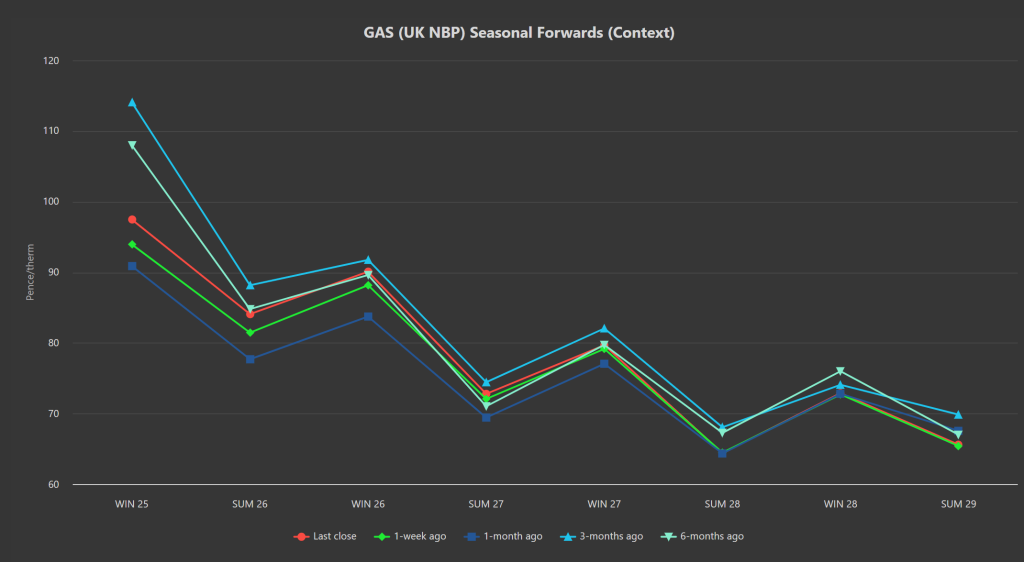

The bulls are finishing the week with the upperhand.

Seasonal Forwards are up on the week and month (please see chart below).

Whilst markets fell yesterday from the highs we saw on Wednesday, the front seasons are reacting bullishly today to LNG shippers seeing higher demand out of Asia off the back of higher temperatures (and the need for gas-fired generation to power cooling demand).

European storage levels are at 45% versus the 5-year average of 58% – so injections this week have been muted/flat, amplifying the storage deficit.

Not surprisingly, US tariff impacts are slowing global economic activity which in turn is decreasing energy consumption (demand destruction) – though lower demand will take time to pressure prices.

With the resumption of Russian gas flows now seemingly off the table, market participants are back to obsessing over storage replenishment in time for the heating season.

The inevitable rise in summer demand across Asia (it happens every year), is adding risk-premium with LNG competition likely to pick-up.

Egypt (which is actively seeking LNG cargoes amid a worsening energy crunch ahead of peak summer demand) is also likely to add further competition to global LNG demand over the coming weeks.

The International Gas Union summed it up well yesterday stating that competition between Asia and Europe for LNG volumes would intensify ahead of summer, adding that “the global LNG market equilibrium is fragile and sensitive to uncertainties from both supply and demand sides”.

Still, Europe continues to push for deeper sanctions against Russia – making it difficult to see where the Ukraine conflict is headed (and further weakening Europe’s ability to secure much needed gas flows).

Norwegian flows have been patchy due to summer maintenance (it happens every year), though capacity is coming back online to finish the week.

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst markets still offer solid comparative value.

This month’s UK gas Day-Ahead averages are holding steady at 81p/therm (or approx. 2.7p/kwh excluding non-gas).

ELECTRICITY & CARBON

Electricity remains tethered to gas movements (as you’d expect given the UK’s ongoing reliance on gas-for-power generation).

As such, Winter-25 is printing £88/mwh at the time of writing (up nearly 10% versus the recent lows on 1st May).

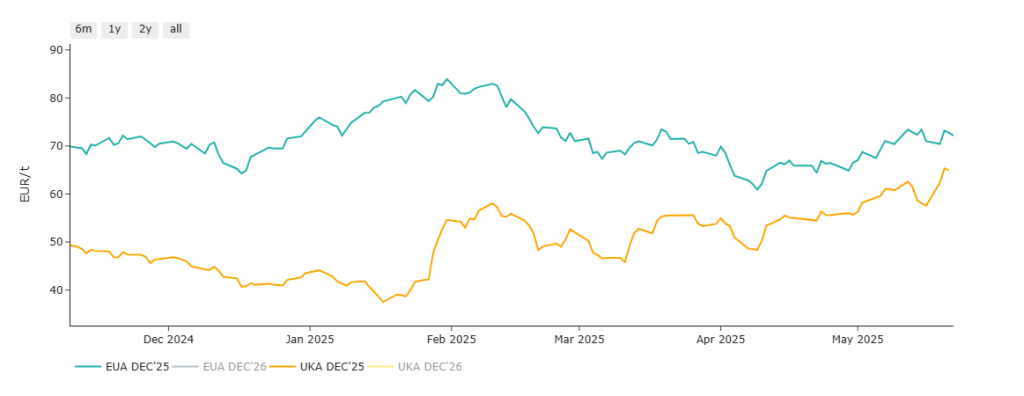

On the Carbon side of things, this week the UK and EU formally agreed to work towards linking their Emissions Trading Systems.

The accord was announced at the EU-UK summit in London, citing aims to “create a level playing field” and “improve energy security” (the link would also mean the UK will avoid being hit by the EU’s carbon tax due to come in next year, potentially saving £800 mn…)

Not surprisingly, given that EUAs remain at a premium to UKAs, this announcement has been price supportive of UKAs as the two markets approach price parity in anticipation of the market merge (please see chart below).

Heavy-emitters across the UK will be disappointed to see this tax back up above £50/tn – currently printing at £54.94, and most definitely back in a bull-run.

Nonetheless, today’s UK electricity generation mix is bearish in nature reflecting solid renewables outputs – specifically, renewables are contributing 40%, thermal at 17% (gas and coal) and low carbon at 27% (nuclear and imports).

So far this month, electricity Day-Ahead averages are holding steady – currently at £75/mwh (or approx. 7.5p/kwh excluding non-energy).

On the trading side, clients running flexible capability are encouraged to scale-in modest hedges over the coming days/weeks whilst markets still offer solid comparative value.