We’ve seen another very steady week on the markets – calm and balance persists.

The heating season has yet to begin in earnest, and across Europe/the UK, gas storage facilities remain in net injection mode (easing the pressure on demand, and prices).

European storage fullness is holding steady at 83% versus the 5-year average of 95%.

Market participants continue to balance benign fundamentals against geopolitical risk – LNG arrivals and send-out are strong, Norwegian pipeline flows are still well under capacity (with maintenance seemingly dragging on at Troll, Kollsnes and Nyhamna) but steady nonetheless, but Russia’s repeated targeting of Ukrainian energy infrastructure means some EU gas supply will likely be needed to replace disabled domestic output.

On the supportive side (looking at the wider energy complex), Trump’s dawning realisation this week that Putin is paying the peace process lip-service only, has resulted in US penalties being imposed on Russia’s big oil producers (Rosneft and Lukoil).

On the weather front, stormy conditions across Europe are contributing to solid wind outputs (limiting gas for power burn/storage withdrawal).

No doubt emboldened by Trump’s new found willingness to impose further sanctions on Russia, EU leaders are increasingly engaging with Zelenskiy’s plan to draw off Russia’s frozen assets to support Ukraine’s defence.

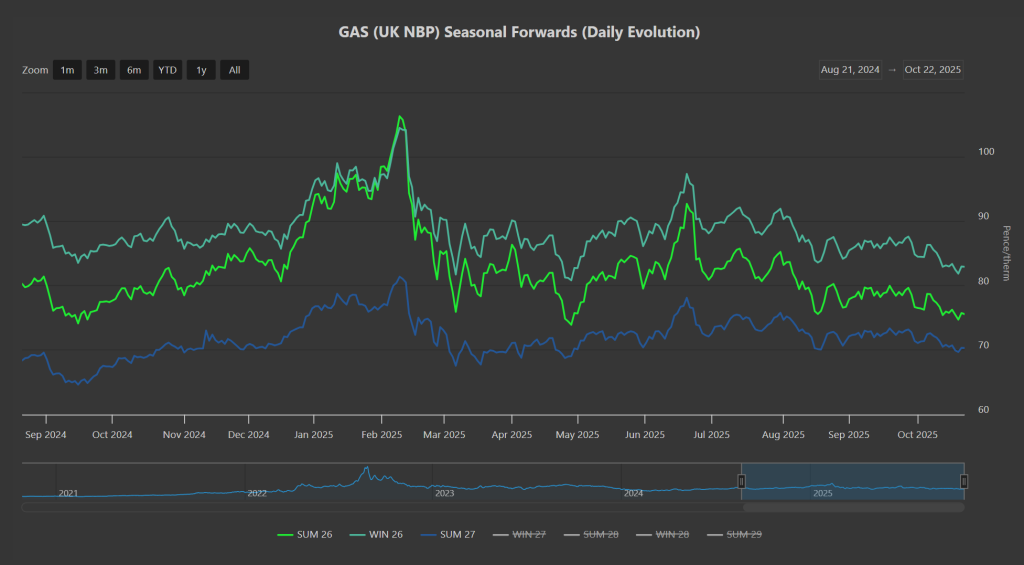

Looking at price action, this time last year, the front 3-Seasons were increasing in price – this year, they’re still dropping off (please see chart below) – a reflection of significantly lower spot/Day-Ahead volatility, and an underlying sentiment that Europe’s supply insecurity is certainly less pronounced than it was back in ’21/’22/’23 (which is saying something, given that this time last year, European gas storage was higher at 93%).

Monthly Day-Ahead averages for October remain at 78p/therm (or 2.66p/kwh exc. non-gas) – unchanged since 10th Oct.

ELECTRICITY & CARBON

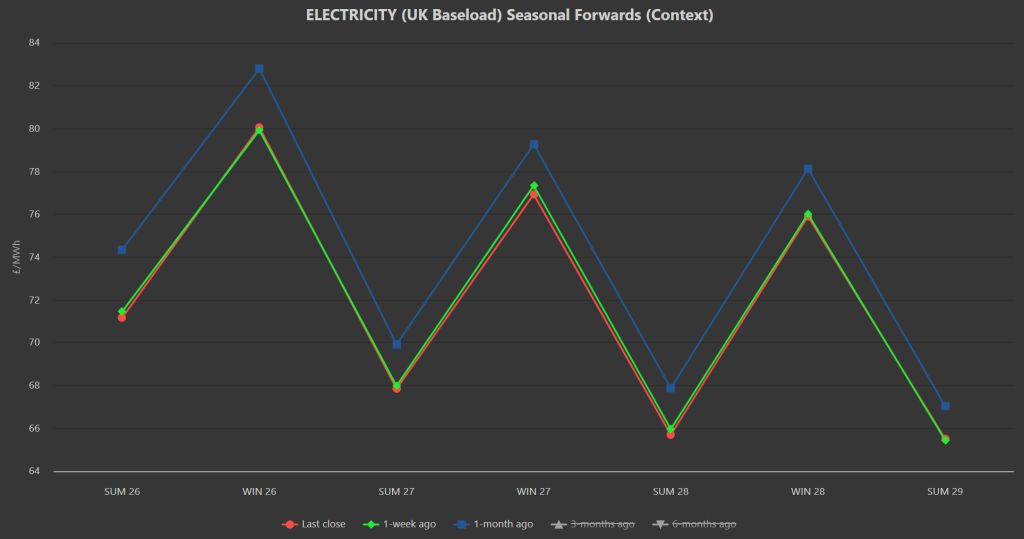

Electricity Seasonal Forwards are barely altered versus 1-week ago, but clearly reduced all the way down the curve versus 1-month ago (please see chart below).

On the Carbon side of things, UKAs are increasingly correlated to EUAs (following the “common understanding” reached between the UK/Europe to link emissions markets at the UK-EU summit in London on 19th May).

Dec ’25 UKA benchmark prices are retesting the lower extremity of a triangle/consolidation pattern that’s been in place since mid-Sep.

At the time of writing, prices are holding steady in the mid-50s (currently at £54/tn) – let’s see if the triangle breaks to the downside (we suspect it will not – instead, we expect more bracketing to retest the upper extremity of the triangle as plenty of room remains before the pattern runs out of road).

Today’s UK electricity generation mix is bearish in nature – specifically, renewables are contributing 53%, thermal at 8% (gas and coal) and low carbon at 23% (nuclear and imports).

Monthly Day-Ahead averages for October so far have fallen in the past week to £73/mwh (or 7.3p/kwh exc. non-energy).