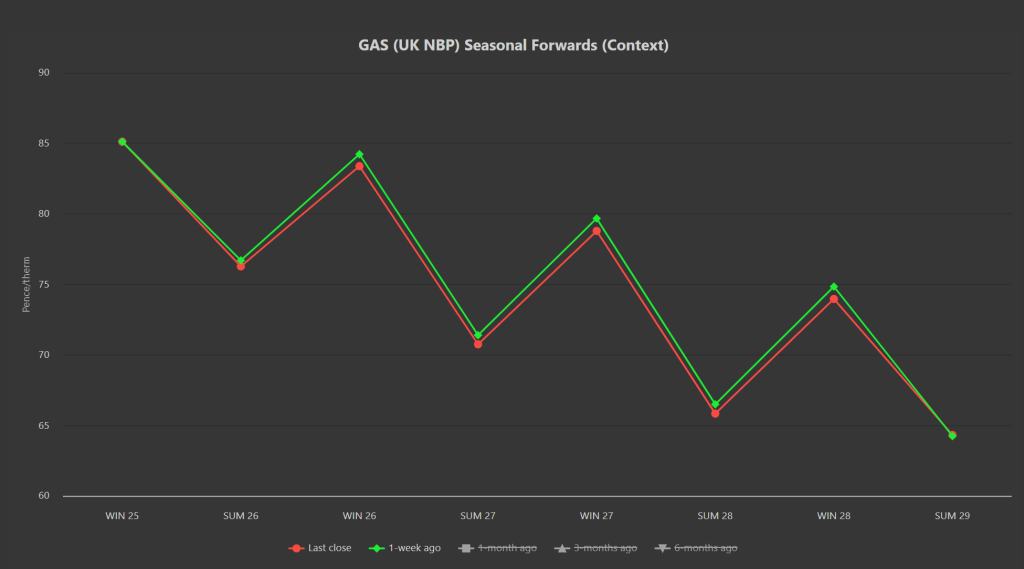

Seasonal Forward prices are very marginally down versus 1-week ago (please see chart below).

It’s been another sedate week on the markets amid continued stable fundamentals.

The end of maintenance at both Dvalin and Oseberg has inevitably resulted in improved Norwegian flows into Europe/the UK.

After a week of heavy gas-for-power burn, temperatures into the weekend look set to climb above seasonal norms coupled with improved wind outputs – so pressure on storage withdrawals should ease.

European storage is at 83% versus the 5-year average of 95% – so, with the heating season due to begin in only a couple of weeks, all eyes will be on mid-to-long range weather forecasts.

In other news, market participants are keeping one eye on Russia’s energy trade (and the resumed US efforts to mediate a peace agreement in Ukraine).

Following Trump’s announcement that he intends to meet with Putin again soon, prices fell only briefly – reflecting that traders don’t necessarily share Trump’s confidence.

All in all, a quiet news week, and a balanced market.

Monthly Day-Ahead averages for October remain at 78p/therm (or 2.66p/kwh exc. non-gas).

In short, whilst Winter-25 has officially begun, we’re yet to feel the effects of increased demand/increased withdrawals/worries over supply tightness.

And so, whilst momentum remains neutral, traders are all too aware of the fragility of the European gas balance.

ELECTRICITY & CARBON

Not surprisingly, electricity prices have mirrored the low volatility of gas markets.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are bracketing in a triangle/consolidation pattern (please see chart below).

At the time of writing, prices are holding steady in the mid-50s (currently at £56/tn) – having failed to break out of the triangle to the downside earlier this week.

The secondary market remains at a discount to auction settlement prices – reflecting increased speculative interest in emissions as winter deepens.

Today’s UK electricity generation mix is bullish in nature – specifically, renewables are contributing 10%, thermal at 54% (gas and coal) and low carbon at 22% (nuclear and imports).

Monthly Day-Ahead averages for October so far are at £77/mwh (or 7.7p/kwh exc. non-energy).