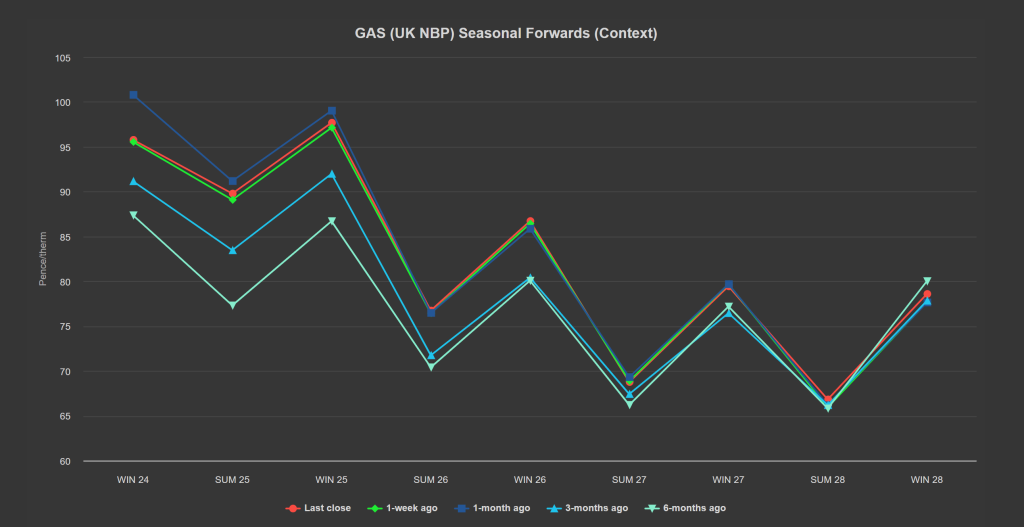

Despite intermittent bursts of “summery” conditions, Seasonal Forwards are barely changed on the week and on the month – see chart below and at https://icdenergymanagers.com/charts/

What’s also evident from the chart is that Seasonal Forwards were better 3-months ago (at the outset of Summer-24) and even better 6-months ago whilst we were still in Winter-23!

In short, the loss of Russia’s Nordstream gas into Western Europe continues to skew the rhythms of the market – and our subsequent increased reliance on LNG has become supportive given global competition for cargos.

Markets continued their plod sideways at this morning’s open – with near-term delivery bound by directionless range trading.

The UK system opened long (supply outstripping demand forecast) – this despite a bump-up in overall demand off the back of lower temperatures (again).

Though forecasts would have us believe that temperatures are still set to increase next week and sit around 3 to 4°C above seasonal norms.

Competition for global LNG has been further evidenced this week with India having purchased more cargos for August and October to facilitate cooling demand.

Were it not for Norwegian flows above seasonal norms and plentiful European storage (83% verus the 5-year average of 76%), markets might be pushing northwards.

Thankfully, summer conditioning prevails and supportive elements are being matched by bearish pressure – hence the meandering sideways movement.

Looking at the big picture, with demand low, and supply comfortable, replenishing gas stocks is not posing any problems.

Europe remains on track to achieve 100% storage levels by Winter-24 (early Oct ’24) – though LNG delivery remains tight against a backdrop of sustained high temperatures across Asia (and the associated cooling demand).

On the hedging side, we’re now on the other side of Summer-24 – with 116 days having elapsed, and 68 remaining.

Clients with open volumes for Winter-24 are increasingly scaling-in so as to avoid any loss of prevailing value.

Monthly Day-Ahead averages so far this month are on target to achieve 74p/therm (or circa. 2.5p/kwh excluding non-gas).

ELECTRICITY & CARBON

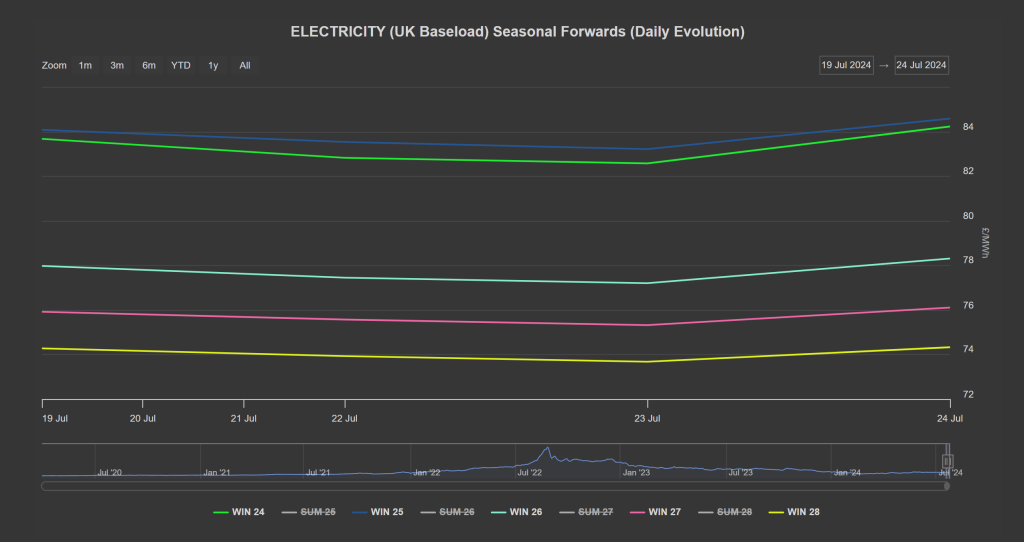

Looking specifically at winter Forwards (see chart below and at https://icdenergymanagers.com/charts/), Winter-28 is at an 11% discount (approx. £10/mwh) versus Winter-24 – a reflection of how standardised risk-premium for winter delivery (all the way down the curve) has become.

Looking to the continent, volatility came roaring back across European power markets yesterday on two fronts – firstly, RTE’s (France’s transmission operator) statement detailing a likelihood of further constraints on export capacities across eastern borders from next week.

Secondly, EDF has expanded its list of reactors at risk of maintenance delays linked to stress corrosion issues next year by 10 units to a total of 23 in a declaration of transparency.

In other bullish news, the benchmark EUA Dec ’24 price continued a technical rebound rallying intraday and moving beyond its 20-day moving average throughout the session, propelled most likely by the COT (Commitment of Traders Report) showing an increase in short positions from speculative players last week, which usually fuels the bullish trend on expectations of speculative players closing out these short positions (contrarian indication!)

Despite a warmer revision in temperature forecasts for next week in western Europe, decent levels of solar and wind power generation are likely to keep a lid on near-curve contracts notwithstanding yesterday’s rally – with more bearish pressure on French prices where export constraints should continue to weigh on sentiment, notably on the back of rising nuclear generation.

EUA prices could take a breath after the rally of the past two trading sessions in the absence of any meaningful fundamental drivers (other than fear and avarice amonogst participants)!

Back in the UK (and despite EUA’s technical repositioning), UKAs (UK Carbon Allowances) continue to fall (as indicated by RSI divergence and confirmed descending trend channels) – now trading at circa. £39/tn.

Our electricity generation mix is a little bearish in nature today with renewables contributing 33%, thermal at 25% (gas and coal) and low carbon at 26% (nuclear and imports).

Monthly Day-Ahead averages so far this month are on target to achieve £68/mwh (or circa. 6.8p/kwh excluding non-energy).