At the end of a relatively flat/directionless/balanced week, Seasonal Forwards are marginally down on the week, but still up versus 1-month/3-months/6-months ago.

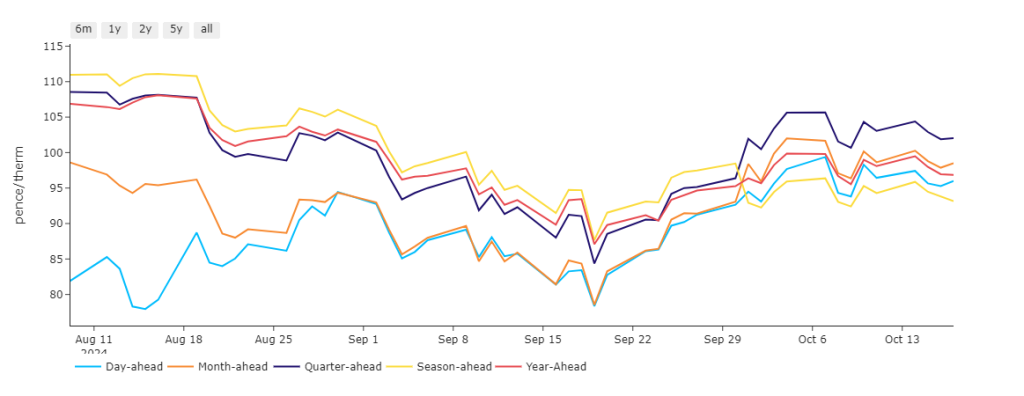

It’s not surprising then (given the absence of volatility) that Prompt pricing (Day/Month/Quarter/Season/Year-Ahead) are flat for the week and at near parity – all priced within 9% of one another (see chart below).

As of this morning, all Seasonal Forwards down the curve have found their way back below 100p/therm off the back of temperatures above seasonal norms meaning reduced heating demand, and solid wind outputs forecast for the coming days reducing gas-for-power demand.

Geopolitically, fears over global supply disruption should conflicts escalate is evidently priced-in – as such, even the confirmed killing of Yahia Sinwar (the alleged mastermind of Hamas’ 7th Oct attack on Israel) has had little to no impact on market sentiment.

On the supply side, extended Norwegian outages are limiting flow into Europe and the UK – though the picture is much improved versus the end of Sep-24.

Demand has returned to seasonal norms today (after a couple of weeks being above seasonal norms) amid a backdrop of European storage at 95% fullness versus a 5-year average of 95%!

For now it would seem markets have found an uneasy equilibrium, and current prices represent fair value.

Increasingly, Chinese economic indicators are reinforcing fears of deflation and underline the need for meaningful stimulus measures – though the Communist Party remain reluctant to devalue the yuan and trigger capital flight (which seems inevitable).

Monthly Day-Ahead averages so far this month are on target to achieve 96.161p/therm (or approx. 3.281p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking at UKAs Dec-24 benchmark on the hourly charts, prices have been observing a rising trend channel since the 7th Oct lows of circa. £35/tn – currently siting at £38.57 (see chart below).

MACD is divergent, volume is low, and ATR (average true range) is falling reflecting surely an unconvincing bullish trend.

Looking at UK electricity, the front 3 seasons (Summer-25/Winter-25/Summer-26) are barely changed versus 1-week/1-month/3-months/6-months ago – only a 2% difference!

This reflects of course how flat Seasonal Forwards have been since the onset of Summer-24 following a 50% drop over Winter-23.

As with gas, an absence of volatility has taken hold with Winter-24 now upon us and global conflicts having little or no impact on current supply/demand dynamics.

UK electricity prices remain comfortably below £90/mwh front to back, all the way down the curve.

Our electricity generation mix is neutral in nature today with renewables contributing 38%, thermal at 37% (gas and coal) and low carbon at 13% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £82.163/mwh (or approx. 8.22p/kwh excluding non-energy).