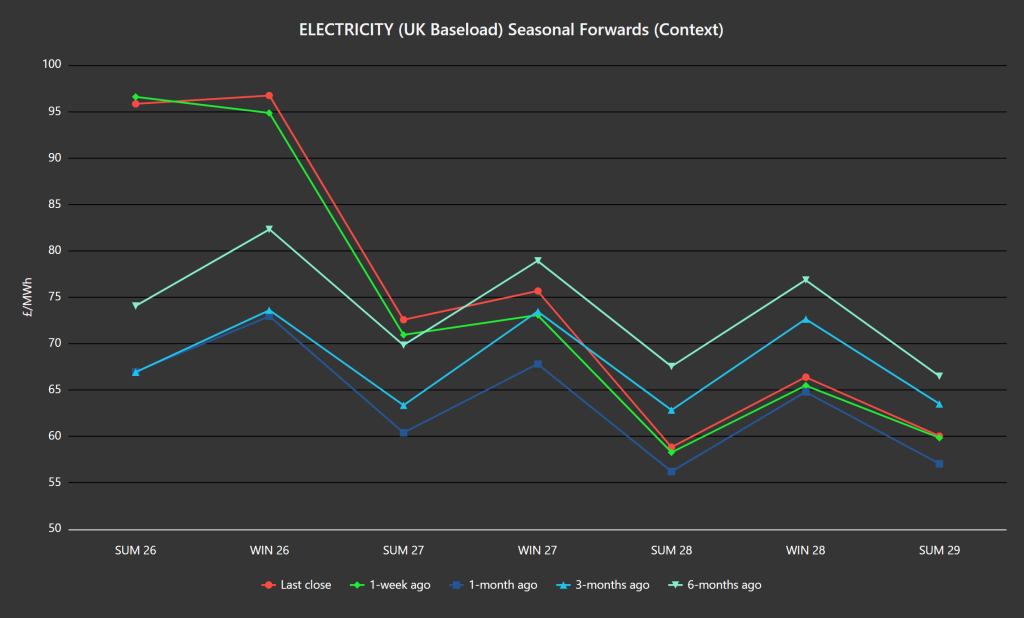

As per the chart below, electricity prices remain (as ever) closely correlated to gas movements.

Conversely, on the Carbon side of things, Dec-26 UKA delivery remains uncoupled from gas volatility with prices still at levels 40% below those printed in mid-Jan amid fears that Trump’s war on Iran is slowing global economies (and, in so doing, Industrial outputs).

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 52%, thermal at 22% (gas and coal) and low carbon at 19% (nuclear and imports).

On the strategy side of things, electricity FLEX clients are being encouraged to build modest positions further down the curve where steady prices persist (given that far term delivery prices are as much as 35% below those of near-term delivery).