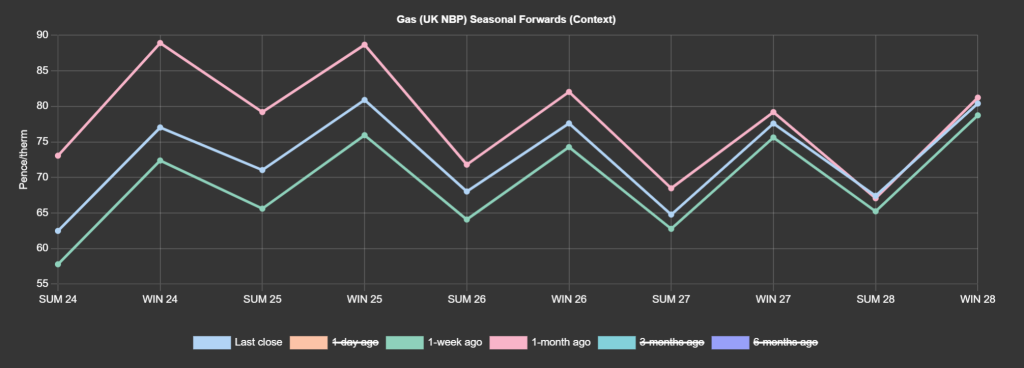

Looking down the curve, Seasonal Forwards are up on the week but down on the month (see chart).

To end the week, prices are little changed versus yesterday’s close.

The UK system was short at this morning’s open (demand outstripping supply) against a backdrop of higher heating demand and reduced LNG send-out.

Depending on which weather report you believe, there’s a colder weekend in the offing – but temperatures are expected to be back above seasonal norms once Monday rolls around.

On the supply side, an unscheduled outage at Norway’s Troll Field is lending support to near-term delivery contracts.

Notably, and for the first time since 2021, China’s LNG imports increased by circa.15% to hit a record high in February (raising jitters about increased global competition for LNG cargoes).

All in all, it’s been a week of muted volatility and sideways price action, with markets having found relative equilibrium.

With only 30 days to go until the onset of Summer-24, surely only geo-political unrest poses any risk to a continuation of the prevailing long-term bear trend.

European storage looks set to finish the winter with more than 50% left in the tank – currently at 63% versus 5-year average of 43%.

Monthly Day-Ahead averages for February ended up at 64p/therm (or circa. 2.2p/kwh).

ELECTRICITY & CARBON ALLOWANCES

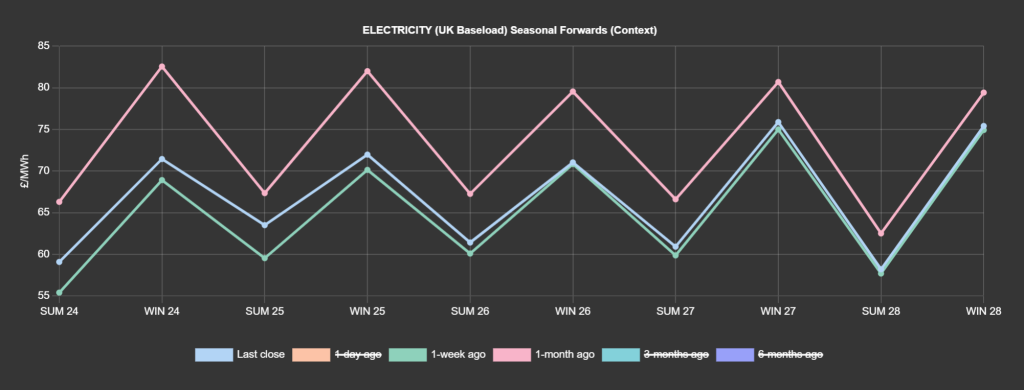

Down the curve, Seasonal Forwards are up on the week but down on the month (see chart).

Looking to the continent, European near-term delivery prices look set to finish the week marginally higher – supported primarily by anticipation of weaker renewables outputs and lower temperatures.

Expect more of the same into the early part of next week.

Far-term delivery contracts are relatively directionless.

All in all, the prevailing (and unchanged) bearish fundamental outlook is keeping a lid an any meaningful upside.

On the European/UK carbon markets, it’s the same story, tight rangebound trading, low volatility.

The upcoming COT (Commitment of Traders report) will be released on 6th March and should shed light on the extent to which the recent rebound was fueled by short-covering (reducing sell exposure) and strategic purchasing from compliance players (Industrials) capitalizing on what feels like a market bottom.

Regardless, anticipation of higher supply and lower demand year-on-year during 2024 is likely to limit any meaningful upside in emissions prices for the foreseeable future.

Back in the UK, our electricity generation mix is bearish in nature with renewables contributing 41% and gas-for-power burn at 26%.

Monthly Day-Ahead averages for February ended up at £59/mwh (or 5.9p/kwh).