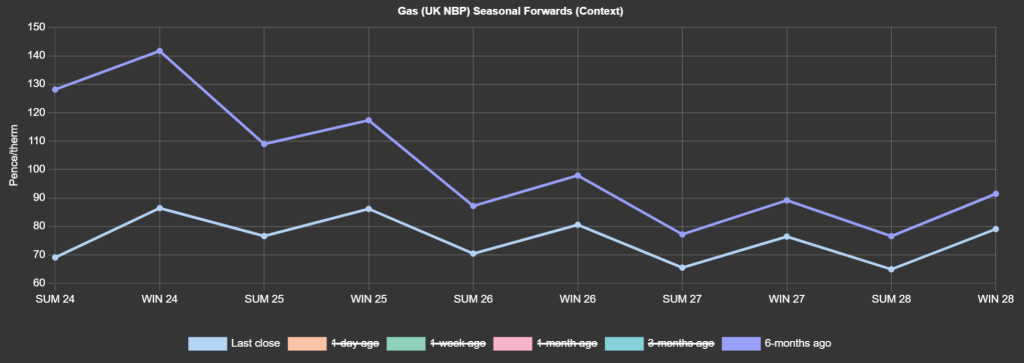

Notably, Summer-24 delivery prices are now at a 47% discount versus 6-months ago at the height of Summer-23 (see chart).

The cold spell is on its way out – with the prospect higher temperatures overnight and a weekend of milder, windier conditions, no doubt exerting bearish pressure on prices to start next week.

Demand has fallen to its lowest levels since the start of the week against a backdrop of improving weather and Norwegian flows comfortably above the 5-day average.

Nonetheless, near-term delivery prices have closed the day marginally firmer versus yesterday’s close.

Geo-political risk persists in the form of Middle East escalations and lingering worries over supply disruption in the Red Sea/Suez Canal.

Monthly Day-Ahead averages are on target this month to achieve 79p/therm (or 2.7p/kwh).

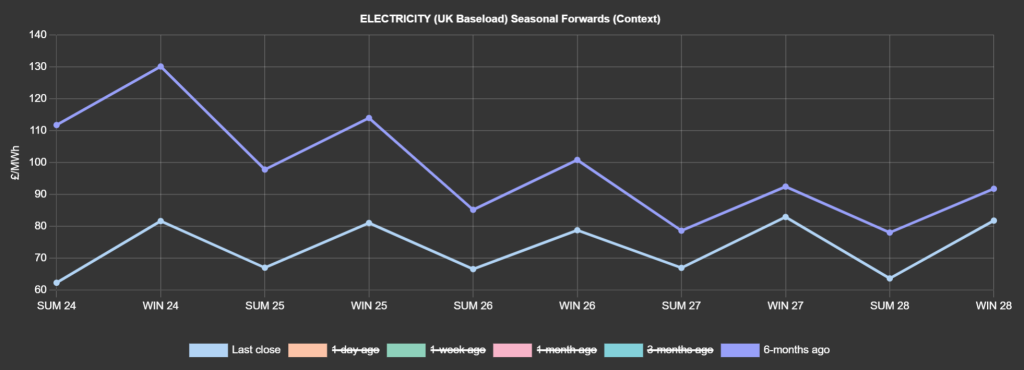

ELECTRICITY

Mirroring gas, Summer-24 delivery prices are now at a 45% discount versus 6-months ago at the height of Summer-23 (see chart).

Looking to the continent for signals, consensus amongst analysts anticipates a plunge caused by strong renewables output coupled with temperatures forecasted to rise by up to 6°C above seasonal norms – limiting heating demand and gas-for-power generation.

French nuclear availability is also forecasted to expected to increase by next weekend, exerting further bearish pressure.

Consensus is building that UKAs may go as low as £30/tonne next week.

Back in the UK, our generation mix is neutral to bearish with 47% gas-for-power burn and 36% renewables.

Monthly Day-Ahead averages are on target this month to achieve £78/mwh (or 7.8p/kwh).