In the last half hour or so, prices all the way down the curve have started to show signs of the market overheating.

We’re now 77 days into the conflict, and despite innumerable reassurances from Trump that it’s all coming to an end soon, the Strait remains closed and the markets look set to overheat in the coming days/weeks.

Inevitably, as the summer wears on (and fears abound over the impacts of El Nino), LNG demand in Asia is beginning to pick up, driven by seasonal norms and inventory restocking.

This is likely to intensify competition for an already tightening supply dynamic.

Notably, during the week ending 8th May, investment funds moderately reduced their net long positions on the TTF (European gas benchmark) by 3.5% (after an increase the week before) – so even the “smart money” is at a loss to know where this is all headed.

Hopes that the Trump/Xi summit this week would somehow bring about a diplomatic channel that would melt the impasse are fading – instead, all we heard following the conclusion of the summit in a statement from the White House was “the two sides agreed that the Strait of Hormuz must remain open to support the free flow of energy”.

Worryingly, yesterday in an interview on CNBC, US Treasury Secretary Scott Bessent said that “China has a much bigger interest in reopening the Strait than the US does. China is the largest oil importer in the world, with much of its crude coming from the Middle East. China will use its influence on Iran to help reopen the Strait of Hormuz. It’s very much in their interest to get the Strait reopened. I think they will be working behind the scenes to the extent anyone has any say over the Iranian leadership.”

And so, the US is making the re-opening of the Strait China’s problem.

Bessent went on to say, “The U.S. believes Iran’s storage tanks are full. None of the ships are getting out, none are coming in, so they’re not able to store oil on the water. They’re going to start shutting down the production. We can see that’s happening from satellite photos.”

And then he conveyed what many perceive to be the real reason behind the US’ de facto closure of the Strait of Hormuz, “China is interested in buying more US energy in response to the supply disruption in the Middle East. China and other nations are looking for more stable sources of energy. The US plans to ramp up oil and liquefied natural gas exports from Alaska, a natural place for China to import energy from, due to its geographic proximity. We think that not only China, but countries all around the world are going to look to diversify away from the Middle East for more stable sources of energy and what better place than the US?”

That being said, US LNG production is actually likely to remain lower than expected as feedgas levels are returning slowly – this will have a knock on effect and impact future supplies as US LNG bottlenecks following maintenance.

Cynics might point out that the US is in no rush to over-produce given that they’re the only show in town right now…

In other LNG news, strike action will begin today at Australia’s Woodside’s LNG plant (which could limit outputs if left unresolved).

Energy buyers across the globe have been waiting for 77 days to see how the conflict would play out.

To date, Israel’s war on Lebanon looks set to continue, and the US has been explicit in explaining why they’re in no rush to see the Strait re-open.

As such, beginning next week (unless a miracle happens over the weekend), we’ll be encouraging buyers with open volumes to hedge-out volumes for June delivery (and, if necessary, beyond).

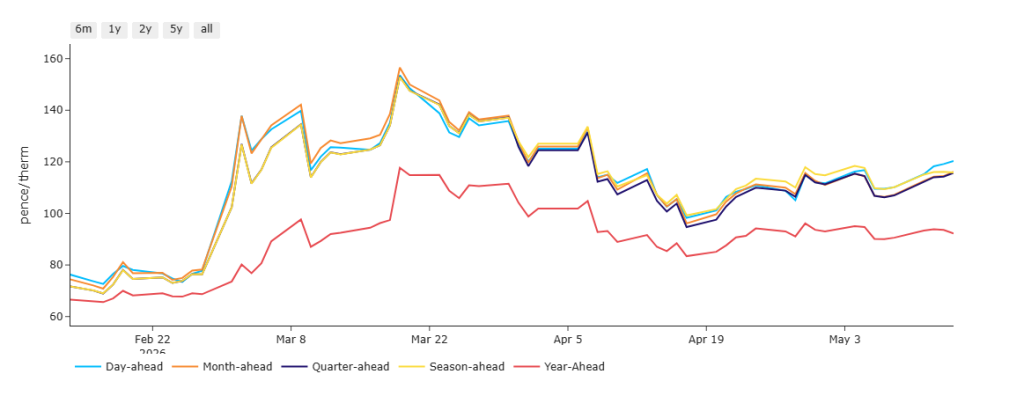

Monthly Day-Ahead Averages for the month have crept up to 114p/therm (or 3.9 p/kwh exc. non-gas) – as per the chart below, Day-Ahead has become the most expensive product on the market to finish the week – so, most of the risk is front-loaded.

ELECTRICITY & CARBON

Whilst UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb, I’m afraid the bulls have got the reins to finish the week.

This despite the fact that today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 56%, thermal at 10% (gas and coal) and low carbon at 21% (nuclear and imports).

On the trading side, beginning next week (unless a miracle happens over the weekend), we’ll be encouraging buyers with open volumes to hedge-out volumes for June delivery (and, if necessary, beyond).

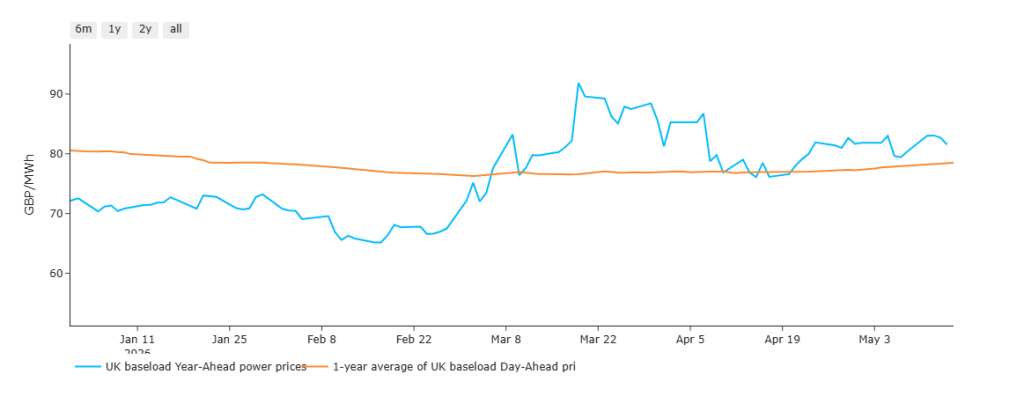

The chart below details UK electricity Year-Ahead prices versus the 1-Year Average of Day-Ahead prices since late-Feb.

By way of explantion, when the blue line is above the orange line, mid-term delivery prices are at a premium to an average of the last 12 months.

As you can see, prior to the onset of the US/Israeli offensive, prices were enjoying a soft-landing heading into Summer-26 – thereafter, Year-Ahead has remained consistently at a premium despite the otherwise ‘summery’ conditions.

Whilst the blue line remains above the orange line, it’s fair to conclude that prices are not as good as they should be (were it not for bullish geopolitical drivers).

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets.

However, correlation has now seemingly shifted to equities, which continue to enjoy a strong, tech-led rally.

At the time of writing, UKA mid-price Dec ’26 delivery is at £51.47/tn (and the spot is at early-50s).

Monthly Day-Ahead Averages for UK electricity for May so far are marginally down at £101/mwh (or 10.1 p/kwh exc. non-energy) off the back of low demand/summery conditions.