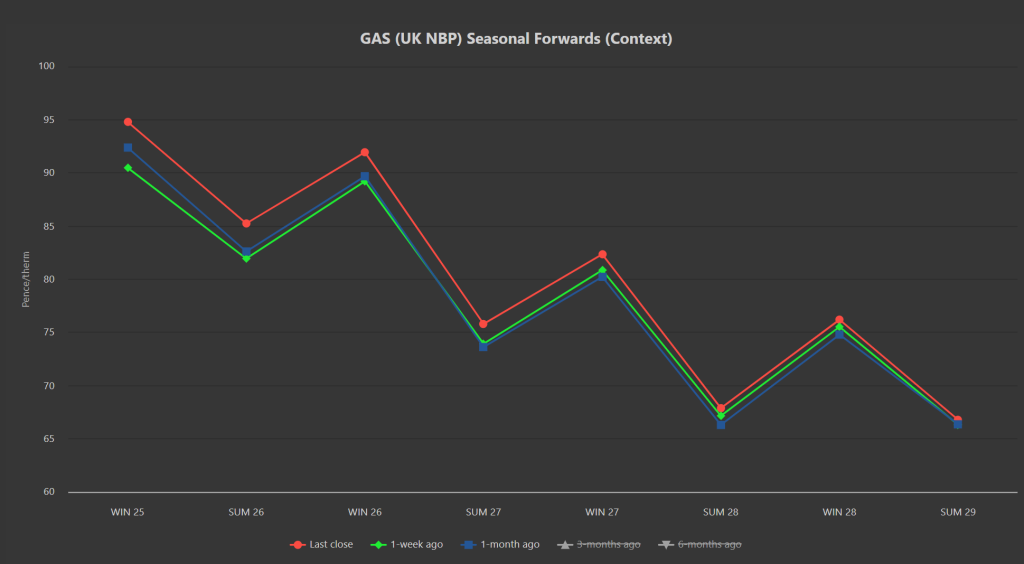

Seasonal Forwards are finishing the week (very marginally) up versus 1-week ago/1-month ago – please see chart below.

This afternoon however, we’re seeing live prices drop off a little (reflecting very good renewables outputs, limiting gas-for-power burn).

In short, all noise aside, both near- and far-term delivery prices remain reangebound/balanced.

Supply is good, demand is seasonal amid forecasts suggesting next week will be warm and windy.

There’s little on the news front – with Trump imposing tariffs that have been trailed for months; Russia seemingly indifferent to Trump’s threats of further sanctions; the US making noises that Trump is a humanitarian and remains determined to help starving Gazans.

So, yes, just news featuring Trump!

European storage remains on track to hit required levels before the onset of the heating season (Nov) with fullness at 68% versus the 5-year average of 79%.

With August now upon us, any clients with significant open volumes for Winter-25 delivery will be minded not to wait too long (as late-Aug/early-Sep can become spiky).

Whilst nobody knows if this market will fall further, we can say for sure that Seasonal Forwards have failed to retest the late-Apr lows despite overwhelmingly benign conditions.

So it’s fair to conclude that supportive elements (primarily geopolitical risk threatening supply security) are limiting downside (along with the need for European/UK prices to stay high so as to discourage LNG vessels from heading to Asia).

July’s Monthly Day-Ahead average came in at 81p/therm (or approx 2.75p/kwh excluding non-gas) – so that’s April/May/June/July all in the 80s (a steady float across the summer for many FLEX clients).

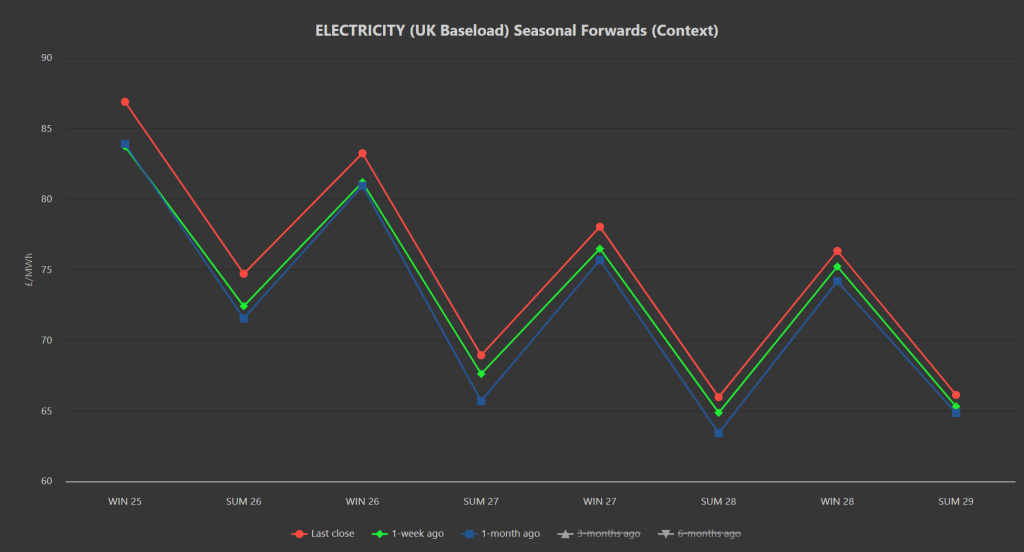

ELECTRICITY & CARBON

Seasonal Forwards are finishing the week (very marginally) up versus 1-week ago/1-month ago – please see chart below.

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are at £49.99/tn on the mid-price.

Today’s UK electricity generation mix is very bearish in nature – specifically, renewables are contributing 52%, thermal at 9% (gas and coal) and low carbon at 24% (nuclear and imports).

July’s Monthly Day-Ahead average came in at £79/mwh (or approx 7.9p/kwh excluding non-gas) – so that’s April/May/June/July achieving between £66/mwh to £79/mwh (a steady float across the summer for many FLEX clients).