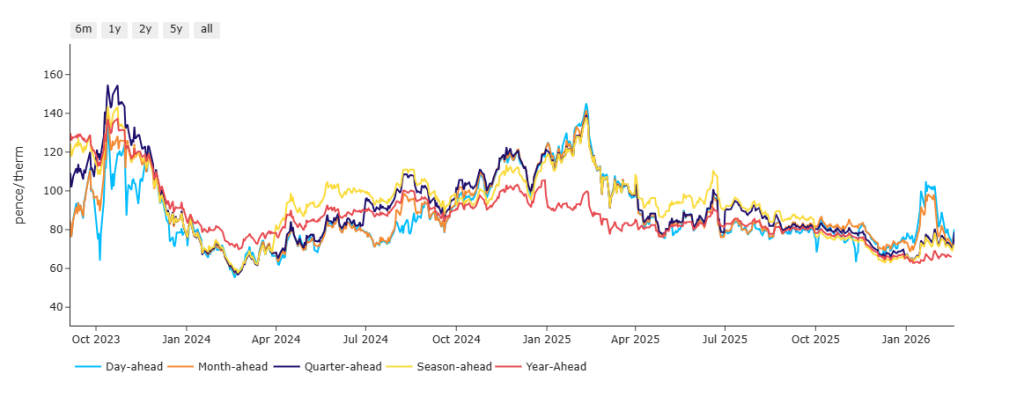

As per the chart below detailing near-term delivery gas prices (Winter-23 to date) , it’s normal to see offers slide heading out of winter into summer.

Given recent volatility which has culminated in a winter spike followed by a sharp drop-off, it’s fair to argue that the lull into summer conditioning has already begun.

Whilst near-term delivery contracts have been well supported this week (amid fears of US-Iran tensions and the elevated risks of LNG disruption through the Strait of Hormuz), the week is nonetheless finishing on a bearish note.

LNG arrivals into Europe and corresponding send-out have been very steady throughout the month (with the UK on-target to degasify nine vessels by month-end).

Asian prices remain at a discount to European prices, ensuring that cargoes make more money by heading our way.

Whilst European storage is still looking very tight (now 32% versus the 5-year average of 58%) , warmer temperatures and improved wind outputs into next week should help ease the pressure on withdrawals (with the end of the heating season now on the horizon).

Forecasts predict that UK wind outputs will be 20% above seasonal norms by the middle of next week.

Nonetheless, traders will keep one big eye on US/Iranian developments and this week’s bullish reactions to geopolitical events serve as a reminder that, whilst fundamentals are pointing toward a soft landing once spring takes hold, unforeseen threats to supply security will always be met by market participants with disproportionate fear and avarice!

On the strategy side, FLEX clients continue to add small positions further down the curve where comparatively great value persists.

Monthly Day-Ahead averages for the month have fallen further to 83p/therm (or 2.8p/kwh).

ELECTRICITY

Seasonal Forwards all the way down the curve are flat on the week, but down versus 1-month/3-months/6-months ago.

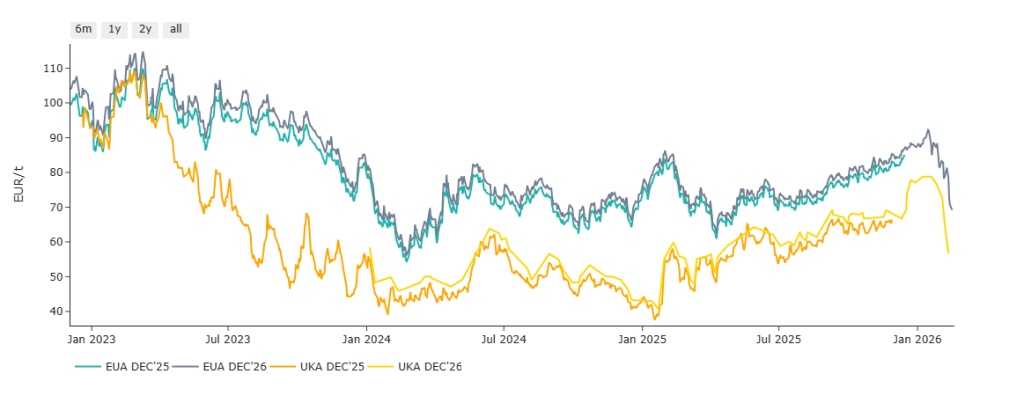

On the Carbon side of things, both EUAs and UKAs have been in free fall amid revelations that make Starmer’s premiership looks increasingly shaky (as traders associate Starmer with linkage of EUETS and UKETS which has meant a climb in UKAs beginning Jan-25 so as to draw UKAs to parity with their more expensive cousin, EUAs).

Since Starmer’s vulnerability has come to the fore these last few weeks, UKAs have become disproportionately bearish with re-linkage starting to look less nailed-on.

At the time of writing, Dec-26 UKA delivery has fallen to £45.42/tn (down 40% versus mid-Jan ’26).

Compliance buyers can only look on and scratch their heads as to how they can budget accurately for a tax which rises and falls with such erratic volatility.

Please see chart below (valued in EUROs) comparing front December EUAs versus UKAs.

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 52%, thermal at 20% (gas and coal) and low carbon at 15% (nuclear and imports).

Monthly Day-Ahead averages for the month have softened to £91/mwh (or 9.1p/kwh exc. non-energy).