Markets are rangebound this morning, but have a decidedly bullish tone to them, with prices increasingly feeling-out the upper range.

Over the coming days/weeks, if the US siege of Iran persists, it seems increasingly likely that buyers across Europe/the UK will have to contend with the ever-complex conundrum of when to pull the trigger on Forward-hedges (given how open-ended the conflict has become over the last week or so).

On the face of it, Trump is looking to drain the regime of financial resources by cutting off their revenue streams (and/or bring about internal revolution by an increasingly desperate population).

Amid further reports of vessel seizures by both the US and Iran, confirmation of a 3-week extension to the Israel/Lebanon ceasefire feels like another red flag – 3 weeks is a long time for Asia to abide whilst the Strait remains closed (and essential imports remain stuck on the wrong side of the waterway).

And whilst Asia is unable to access vital resources, they’ll be increasingly forced to compete with Europe in global markets, driving up prices – who knows, the whole world could be fighting for US oil and LNG come Q3.

Flight cancellations due to jet fuel shortages will become more prevalent over the coming weeks/months.

Europe’s reserves are designed to last 90 days (longer if eked out), but if the Strait remains closed, Europe will be forced to stop injecting into storage come Q326, meaning a shortfall in reserves before the onset of the heating season in November.

If this happens, inevitably markets will go to the moon – much as they did back in ’22.

If we then have a cold winter, significant economic contraction across Europe/the UK amid higher interest rates (to dampen inevitable inflation) will be the outcome.

This of course is worst case scenario, but if Trump is of a mind to weaken Asia/Europe (given his well-publicised protectionist agenda), he’s quite clearly already secured the means by which to do so.

Don’t forget the Pentagon has already suggested that even if the Strait opens, it will take 6 months to clear the mines that the Iranians have placed along the Oman-side of the Strait.

Back to this morning, prices are roughly still about 40% above pre-war levels.

Notably, amid the prevailing supply squeeze, the EU will stop buying Russian LNG on the spot market beginning Saturday (though longer‑term contracts are permitted to run up to year‑end).

With Russia, even now, still accounting for more than 10% of Europe’s demand, one has to wonder if Europe’s leaders aren’t being out maneuvered by Trump/Putin.

On the supply side, LNG send-out is decreasing incrementally day on day (with no UK arrivals scheduled for the coming weeks).

Heavy exporters of LNG (the US/Russia/Australia/Canada) are likely to reap untold profits this summer as Europe and Asia fight for captive resources.

If its Trump’s intention that the waterway be closed indefinitely so as to serve his political objectives, who is going to stand in his way (considering that 28 US warships will be protecting the blockade)?

On the trading side, FLEX clients are all but closed-out for May in the hopes that, come June, the Strait will re-open and essential LNG transit will have been restored.

For now, however, it’s increasingly difficult to see just how/when the impasse might be overcome – or whether there’s a willingness on the part of the US to do so at all.

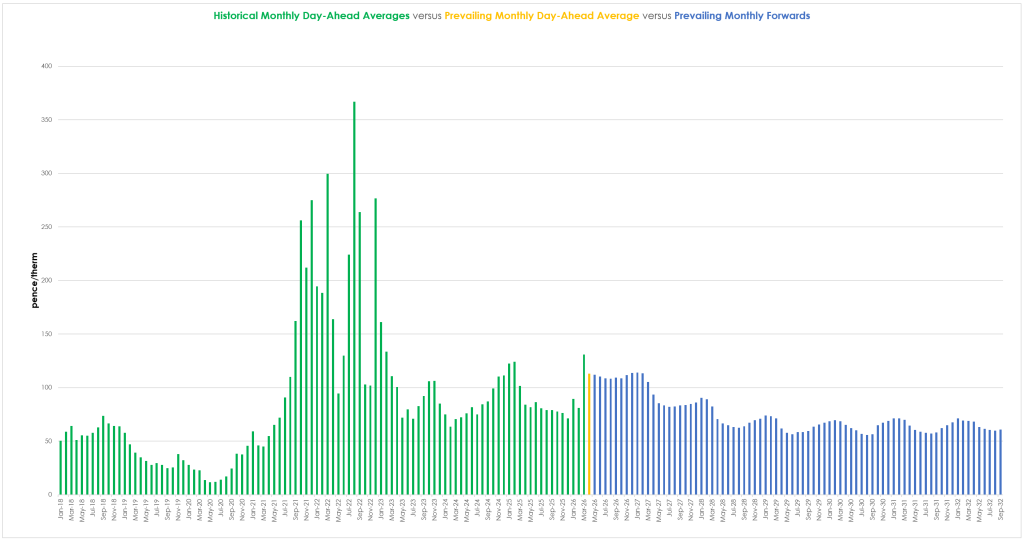

Monthly Day-Ahead Averages for the month remain are holding steady at 113 p/therm (or 3.9 p/kwh exc. non-gas).

ELECTRICITY & CARBON

Thankfully, UK electricity prices have been significantly less volatile than gas prices since the US/Israeli offensive began back on 28th Feb.

Suffice as to say, given summer conditions (improved renewables/lower gas for power burn), UK electricity prices remain comfortably below the psychological level of £100/mwh.

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 43%, thermal at 5% (gas and coal) and low carbon at 29% (nuclear and imports).

On the trading side, FLEX clients are all but closed-out for May in the hopes that, come June, the Strait will re-open and essential LNG transit will have been restored.

For now, however, it’s increasingly difficult to see just how/when the impasse might be overcome – or whether there’s a willingness on the part of the US to do so at all.

On the Carbon side of things, Dec-26 UKA delivery began the conflict heavily correlated to gas markets – so when gas prices fell, UKAs rose (and vice versa).

However, given this week’s volatility in UKAs, having fallen £3/tn on Tuesday, we increasingly see a correlation with global equity markets which are enjoying a strong, tech-led rally begining 1st April.

Key drivers include robust corporate earnings, with the benchmark S&P 500 up 9% this month so far.

At the time of writing, UKA mid-price Dec ’26 delivery is back up to £50/tn (and the spot is at mid-48s).

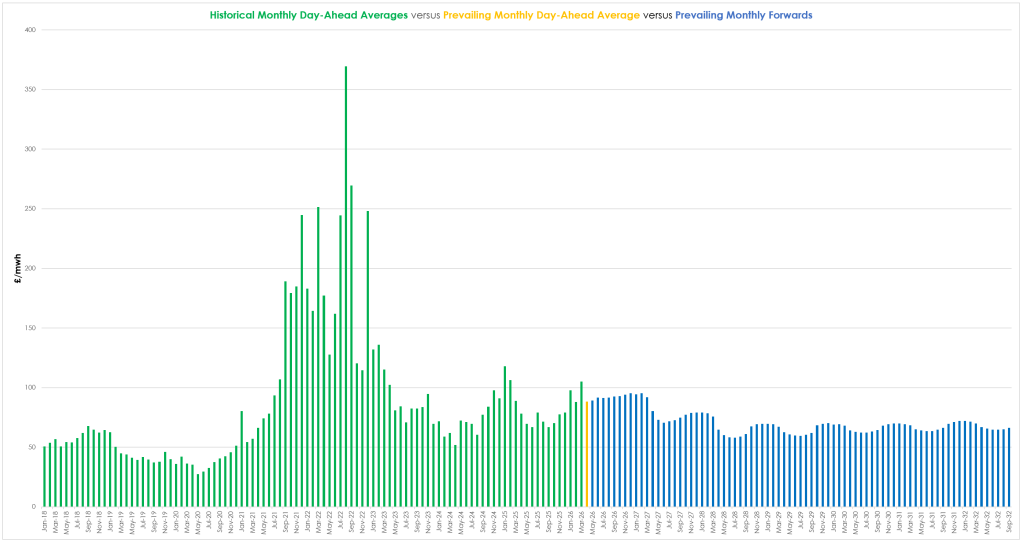

Monthly Day-Ahead Averages for UK electricity for the month are holding steady at £88/mwh (or 8.8 p/kwh exc. non-energy).