Winter is finally upon us, with forecasts for below seasonal-norm temperatures across Europe from next week supporting near-term delivery.

Temperatures are forecast to fall well below seasonal norms from 26th onwards – with some models showing days with an average of -8°C.

The cold front is being driven by a chilly Siberian airmass (often referred to as the “Siberian Express”) which is formed by radational cooling of Siberia’s massive snow covering (meaning high pressure is prevalent across most of the winter months).

The front is semi-permanent and produces some of the world’s lowest temperatures ordinarily accompanied by low humidity and driving winds.

The “Siberian Express” is forecast to sweep east to west across Europe and could linger for a fortnight or so.

The impact of Europe’s looming cold snap will likely see European gas prices post their highest weekly increase since late ’23 off the back of a spike in heating demand.

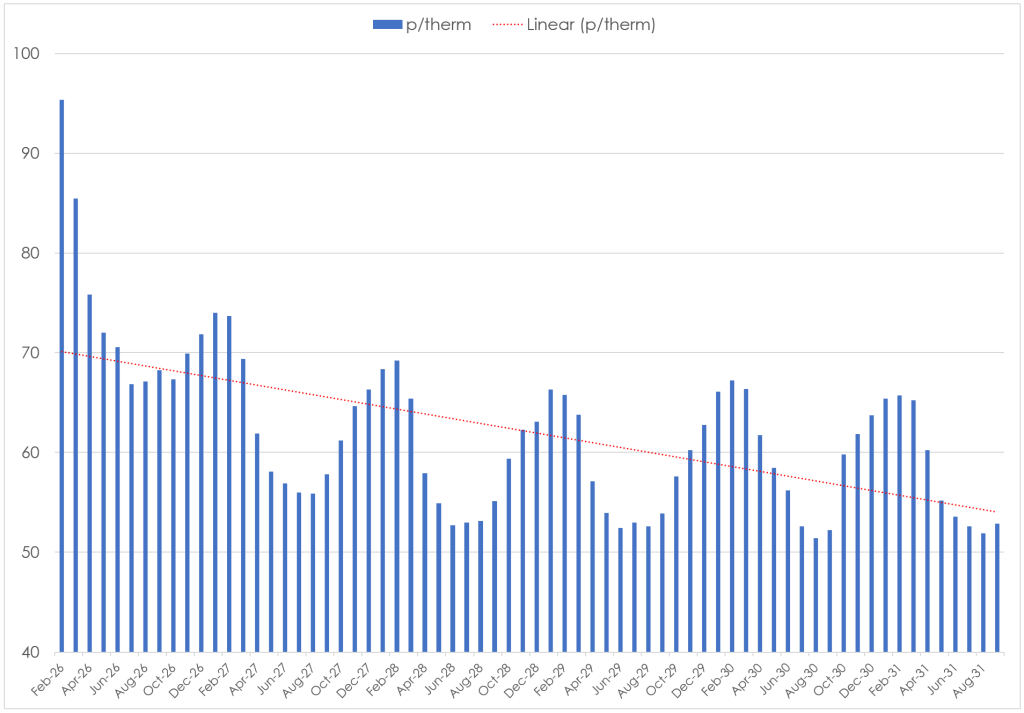

It’s evident from today’s Monthly Forward chart below that, for now, only the Front 2-months have surged in price in anticipation of the wintry conditions, whilst prices further down the curve remain unchanged from last week – so all being well, the long-term picture will remain bearish and we’ll all just need to weather the storm until late-Feb.

As for the UK, we’ll see temperatures begin to fall below seasonal norms as of 22nd onwards.

European storage inventories are down to 52% versus the 5-year average of 76%, so the rate of withdrawals has evidently picked up!

In short, demand is up, supply remains steady, storage is under pressure, and the bulls have the reigns for now.

Monthly Day-Ahead averages for January so far are at 79p/therm (or 2.7p/kwh) – though expect this to creep up in the coming days.

ELECTRICITY & CARBON

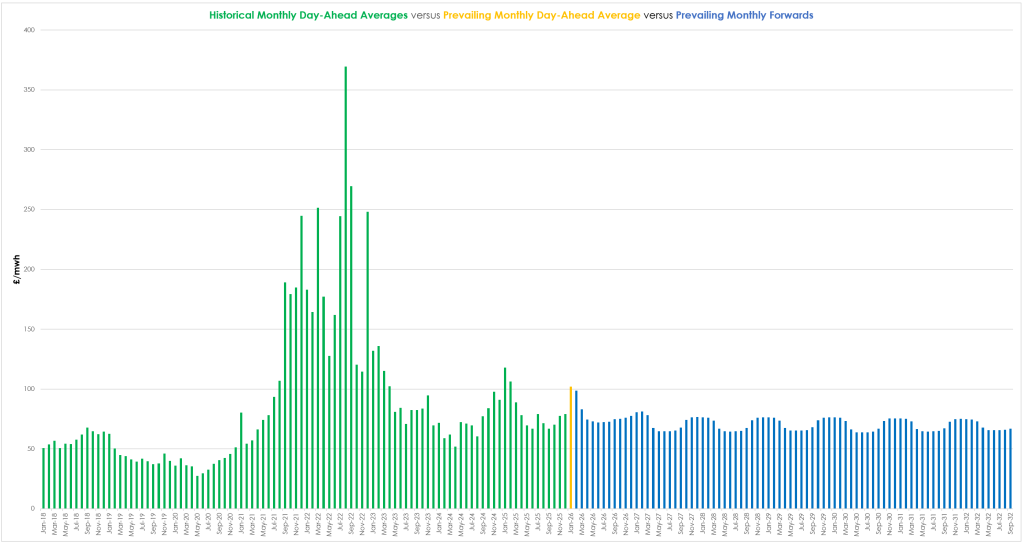

As per the chart below, prevailing Monthly Day-Ahead average prices for UK electricity are well above Monthly Forwards all the way down the curve – reflecting the news that the Siberan Express is on its way, but will not stay too long.

On the Carbon side of things, Dec-26 benchmark prices for UKAs saw a spike on Wednesday despite the auction clearing at £68/tn – an announcement by the EU that talks to merge UKAs and EUAs are going well gave speculators all the ammunition they needed to take the market significantly higher.

Other bullish drivers for UKAs include 200,000 fewer credits available at auction each fortnight (than was the case in ’25) coupled with a general reduction in free allocation being implemented across sectors for ’26 into ’27.

UKAs are up more than 100% versus 12-months ago.

Compliance buyers (whose activity in the market is eclipsed by the investment funds) can only look on from the sidelines fearing the worst.

UKA spot prices on the secondary market remain at an approximate £2/tn discount.

Today’s UK electricity generation mix is bullish in nature – specifically, renewables are contributing 42%, thermal at 15% (gas and coal) and low carbon at 19% (nuclear and imports).

Monthly Day-Ahead averages for January so far are looking very wintry at £102/mwh (or 10.2p/kwh exc. non-energy).