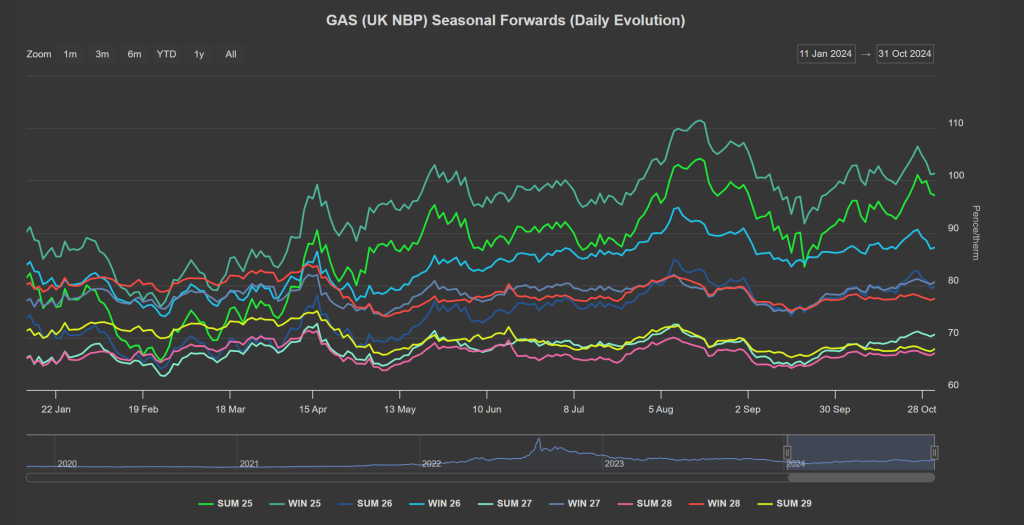

Following the circa. 50% fall in Seasonal Forward prices back in Winter-23 (between Dec-23 to Feb-24), prices down the curve were bunched pretty tight with only 19% separating top to bottom (see chart below).

Thereafter, front Seasons rose in price throughout Summer-24 stretching the Seasonal price differentials – at the time of writing, the curve remains stretched with 33% separating top to bottom i.e., Summer-28 (as the lowest Seasonal cost available) closed yesterday at 66p/therm, whereas Winter-25 (as the highest Seasonal cost available) closed yesterday at 101p/therm.

This reflects, of course, a steeply backwardated market (where future delivery prices are discounted versus near-term delivery prices) i.e., the lion’s share of the risk is front loaded.

At this morning’s open, the UK system was marginally short (demand forecast outstripping supply) – whilst temperatures are above seasonal norms limiting heating demand (bearish), wind outputs are below seasonal norms resulting in higher gas-for-power generation (bullish).

Yet, forecasts of persistent warmer weather and stronger wind speeds toward the end of next week should keep a lid on any bullish momentum.

Right now, prices are down off the back of reports that negotiations look promising for Azerbaijan to replace Russia transitting gas via Ukraine into Europe (once the Ukraine-Russia agreement ends at the turn of the year).

With the US election happening on 5th November, market participants are listening intently to the build-up for any mention of LNG (liquefied natural gas) impacts i.e., policy changes and/or attitudes to conflict escalation/resolution.

Rumours abound that off Russia’s far eastern coast, vessels transporting sanctioned liquefied natural gas are amassing waiting to degasify – reflecting the challenge of finding buyers amid increasingly stringent western regulatory requirements.

However, depending on who wins the election, sanctions on Russian LNG may be subject to change…

Heading deeper into Winter-24, any meaningful upside is being tempered by a de-escalation in Middle East tensions (for now) which lowers some supply uncertainty amid European storage levels at 95% fullness versus the 5-year average of 92%.

Monthly Day-Ahead averages for October achieved 99.161p/therm (or approx. 3.384p/kwh excluding non-gas).

Monthly Day-Ahead averages so far this month are on target to achieve 98p/therm (or approx. 3.344p/kwh excluding non-gas).

ELECTRICITY & CARBON

Looking to the continent for signals, the weather outlook has revised warmer.

Overnight, the outlook has revised windier for the end of next week.

Higher levels of solar generation are forecast from Sunday until Tuesday.

On the carbon markets, EUAs (European Carbon Allowances) saw an aggressive sell-off yesterday throughout the session.

The benchmark Dec ’24 contract opened at €66.85/tn and fell south thereafter, mirroring gas moves.

The CoT data (Commitment of Traders Report) helped further as it indicated there is now more room to short (sell) the market.

On the European electricity forward market, prices were slightly down, following carbon and gas prices (despite poor wind outputs).

Back in the UK, UKAs remain in a longer term downtrend but have spent the last fortnight rangebound between £38 to £40/tn.

However, yesterday saw a break below £38/tn, reaching as low as £37/tn in late afternoon – with activity increasingly choppy but with a bearish bias.

Looking down the electricity curve, FLEX buyers are eyeing up the comparative value on offer with Summer-30 at a 40% discount versus the balance of Winter-24.

Our electricity generation mix is bullish in nature today with renewables contributing 20%, thermal at 42% (gas and coal) and low carbon at 21% (nuclear and imports).

Monthly Day-Ahead averages for October achieved £84.086/mwh (or 8.40864p/kwh excluding non-energy).

Monthly Day-Ahead averages so far this month are on target to achieve £92.026/mwh (or 9.2026p/kwh excluding non-energy)