The steam having gone out of US/Russia peace negotiations is re-introducing support into near-term delivery prices as optimism fades.

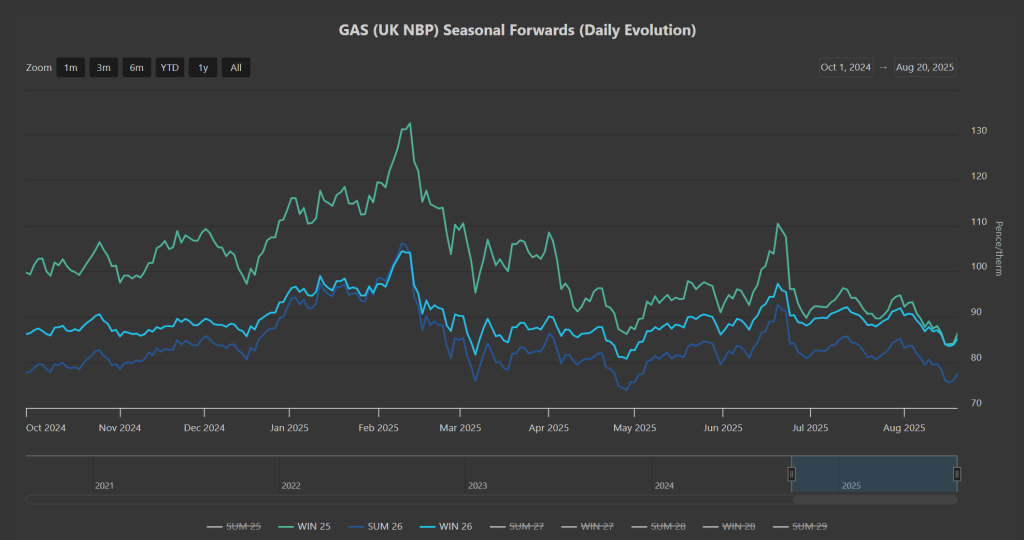

Whilst the front-3 Seasons (Winter-25/Summer-26/Winter-26) are significantly down versus Winter-24’s highs (please see chart below), it’s fair to say that optimistic bears have become despondent bulls in the last few days as it’s become clear that the Kremlin want to be involved in Ukraine’s security guarantees and territorial claims (an unrealistic prospect given their other roles as invaders/occupiers/aggressors).

And so, market participants have once again to face up to the reality that the re-introduction of Russian flows into Europe is next to zero.

By way of rubbing salt in the wound, rumours abound that Serbia (an official candidate for EU membership since 2012) is on the verge of closing a deal with Gazprom (Russia’s state provider) to acquire more than 6 million m³ of gas per day at a discounted rate versus prevailing European pricing.

Other than that, it’s as you were – supply remains steady (though Norwegian flows are drifting lower as the climax of the scheduled maintenance season approches); injections creep toward Europe’s storage objective of 85% fullness in time for the onset of the heating season (now at 75% versus the 5-year average of 85%); wind outputs look steady across Europe, but shaky in the UK (so our generation mix is neither supportive nor bearish to end the week).

Norwegian outages are likely to pick up next month, so focus will shift to Winter-25 storage, and the potential impacts of mid-to-long range weather forecasts.

Any late buyers of Winter-25 delivery are still advised to get in BEFORE the 2nd week of September at the very latest.

Monthly Day-Ahead averages for the month so far are at 79p/therm or 2.7p/kwh (all but unchanged from the start of the month, reflecting very low-short term risk).

ELECTRICITY & CARBON

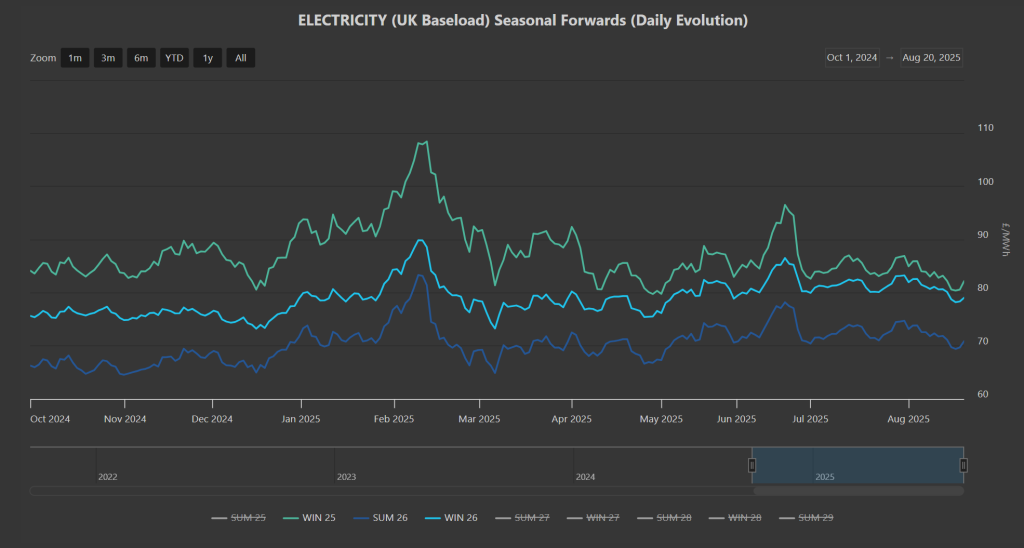

Winter-25 and Winter-26 delivery are almost flat, with Winter-26 at only a 3% discount versus its nearer-term cousin (please see chart below).

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are at £52.45/tn on the mid-price, having fallen below support to start the week but now retesting resistance – in short, it’s rangebound price action with prices having traded within a 15% bracket since the onset of Summer-25 (1st Apr).

Today’s UK electricity generation mix is neutral in nature – specifically, renewables are contributing 31%, thermal at 25% (gas and coal) and low carbon at 26% (nuclear and imports).

Monthly Day-Ahead averages for the month so far are at £71/mwh (or 7.1p/kwh exc non-energy).