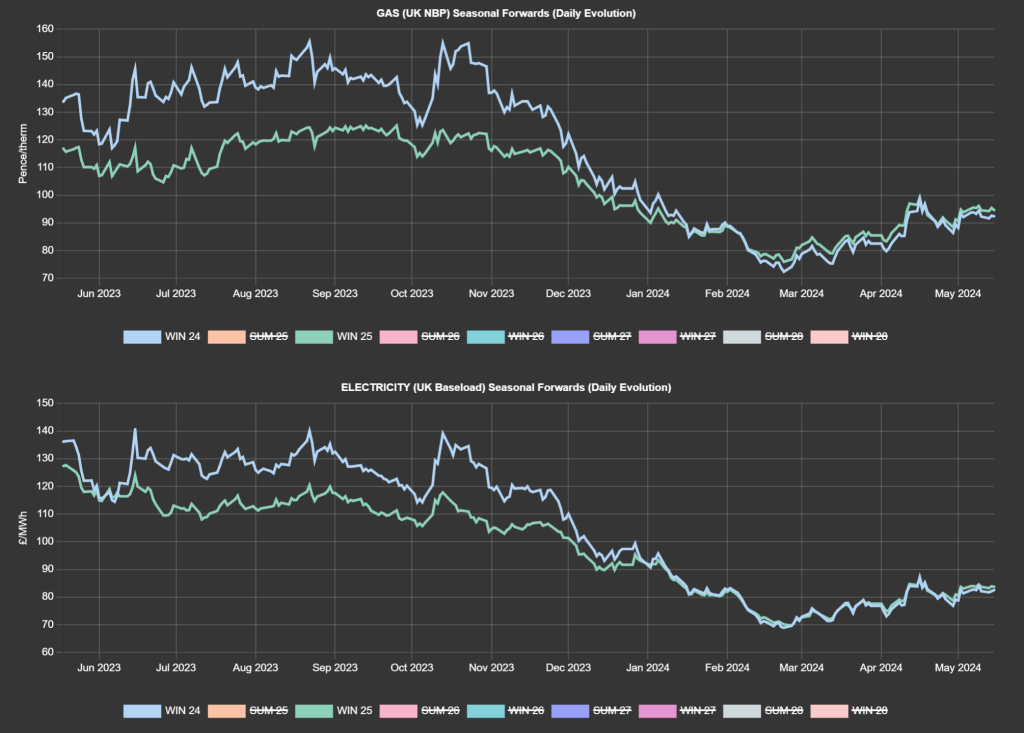

Looking specifically at Winter-24/Winter-25 delivery (currently the highest priced seasons down the curve), delivery prices fell below historical support levels in Dec ’23 and dropped off throughout Q124 (see chart).

Winter-24/Winter-25 prices then established a market bottom/support in late Feb, and have been on a shallow rise to date – though markets are currently below the recent highs printed mid-Apr’24.

As such, market participants are watching closely as summer conditions deepen to see if prices will retest the Feb’24 lows or if prices will remain rangebound throughout Summer-24.

137 days of Summer-24 remain – historically, June is the month which marks the “bottom” of summer value – so watch this space.

Lower activity at US LNG facility freeport, possibly due to a massive storm in the region, has buoyed the energy complex this morning – though prices are meandering back down at the time of writing.

European LNG imports have now fallen below the 30-day moving average – though of course, MRS (European gas storage) is 66% full verus the 5-year average of 47% – easing the supply/demand dynamic across Europe/UK.

Notably, China’s gas production has risen 5% so far this year with some analysts predicting a break of 2023’s record for LNG imports (fuelling higher prices due to global competition for cargoes).

Norway’s scheduled summer maintenance will take significant volumes offline beginning 21st May – no doubt providing additional price support.

Off the back of a drone strike on another Russian oil refinery today, concerns abound over security of underwater pipelines – with intelligence suggesting that energy infrastructure beyond Russia and Ukraine’s borders is very much at risk of sabotage.

Back in the UK, we’re expecting 3 LNG arrivals before month-end with Asian buyers thanksfully putting the brakes on.

Unscheduled maintenance at the UK’s South Hook LNG terminal yesterday resulted in a 6-hour shutdown which added to supply jitters – though the problems have been resolved and LNG sendout going forward is not expected to be impacted.

In short, it’s as you were – rangebound price-action – it would be fair to liken the markets to a windless ocean (flat for now, but the winds will inevitably return!)

Markets remain at equilibrium with geopolitical support at odds with seasonal pressure (falling demand/solid supply/less reliance on withdrawals etc).

Monthly Day-Ahead averages are on target this month to achieve 72p/therm (or circa. 2.45p/kwh excluding non-gas).

ELECTRICITY & CARBON

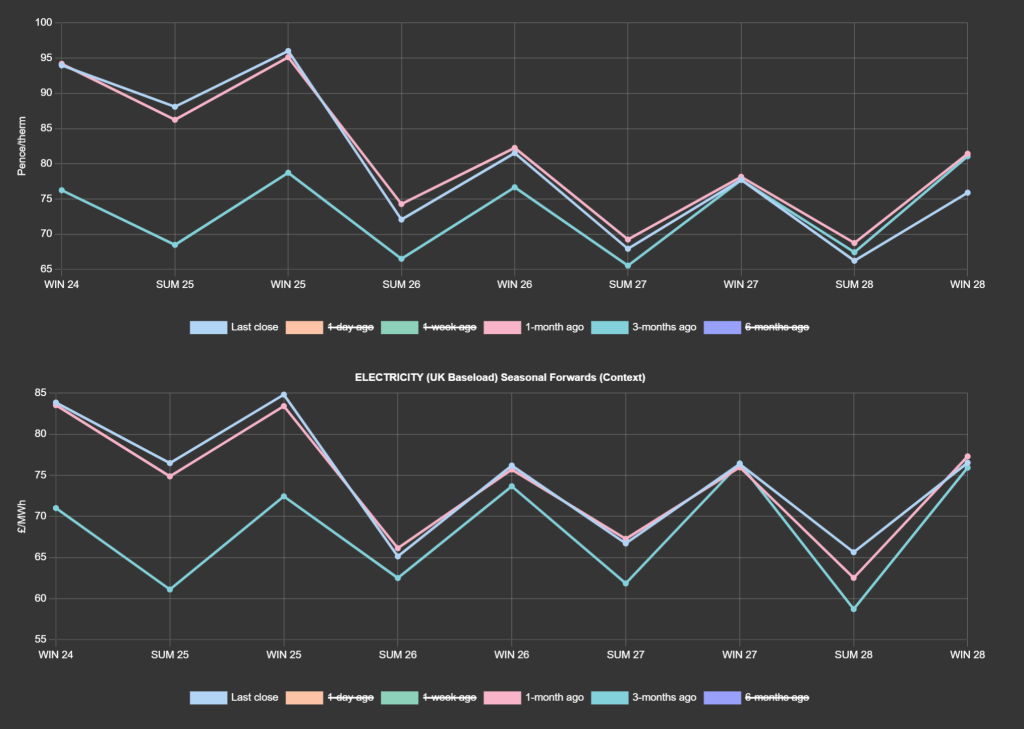

Seasonal Forwards down the curve are pretty much unchanged versus 1-month ago – but significantly up versus 3-months-ago (see chart).

Looking to the continent, near-term delivery prices found support yesterday on forecasts of falling solar generation.

On the carbon markets, prices posted noticeable gains yesterday attributed mainly to firmer gas prices amid prospects of lower renewable outputs and scheduled Norwegian maintenance.

The EUA (European Carbon Allowances or EU-ETS) Dec’24 benchmark has already climbed this morning – likely headed to test its 200-day moving average if gas prices remain firm.

Back in the UK, UKAs (UK Allowances) are trading at £39.9/tn (Dec-24 benchmark) – having broken above the highs printed on 25th Mar ’24.

Our electricity generation mix is neutral in nature today with renewables contributing 30%, thermal at 30% (gas and coal) and low carbon at 26% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £70/mwh (or 7p/kwh excluding non-energy).