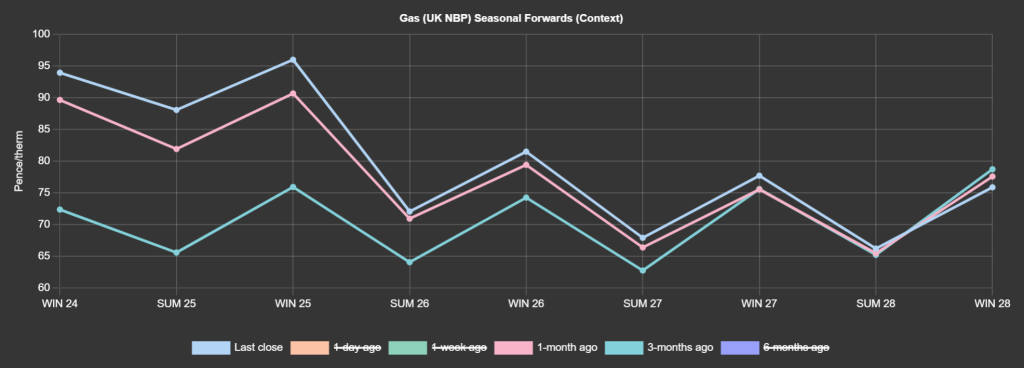

It’s been a bullish week on the markets – particularly for the Prompt (Day/Month/Quarter-Ahead) and the front seasons (Winter-24/Summer-25/Winter-25).

Prices are up versus 1-month ago and 3-months ago – see chart.

Oftentimes, when markets don’t have enough impetus to go lower, the only options for price is to consolidate sideways or test historical highs.

Speculators make more money from volatility than they do from markets in equilibrium.

Notwithstanding bearish fundamentals, prices found support this week from a mixed bag of bullish drivers:

a) One of the main contactors of a new LNG export plant in the US (Golden Pass) filed for bankruptcy which could delay the launch.

b) Remaining Russian gas supplies through Ukraine may be suspended.

c) Lower renewables outputs coupled with reduced Norwegian flows due to maintenance.

d) A rise in coal prices and Asian gas prices (warmer weather projections have sent Asian LNG prices to their highest points since January, suggesting that Asian demand for LNG may pick up in the upcoming months).

e) Reports broke from Austria’s OMV that a foreign court decision could seize payments made to Gazprom and therefore cut Russian supply to the remaining European countries receiving gas.

At present this has only impacted OMV but other countries could face the same possibility in coming weeks and this risk has caused European markets to climb.

Low wind remained the theme for today with temperatures also dropping below seasonal norm over the coming weekend.

Wind generation should see a boost on Monday as the UK enters a more unsettled period of weather bringing some boost to near-term renewables outputs.

Lest we forget, MRS (European mid-range storage) levels are at 68% fullness versus the 5-year average of 49%.

Looking at the bigger picture then, geopolitical support remains at odds with seasonal pressure (falling demand/solid supply/less reliance on withdrawals etc).

Monthly Day-Ahead averages are on target this month to achieve 72p/therm (or circa. 2.45p/kwh excluding non-gas).

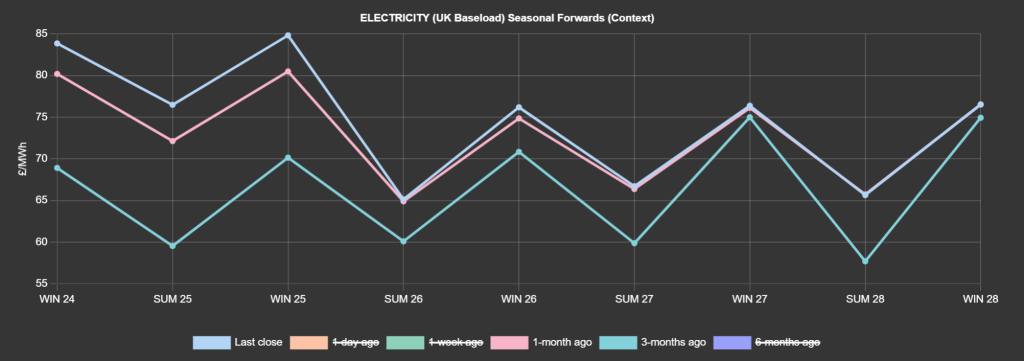

ELECTRICITY & CARBON

Looking to the continent, near-term electricity delivery prices extended their bull rally yesterday on forecasts of falling wind/solar/nuclear availability.

Next week, persisting weak wind output should continue to support the spot market, although French nuclear availability is forecast to pick-up amid public holidays in Germany on Thursday – which should offset some of the bullish momentum.

On the European Carbon markets, prices lost steam and traded sideways yesterday.

Market participants (bears evidently) cite the still mostly comfortable fundamentals suggesting that we could be due for a profit-taking correction.

The EUA Dec ’24 contract is still testing its 1-year moving average which, if broken, could be a strong signal for a steep correction downwards!

Back in the UK, UKAs (UK Allowances) are still on a bull run – now trading at circa. £46/tn (Dec-24 benchmark) – having broken above the highs printed on 25th Mar ’24 and having breached overhanging resistance trendlines.

Our electricity generation mix is bullish in nature today with renewables contributing 16%, thermal at 42% (gas and coal) and low carbon at 30% (nuclear and imports).

Monthly Day-Ahead averages are on target this month to achieve £71/mwh (or 7.1p/kwh excluding non-energy).