Markets have spent the week dropping-off in the mornings, then picking-up in the afternoons.

Neither bulls nor bears have enjoyed the meaningful momentum needed to breakout of the prevailing range-bound price action.

All eyes remain on the outcomes and impacts of China-US trade relations, and Ukraine peace talks.

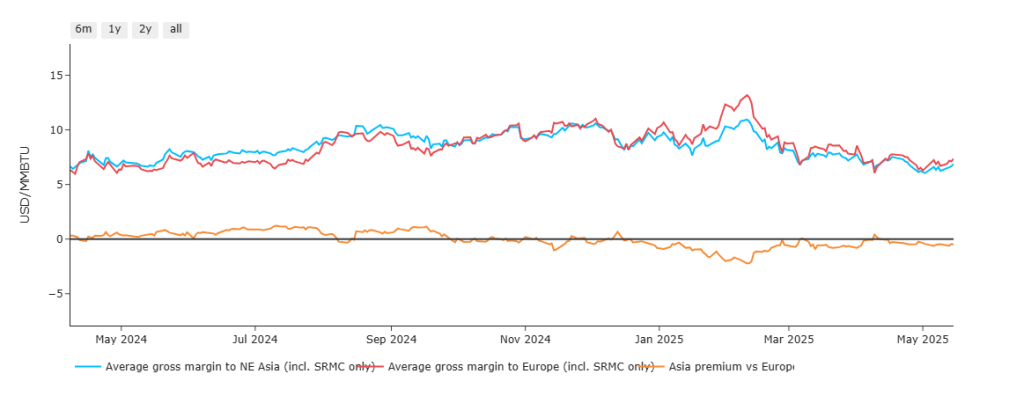

Looking at US LNG netbacks (the profit margin achieved by a US LNG cargos after factoring in transportation and other costs), it remains more profitable to be degasifying at European/UK ports than those across Asia (please see chart below).

On the supply side then, Europe will continue to face the threat of competition from Asian LNG buyers as the summer progresses, and must also keep a close eye on the feedgas issues of some LNG producers (feedgas being the raw natural gas that is delivered to a liquefaction facility via pipeline to be converted into LNG).

These combined risks contribute to ongoing price support, leaving little opportunity for further price declines (unless Russian flows are reintroduced to the European system).

On the other hand, the relative weakness of oil values (which then limits the willingness of Asian LNG buyers to pay over the odds for gas when they could use oil) is limiting demand for LNG across Asia.

As such, key drivers are both supporting and a keeping a lid on prices – so range-bound price action right now makes sense.

All-important European storage levels are at 44% versus the 5-year average of 55% – having risen from 42.50% at the start of the week (thanks to healthy ‘summery’ injections).

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst the going’s good – and whilst so many geopolitical variables remain outstanding.

This month’s UK gas Day-Ahead averages are holding steady at 80p/therm (or approx. 2.7p/kwh excluding non-gas).

ELECTRICITY & CARBON

Electricity remains tethered to gas movements (as you’d expect given the UK’s ongoing reliance on gas-for-power generation).

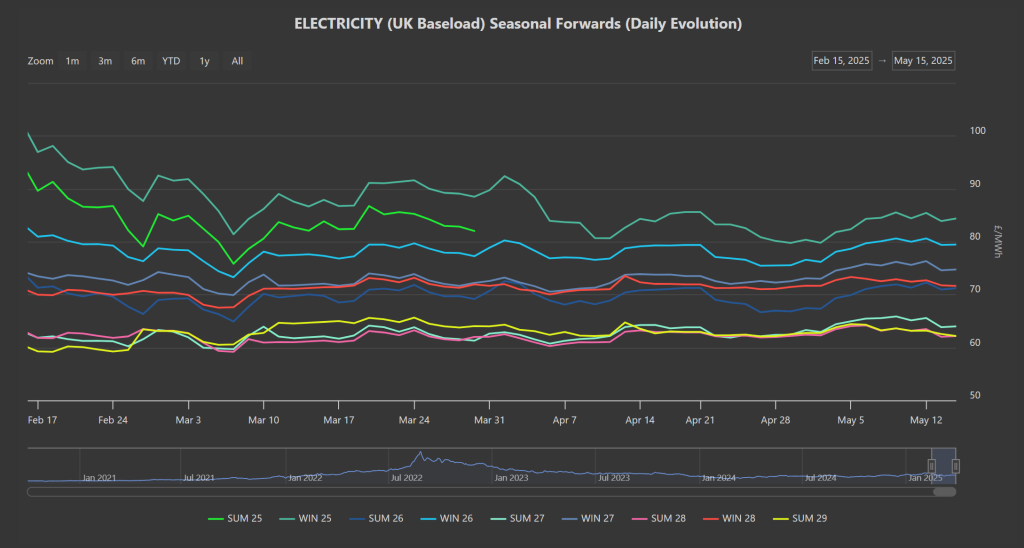

Winter-25 prices are drifting northwards, away from the £80/mwh level which has failed to break to the downide on multiple occasions over the last year or so (Apr’24/Sep’24/Dec’24/Mar’25, then twice this month so far).

So it’s fair to conclude that £80/mwh (or 8p/kwh) represents the market-bottom for Winter-25 right now.

UKAs (mandatory carbon credits) dropped like a stone earlier in the week (off the back of low demand, improved renewables outputs) but failed the break below £46/tn – at the time of writing, we’re back up at £49.75/tn off the back of firmer gas prices.

Nonetheless, today’s UK electricity generation mix is bearish in nature reflecting high temperatures and good renewables outputs – specifically, renewables are contributing 59%, thermal at 5% (gas and coal) and low carbon at 30% (nuclear and imports).

So far this month, electricity Day-Ahead averages are holding steady at £74/mwh (or approx. 7.4p/kwh excluding non-energy).

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst the going’s good – and whilst so many geopolitical variables remain outstanding.

It’s worth noting that Summer-27/Summer-28/Summer-29 are currently offered in the £60s/mwh; Summer-26/Winter-27/Winter-28 are being offered in the £70s/mwh – please see Seaonsal Forwards chart below.