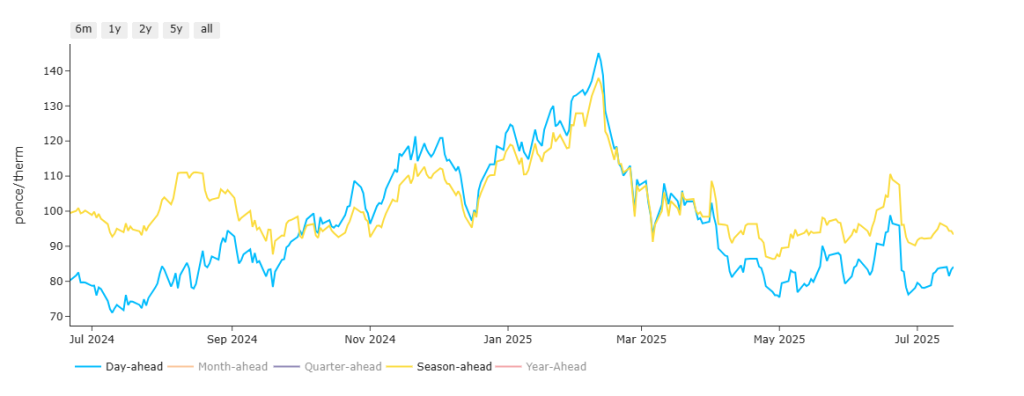

The chart below illustrates nicely how markets have resumed a traditional summer/winter risk dynamic following the comparatively unpredictable chaos that was ’21 to ’23.

Clients can increasingly rely on low Day-Ahead prices across the summer months with a view to hedging winter delivery in advance of the shoulder month (September).

Likewise, during the Winter-24 months, Day-Ahead and Season-Ahead drifted along at near-parity – will they do the same again this year?

Right now, the monthly Day-Ahead average for July to date (81p/therm, or 2.77p/kwh), remains at a 14% discount versus Winter-25 – this time last year, that same differential was 20%.

So, if recent history is anything to go by (in the absence of any overwhelming geopolitical disquiet), it’s likely we’ll see modest Day-Ahead increases in Aug/Sep ’25 amid a fairly flat Winter-25 offering.

However, looking at the chart should serve as a caution to FLEX buyers not to wait too long before pulling the trigger on Winter-25 transactions.

If the prevailing shape holds, come Sep ’25, the blue price line (Day-Ahead) will approach parity with the yellow price line (Season-Ahead) and remain as such until the onset of Summer-26 (at which point the reverse will hopefully repeat).

Of course, we don’t know what’s in store over the winter – but so long as storage targets are hit by Oct ’25 (and the winter is not too cold and still), it’s surely not overly optimistic to predict another soft landing in Summer-26 (and hopefully another cost-efficient Day-Ahead float for Industrials).

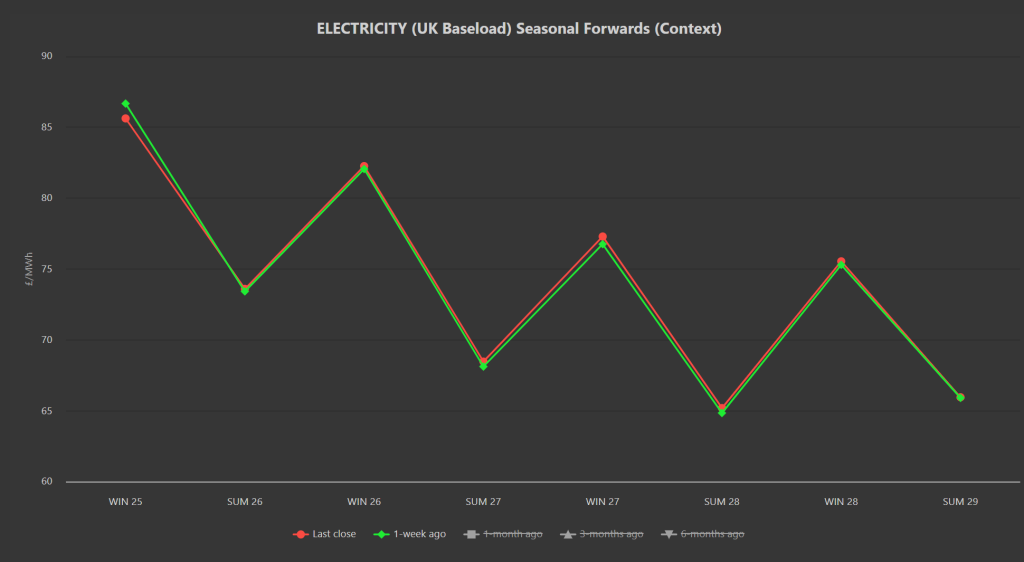

Anyway, back to now, it’s been another rangebound week for Seasonal Forwards with prices very marginally down versus 1-week ago.

Looking forward, fundamentals are in good shape, with the second half of the year seeing an extra 7 million tonnes of LNG per annum (mtpa) coming online from the second phase of Plaquemines in the US, as well as another 14 mtpa from LNG Canada.

On the storage side of things, Europe’s inventories are now at 64% versus the 5-year average of 75% – so a little off the pace.

However, Norwegian flows are back up above the 10-day noving average with Nyhamna and Kollsnes coming back online – so withdrawals will decrease and injections should pick up again heading into next week (temperatures are forecast to remain above seasonal norms for the remainder of the month).

Whilst US LNG cargoes are still making more money by heading to Europe over Asia, market participants continue to eye cautiously the impacts of Asian temperatures (and the corresponding cooling demand).

Back in the UK, monthly Day-Ahead averages for the month so far are at 81p/therm (or approx 2.77p/kwh excluding non-gas).

In short, price equilibrium is holding amid steady fundamentals and (dare I say it), Trump’s (perhaps unintended) calming influence!

ELECTRICITY & CARBON

Seasonal Forward prices are pretty much flat versus 1-week ago – please see chart below!

Winter-25 has traded in a tight range between £84/mwh at £88/mwh all week.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

At the time of writing, Dec ’25 UKA benchmark prices are at £49.51/tn on the mid-price.

Today’s UK electricity generation mix is fairly neutral in nature reflecting so-so renewables outputs today – specifically, renewables are contributing 39%, thermal at 21% (gas and coal) and low carbon at 25% (nuclear and imports).

Monthly Day-Ahead averages for the month are at £78/mwh (or approx 7.8p/kwh excluding non-energy).