Whilst the bigger picture remains overwhelmingly bearish, the last couple of days have seen prices well-supported – though gains have been very modest.

Strong moves in the wider energy complex (fuels and emissions) have added some marginal value to near-term delivery gas contracts.

Despite the UK system being long at market open (supply outstripping demand), prices rallied this morning – but have dropped back again to end the week.

Most likely, prices have found their bottom for now and so market participants are bound to test support/resistance levels until such a time as the bulls or the bears take hold.

In real terms, markets are balanced and enjoying comparative equilibrium versus the volatility that began in mid ’21 and only really abated at the back end of ’23.

Down the curve, prices are a little firmer too – supported in the main by concerns over supply tightness as flows have dropped off to the Corpus Christi LNG facility (Texas, USA).

Europe is heavily reliant on imports from the US, most of which come from Texas.

Also, one of the trains at Freeport LNG (also Texas) remains offline – further limiting export capability.

Temperatures are set to remain warm over the weekend and will stay above seasonal norms into next week – limiting heating demand.

Norwegian flows remain steady and (due to the mild winter we’ve had) European storage has suffered little by way of withdrawals – with inventories at a record-breaking 60% versus the 5-year average of 40%.

Geo-political risk has become background noise over the past few weeks, with lingering shipping disquiet in the Red Sea area – though LNG has been mostly rerouted around the Cape of Good Hope until further notice.

With only 15 days of Winter-23 remaining buyers are looking to summer conditioning to further soften Winter-24 offers.

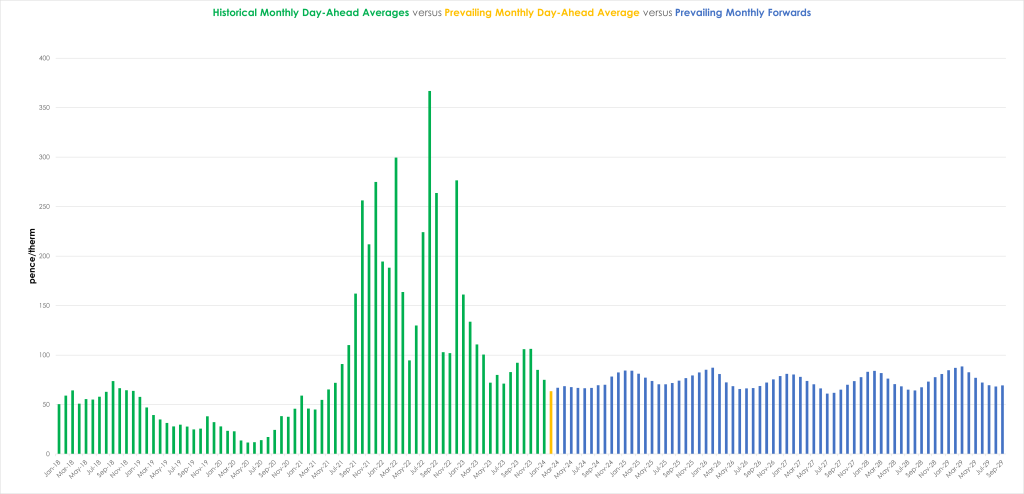

Monthly Day-Ahead averages are on target this month to achieve 67p/therm (or 2.28p/kwh).

ELECTRICITY & CARBON

Looking to the continent, rising temperatures and renewable production continued to weigh on short-term delivery prices in the latter part of this week – shedding circa. 20% in anticipation of lower demand and limited gas-for-power burn.

Nonetheless, prices may find support next week with forecasts of colder temperatures and weak renewables outputs.

Down the curve, markets firmed to end the week, though market participants struggled to identify a fundamental rationale for the upward movement, with some attributing it to potential positioning /short-covering.

On the carbon markets, prices remain rangebound with neither bulls nor bears managing to break above/below established support/resitance levels.

Any hope amongst bulls that carbon is ready for another rally seems premature – with many analysts preferinng to explain any upwards movement as market noise rather than a shift in fundamental sentiment.

UKAs closed the week at circa. £40/tn – with the prevailing range at £45/tn to the topside (and £30/tn to the downside).

Back in the UK, our electricity generation mix is bearish in nature to end the week with renewables contributing 43%, thermal at 18% (gas and coal) and low carbon at 25% (nuclear and imports).

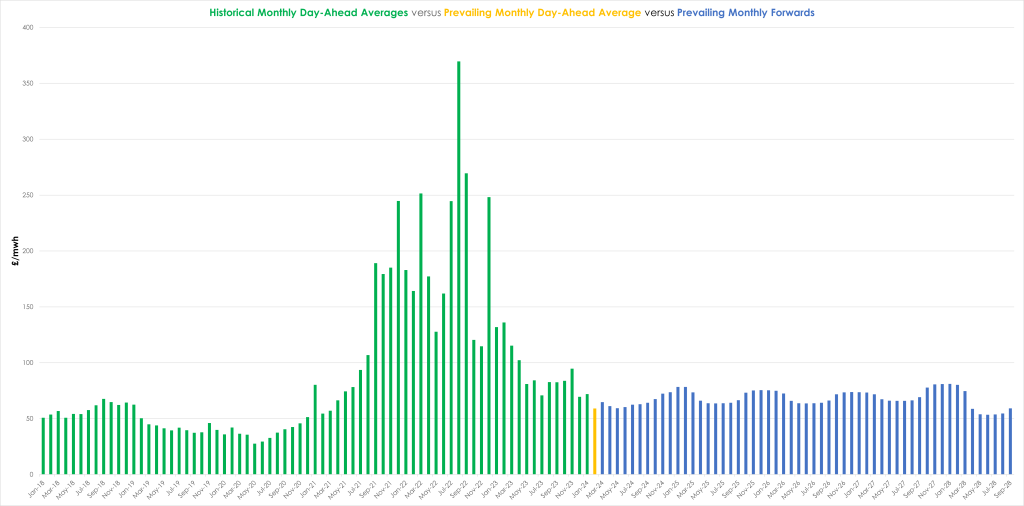

Monthly Day-Ahead averages are on target this month to achieve £65/mwh (or 6.5p/kwh).