It’s been another week of sideways price action – with Seasonal Forwards barely altered versus 1-week ago.

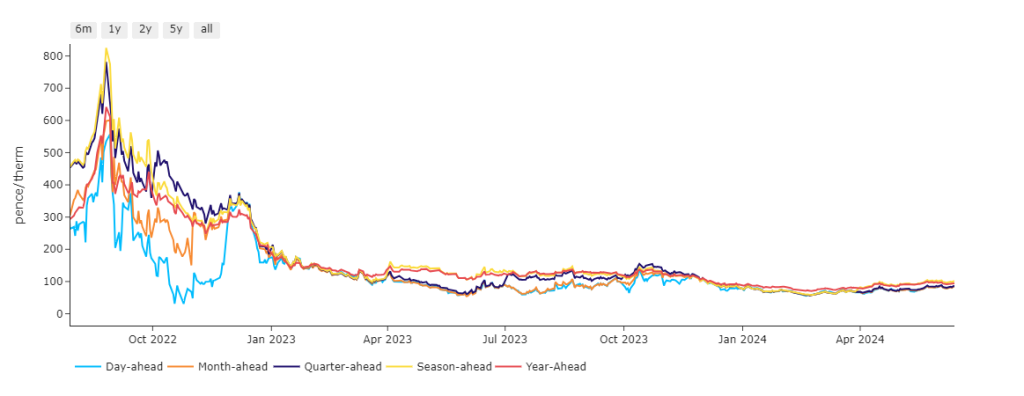

Looking at the bigger picture, market volatility for near-term delivery remains relatively flat versus the chaos of ’21/’22/’23 – see chart.

Any bullish momentum has been driven by fears of supply tightness further to the unscheduled, ongoing maintenance at Wheatstone LNG terminal in Australia – it’ll be weeks before the site comes back online.

This perceived tightness is coupled with high temperatures across Asia (and the associated high cooling demand) – prices are higher in Asia, so that’s where cargos are headed.

Whilst Europe has gone a long way toward diversifying gas supply since Russia invaded Ukraine, risks persist.

As we’ve seen recently with Freeport in Texas, and now with Australian LNG fields, Europe is being forced to compete with Asia (China) – this competition will always be price supportive.

Though as outlined in recent reports, if gas prices go too high, Asia will likely turn to coal – so the price support has its limits.

The UK system was long this morning (supply outstripping demand forecast), notwithstanding temperatures below seasonal norms (sustaining LDZ, or heating demand).

Prices have softened to end the week despite confirmation that maintenance at both the Barrow North terminal (UK) and the the Visund gas plant (Norway) is to be extended.

As we head deeper into summer conditioning, demand is on a downwards trend and will gradually loosen the UK balance – allowing storage injections.

Whilst it’s conceivable we’ve already seen the bottom of summer pricing, it’s not panic stations just yet.

The consensus amongst Industrials continues to be one of scaling-in whilst adopting a wait-and-see approach to any remaining open volumes for Winter-24/winter-25.

109 days of Summer-24 remain (with 75 days now used up) – so a significant chunk of Summer-24 is still ahead of us.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24).

Monthly Day-Ahead averages are on target this month to achieve 83p/therm (or approx. 2.8p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent, European near-term delivery prices dropped off yesterday, pressured by prospects of weaker demand and stronger wind outputs.

Prices are expected to fall further this weekend off the back of sustained renewables generation.

On the European Carbon markets (EUAs) , it’s been the same pattern all week – up in the morning to mirror gas prices, then losing steam toward the end of the session.

Back in the UK, UKAs (UK Allowances) are treading water – now trading at approx. £48/tn (Dec-24 benchmark) – having failed to break above the upper extremity of the confirmed price channel, with momentum indicators in overbought territory and rolling over.

Our electricity generation mix is bearish in nature today with renewables contributing 39%, thermal at 19% (gas and coal) and low carbon at 27% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £67/mwh (or 6.7p/kwh excluding non-energy).