As has been evident for some time, Israel’s unwillingness to curtail its invasion of Lebanon represents the biggest risk to peace across the Middle East.

Whilst markets breathed a collective sign of relief when Trump and Iran signed the MoU (Memorandum of Understanding) on Wednesday, subsequent fighting between Israel and Hizbollah resulted in the postponement of peace talks between the US/Iran scheduled to take place in Geneva today (increasing uncertainty over the full reopening of the Strait of Hormuz and reintroducing marginal risk-remium into Forward prices).

And so it would seem, the US and Israel are no longer on the same page – Trump said on Thursday night that he expected “a complete ceasefire on all fronts, including Lebanon, Hezbollah, and Israel.”

What’s now entirely clear is that Trump regards the Iran crisis as a risk to his second term – so market participants remain confident that a resolution to the Strait of Hormuz closure remains likely, even if it means damaging the US/Israeli coalition.

Nonetheless, markets are firmer today reflecting a fear that Israel will not come to heel despite Trump’s claims that he’s in charge.

Thankfully, warmer weather forecasts and solid renewables outputs are keeping a lid on today’s renewed set of worries (limiting demand).

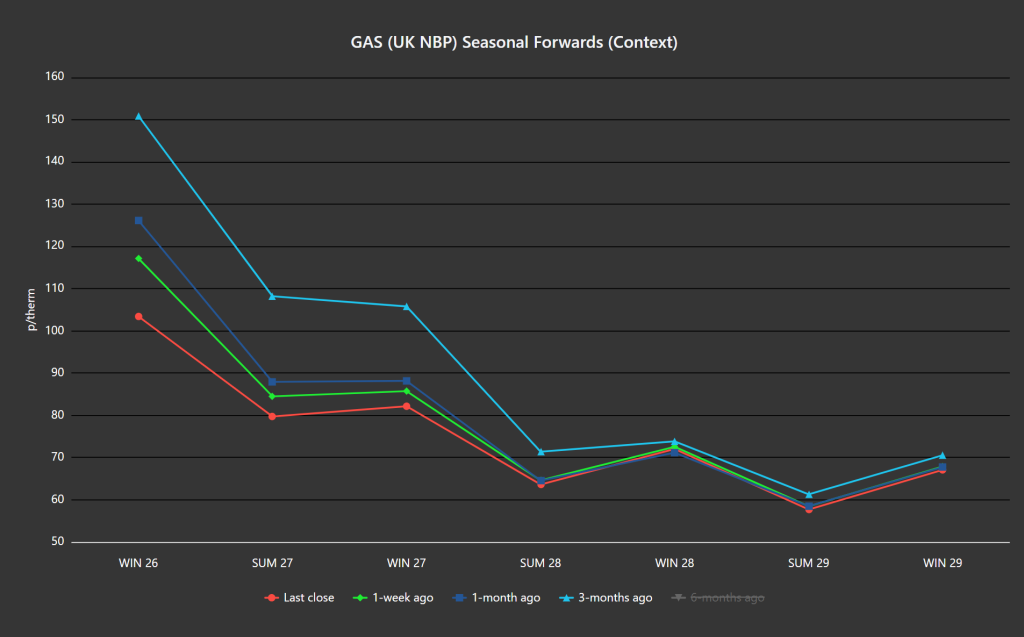

As of last night’s closing prices, Seasonal Forwards were down on the week/month/3-months ago – please see chart below.

On the supply side, European storage numbers are well off the pace again – fullness is now at 46% versus the 5-year average of 67% (so the reopening of the Strait is essential if we’re to successfully replenish storage in time for the onset of Winter-26).

On the FLEX side, as has been the case all summer, it’s a case of buying short-term delivery in the dips pending a resolution to the crisis – so all eyes are on the US to see how they deal with Israel’s disobedience.

Monthly Day-Ahead Averages for June so far have fallen to 114 p/therm (or 3.9 p/kwh exc. non-gas).

ELECTRICITY & CARBON

UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb – primarily due to summery conditions, solid renewables outputs (meaning lower gas-for-power generation).

Today’s UK electricity generation mix remains bearish in nature – specifically, renewables are contributing 52%, thermal at 14% (gas and coal) and low carbon at 22% (nuclear and imports).

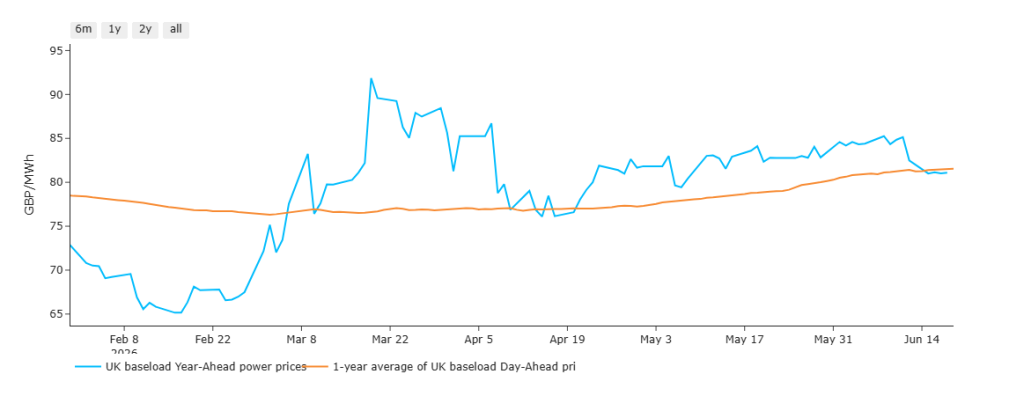

The chart below details UK electricity Year-Ahead prices versus the 1-Year Average of Day-Ahead prices since late-Feb.

By way of explanation, when the blue line is above the orange line, mid-term delivery prices are at a premium to an average of the last 12 months.

As you can see, prior to the onset of the US/Israeli offensive, prices were enjoying a soft-landing heading into Summer-26 – thereafter, Year-Ahead has remained consistently at a premium despite the otherwise ‘summery’ conditions.

However, following this week’s optimism, the blue line is back below the orange line for the first time since mid-April reflecting a significant shift in sentiment.

On the Carbon side of things, Dec-26 UKA delivery is at £60/tn (and the spot is at early 59s) in anticipation of EUETS/UKETS linkage beginning ’28 (so UKAs are rising to parity).

On the FLEX side, as has been the case all summer, it’s a case of buying short-term delivery in the dips pending a resolution to the crisis – so all eyes are on the US to see how they deal with Israel’s disobedience.

Monthly Day-Ahead Averages for June so far have fallen to £91/mwh (or 9.1 p/kwh exc. non-energy).