Markets remain on the slide, with near- and far-term prices drifting southwards.

Prices are down on the week/month/quarter/6-months.

In short, the bear-trend that began in Q422 is still in place.

Temperatures are set to peak circa. 7 degrees above seasonal norms into the weekend.

On the bullish side, wind outputs will drop off circa. 40% today/tomorrow, meaning higher-gas-for-power burn, and potentially increasing the rate of withdrawals.

Looking to the wider energy complex, European coal supply is in good shape and carbon remains in the doldrums.

With Summer-24 only 45 days away, only geo-political unrest poses any risk to a continuation of the prevailing bear trend.

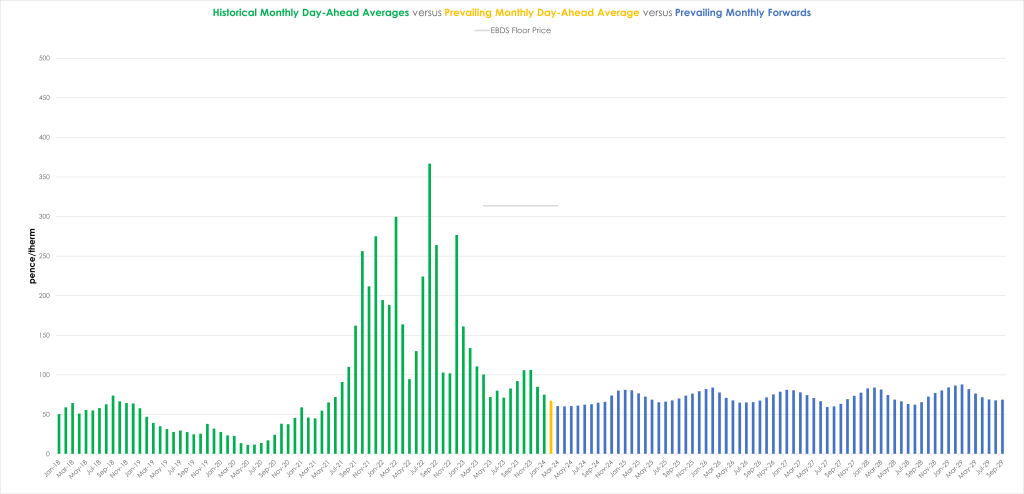

Monthly Day-Ahead averages are on target this month (so far) to achieve 67p/therm (or circa. 2.25p/kwh).

ELECTRICITY & CARBON ALLOWANCES

For the first time since 2018, Seasonal Forwards have assumed a contango state (future delivery prices more expensive than near-term delivery prices) – see chart.

Looking to the continent, near-term delivery prices dropped again yesterday driven down by weaker fuels and emissions prices along with expectations of slightly higher wind production and nuclear availability.

With European gas stocks at an all time high (66% versus the 5-year average of 53%), ongoing Industrial demand destruction and the “solar season” just around the corner with days getting longer, it’s difficult to see where any upward momentum might come from (save geo-political escalations).

UKAs (UK carbon allowances) are circa. £38/tonne with a retest of 29th Jan lows of £36/tonne surely very likely if EUAs fall further.

Back in the UK, our generation mix is bang-on neutral with renewables contributing 32% and gas-for-power burn at 32%.

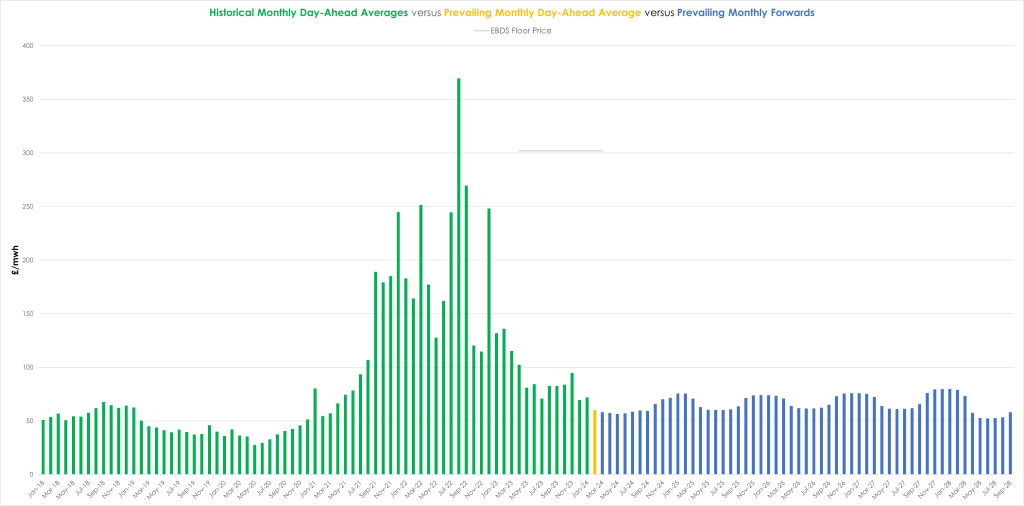

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £60/mwh (or 6p/kwh).