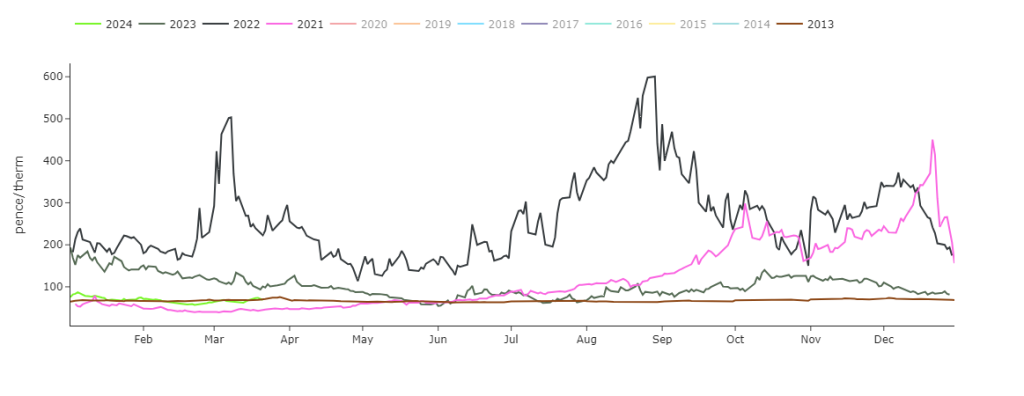

Month-Ahead prices are now commensurate with those printed in 2013 (though still above early ’21, but way below ’22) – see chart.

We had another bearish day yesterday, and a sideways day today.

Temperatures are mild and windy.

Low exports out of the UK to the continent reflect weak LNG send-out.

9 days of Winter-23 remain, and nothing in the fundamentals makes us think that further downside is not going to happen with the onset of summer conditioning – lower demand, high storage, solid Norwegian flows.

Geopolitically speaking, a ceasefire would likely calm the Red Sea disquiet (and so alleviate the tension around LNG re-routing etc)

Monthly Day-Ahead averages are on target this month to achieve 68p/therm (or 2.3p/kwh).

ELECTRICITY & CARBON

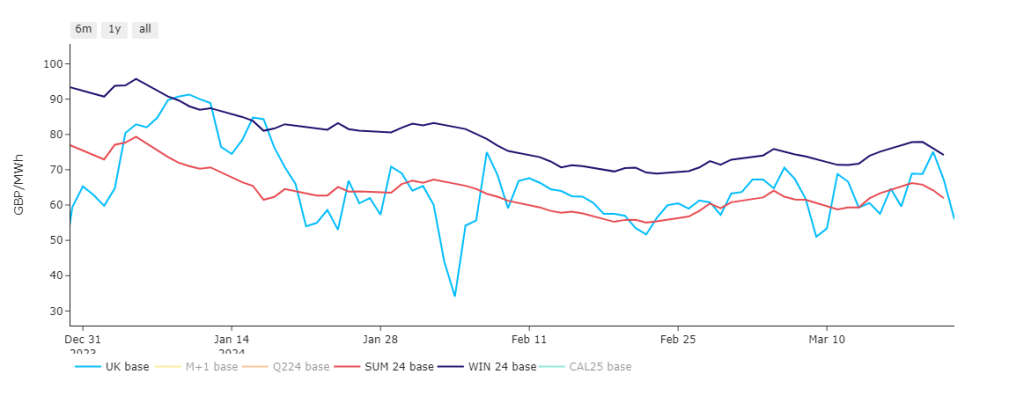

Day-Ahead continues to use Winter-24 prices as resistance (see chart).

Looking to the continent, European near-term delivery prices continued to fall as expected yesterday, weighed by soaring wind outputs and falling demand.

The weekend may see prices plummet due to surging wind production, though the market could find support early next when wind drops off and temperatures fall.

Though these weather conditions are not expected to last, so it’s all about treading water in a tight price range right now.

Down the curve, contracts are being dragged down by declining gas and emissions prices (as gas supply reduction worries slowly fade and participants remember the still very comfortable fundamental outlook).

On the carbon markets, yesterday saw another calm and slightly bearish session, the benchmark contract dropping below the 60 €/t mark in the first hours of trading then slowly decreasing throughout the day.

Today, it’s been a pretty directionless session with prices having found equilibrium.

At the time of writing, Dec-24 contracts for UKAs are sitting at £38/tn.

The UK’s electricity generation mix is bearish in nature today with renewables contributing 44%, thermal at 18% (gas and coal) and low carbon at 26% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £65/mwh (or 6.5p/kwh).