European storage is still at 65% versus the 5-year average of 45%, Norwegian flows to the UK/Europe remain steady, LNG arrivals are constant, and temperatures are forecast to rise back above seasonal norms by the middle of next week.

Whilst the UK system opened short this morning (demand outstripping supply), demand remains below seasonal norms.

With Summer-24 only 37 days away, only geo-political unrest poses any risk to a continuation of the prevailing bear trend.

Monthly Day-Ahead averages are on target this month (so far) to achieve 64p/therm (or circa. 2.2p/kwh).

ELECTRICITY & CARBON ALLOWANCES

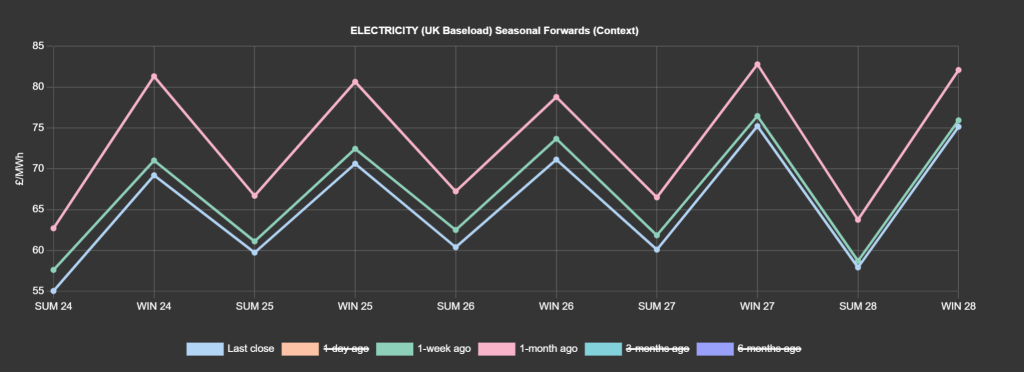

Front seasons (Summer-24/Winter-24) are at a circa. 12% discount versus 1-month ago (see chart).

Looking to the continent, European short-term delivery prices experienced significant volatility yesterday amid very strong wind production, which then dropped off abruptly – after which prices found support driven by a fall in temperatures and weakening French nuclear availability.

Next week, prices should find support off the back of colder and calmer weather against a backdrop of ongoing weakness in French nuclear availability – although prospects of stronger solar generation could offset bullish momentum.

Down the curve, prices are extending their decline pressured by declining fuels and emissions prices, comfortable fundamentals and lack of demand recovery as the end of Winter-23 is on the horizon.

On the carbon markets, EUAs reversed a 2-day retracement yesterday and resumed its downtrend plummeting to a 31-month low.

Prices remain on a downward trajectory – unchallenged by prevailing softness across the wider energy complex.

UKAs are still threatening to retest the psychological support levels of £30/tn.

Back in the UK, our generation mix is bullish in nature with renewables contributing 21% and gas-for-power burn at 39%.

Monthly Day-Ahead averages for UK electricity are on target this month (so far) to achieve £59/mwh (or 5.9p/kwh).